Helping Millennials cut taxes, boost income, and build wealth • @InvestmentNews Best Wealth Managers Under 40 • @Investopedia Top 100 FA • Tweets ≠ Advice

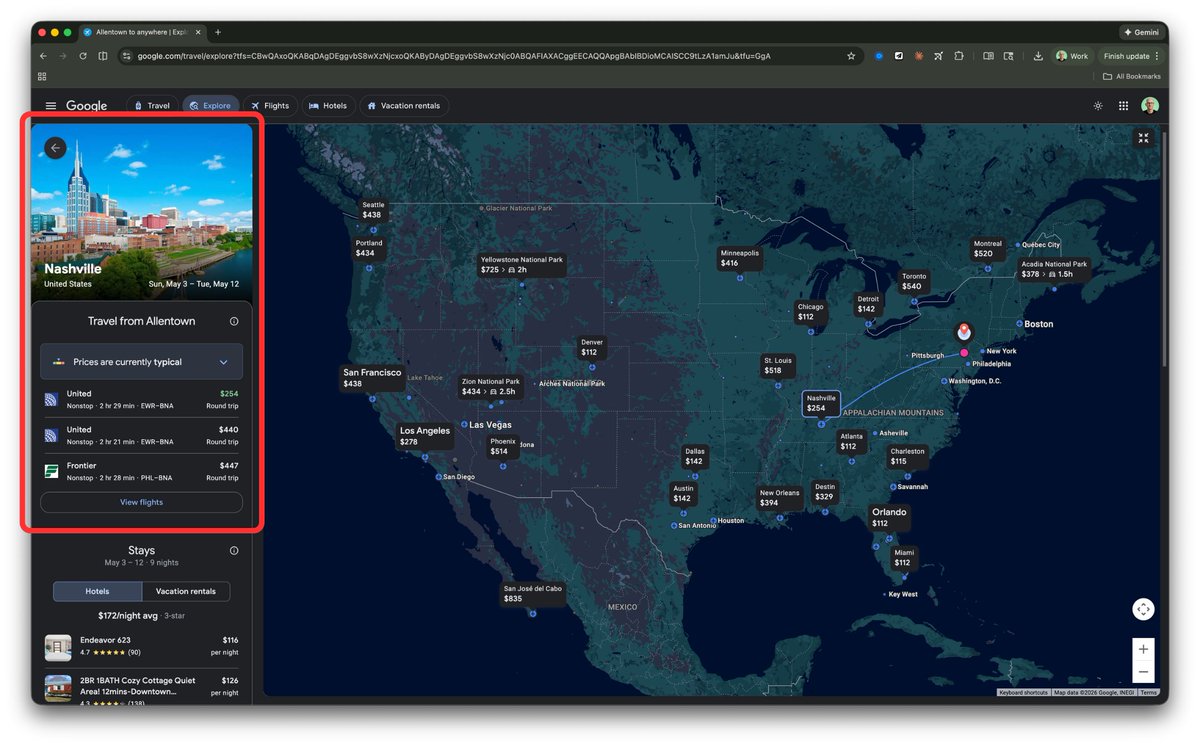

Most people search flights the expensive way:

Most people search flights the expensive way: The hard truth?

