these are so simple, so easy, that even i can’t mess them up.

these are so simple, so easy, that even i can’t mess them up. you can read it here: robotjames.substack.com/p/a-dirty-long…

you can read it here: robotjames.substack.com/p/a-dirty-long…

read the full article here because it's comprehensive and massive and contains a bunch of statistical modeling code:

read the full article here because it's comprehensive and massive and contains a bunch of statistical modeling code:

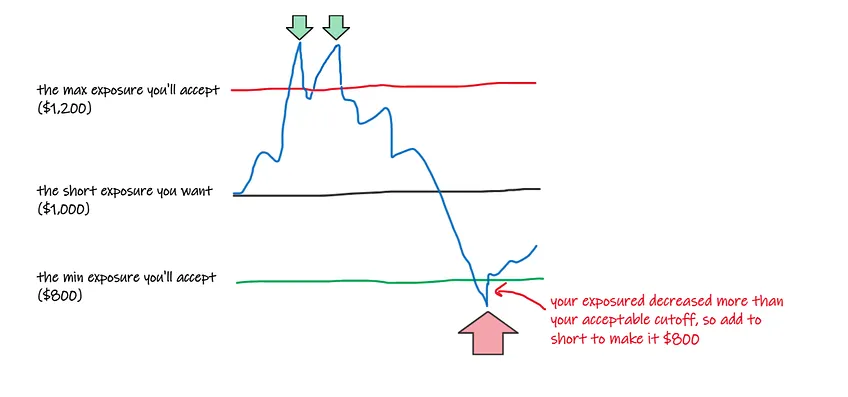

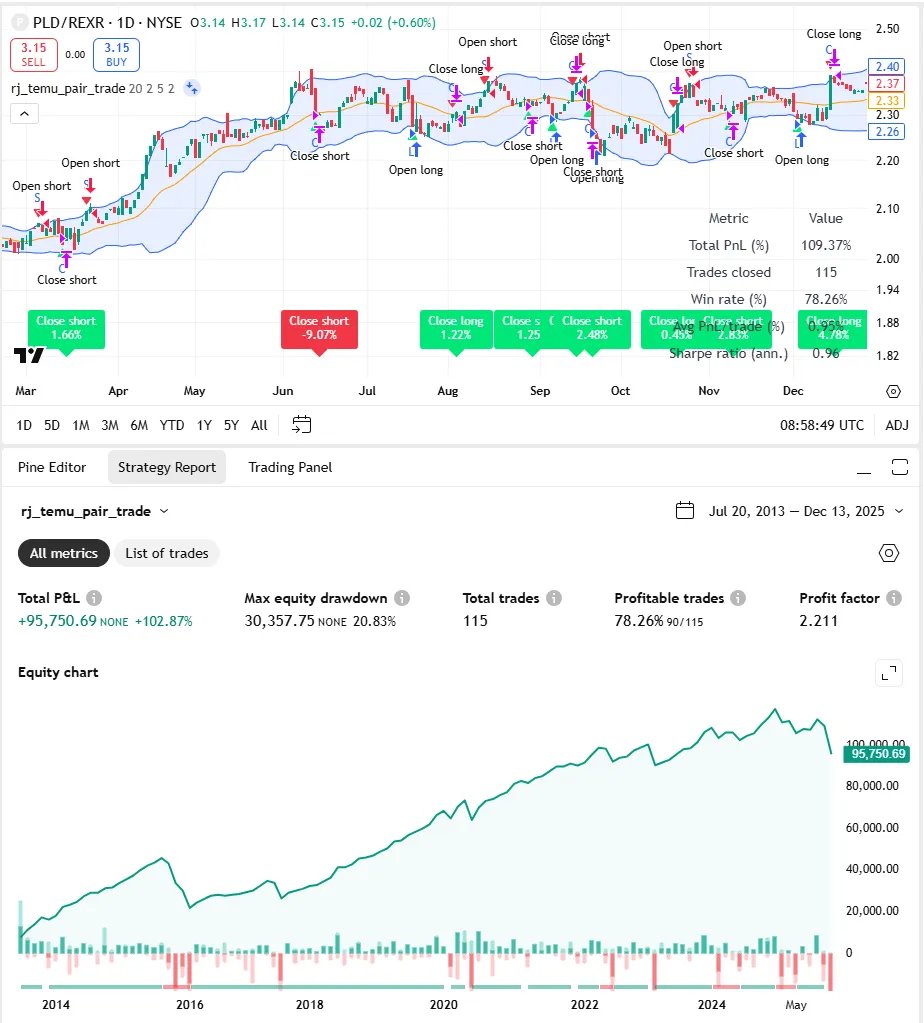

in this article i show you how a naive approach to trading this kinda works, but is strewn with blow up risk.

in this article i show you how a naive approach to trading this kinda works, but is strewn with blow up risk.

when the proverbial excrement really hits the proverbial fan, a lot of shit starts dislocating in very clear and obvious ways.

when the proverbial excrement really hits the proverbial fan, a lot of shit starts dislocating in very clear and obvious ways. like everything i share, it’s going to be very straightforward.

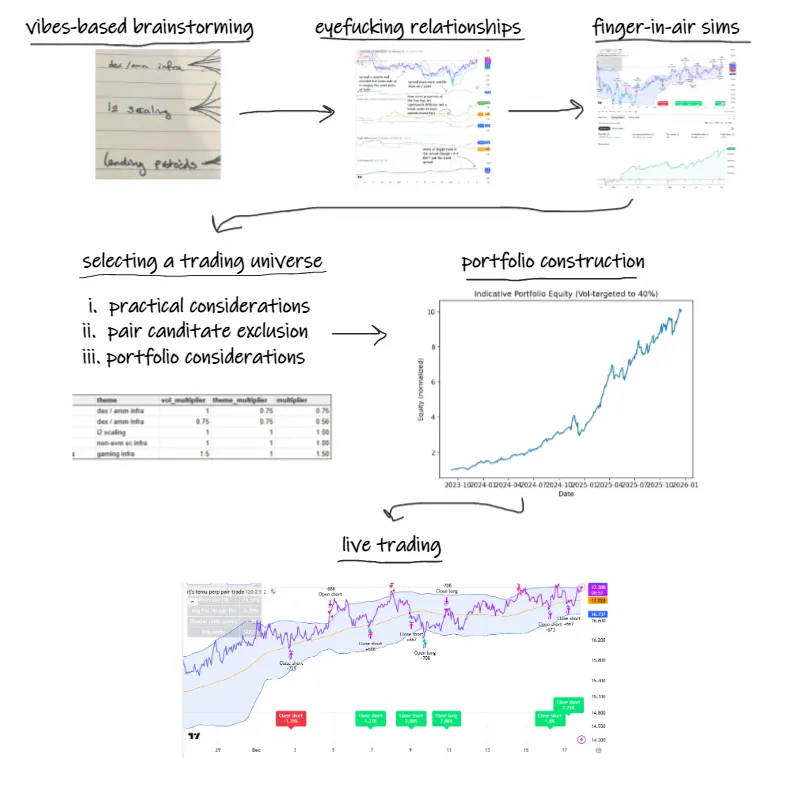

like everything i share, it’s going to be very straightforward. i’m going to tell you what pairs trading is.

i’m going to tell you what pairs trading is.

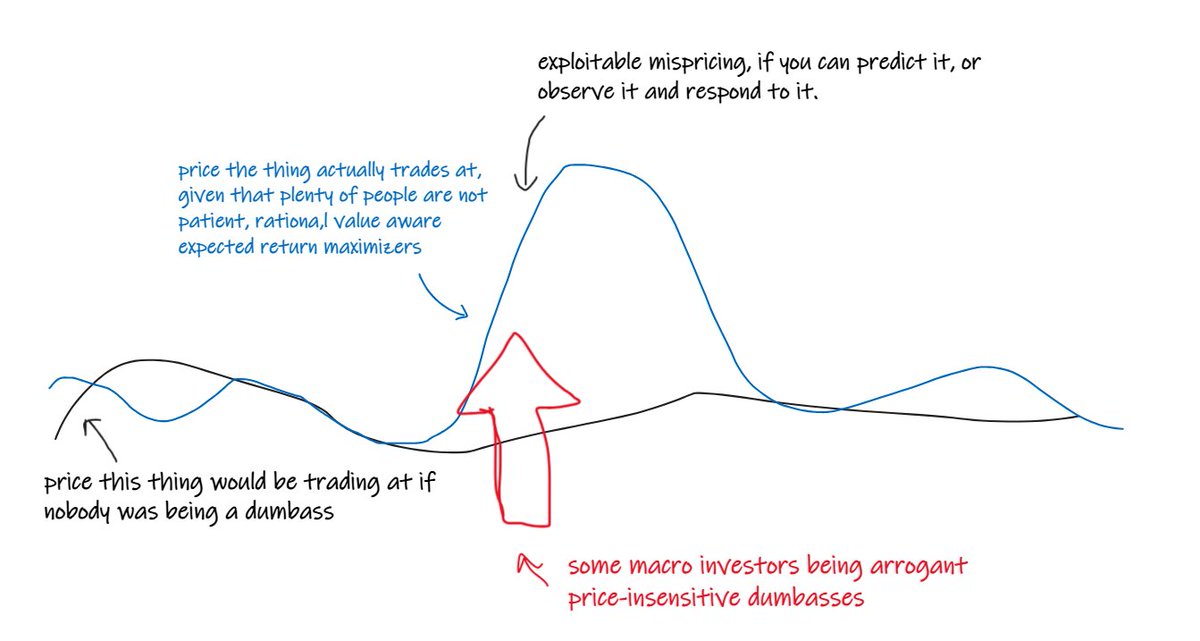

your job as trader, operating in an efficient, competitive market, is to tell yourself that your idea about that is probably bullshit.

your job as trader, operating in an efficient, competitive market, is to tell yourself that your idea about that is probably bullshit.

highlighly scientifically, i looked at etfdb and picked 15 active / tactical ETFs based on their name and category.

highlighly scientifically, i looked at etfdb and picked 15 active / tactical ETFs based on their name and category.

that the median case is to fail straight away should be self-evident.

that the median case is to fail straight away should be self-evident.