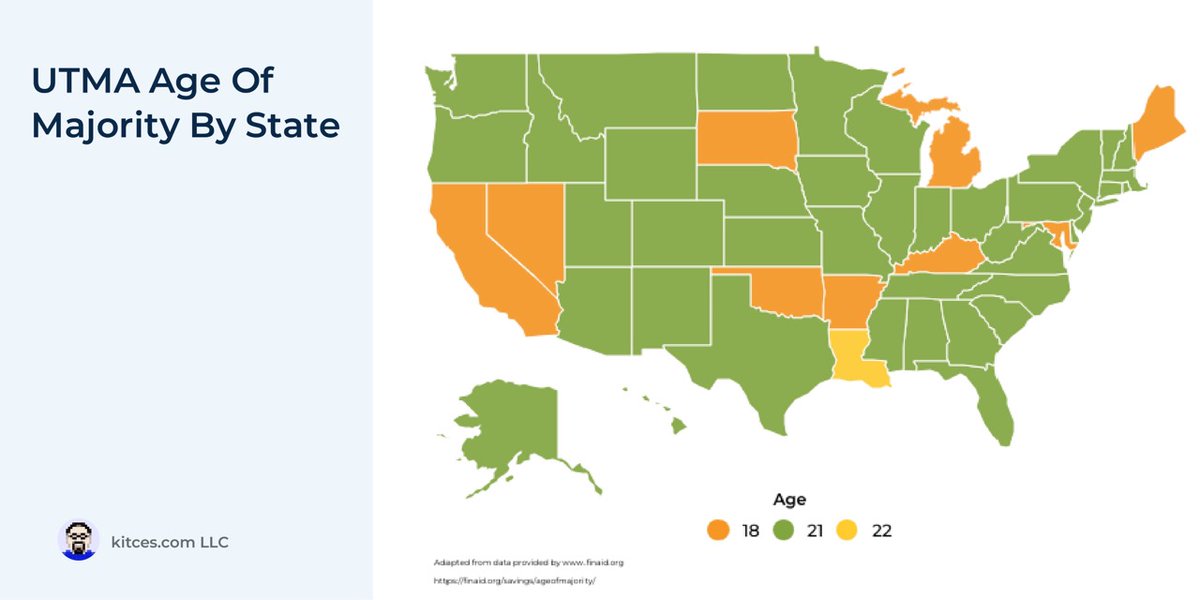

The hard truth? The IRS has a rule most parents don't know about.

The IRS has a rule most parents don't know about. The industry trained us specifically: Make 500 cold calls a week.

The industry trained us specifically: Make 500 cold calls a week.

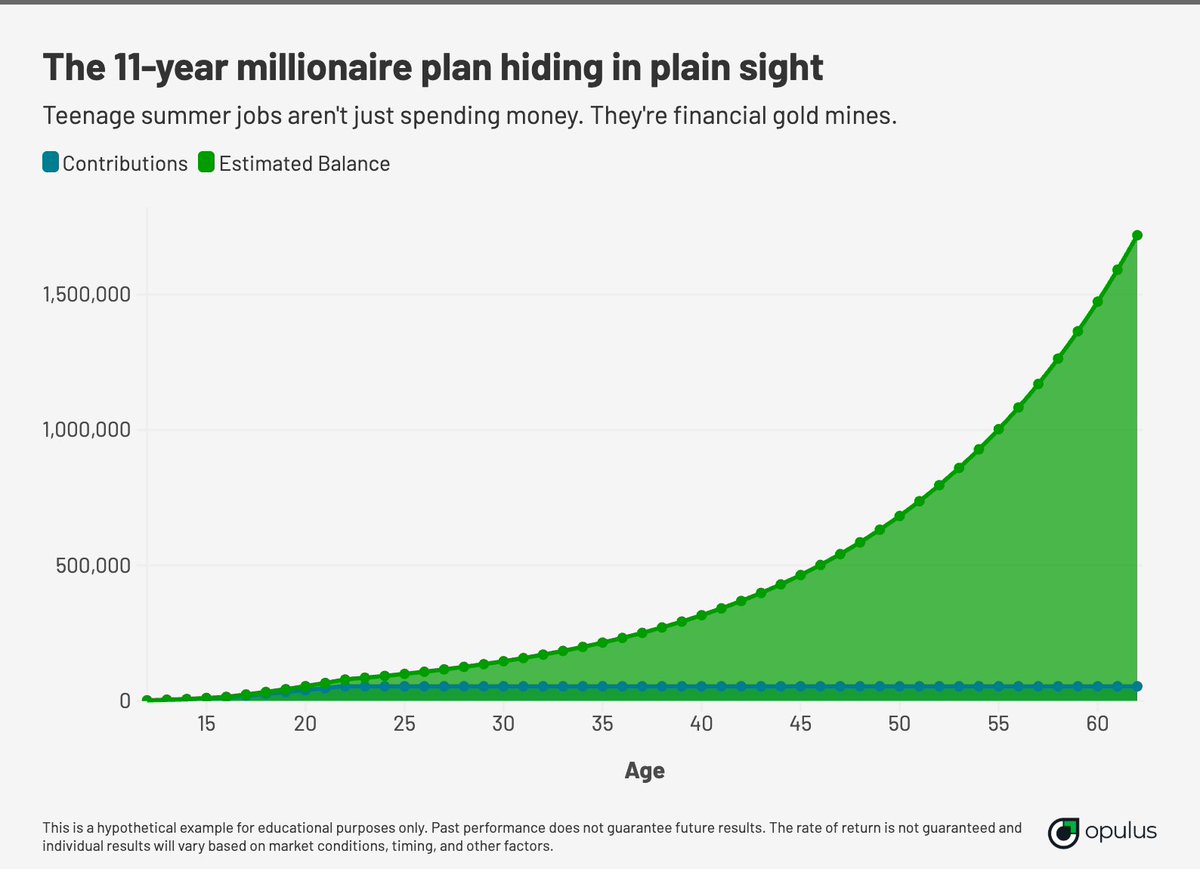

First, the opportunity:

First, the opportunity:

Ever notice how flight booking feels designed to empty your wallet?

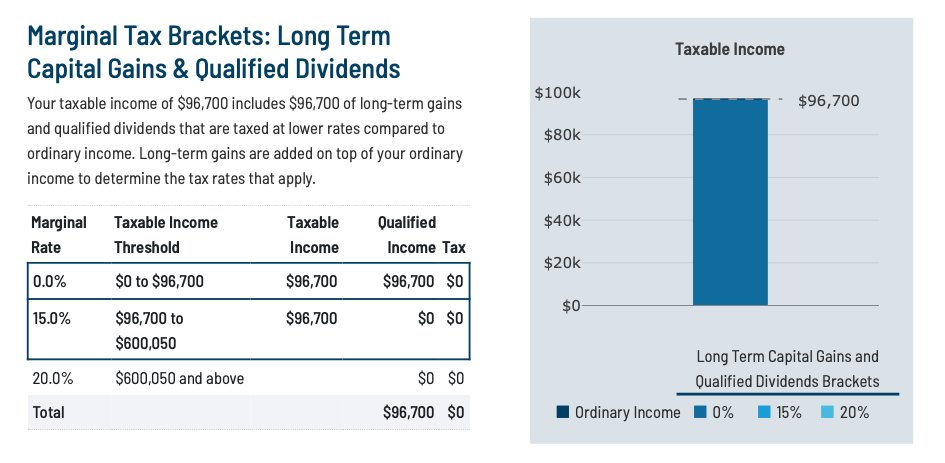

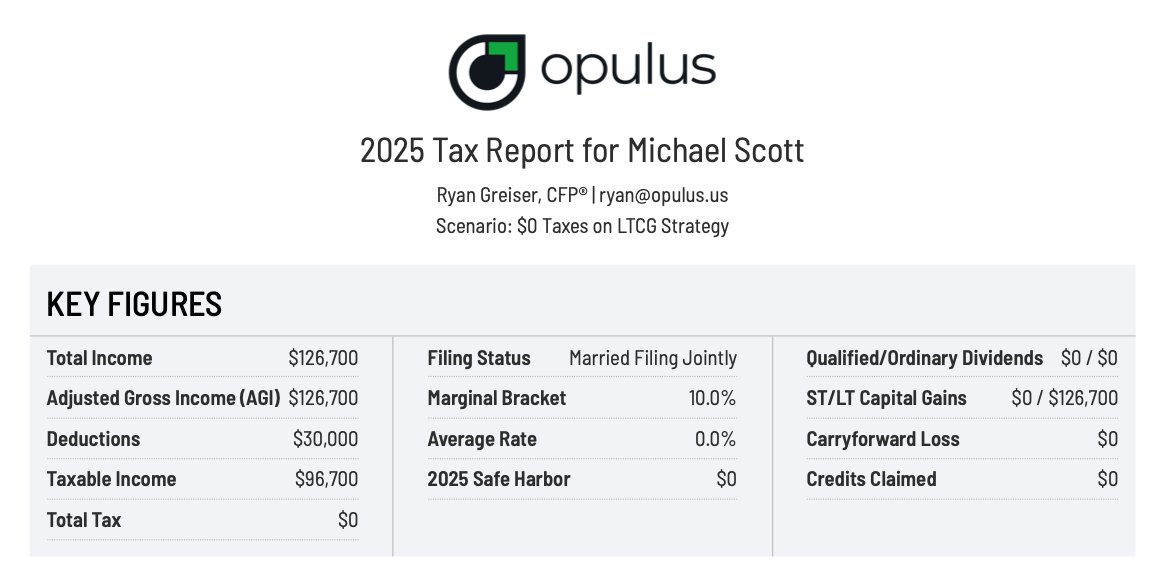

Ever notice how flight booking feels designed to empty your wallet? Here's the math behind the Zero-Tax strategy for 2025:

Here's the math behind the Zero-Tax strategy for 2025: