Expert in low-quality businesses.

Darkness within darkness. The gate to all mystery.

$HES EV $60B as validated by suitor $CVX.

$HES EV $60B as validated by suitor $CVX. "The move underpins the French supermajor’s plan to fast-track the exploitation of its multi-billion-barrel deep-water oil and gas find on the prolific Orange basin."

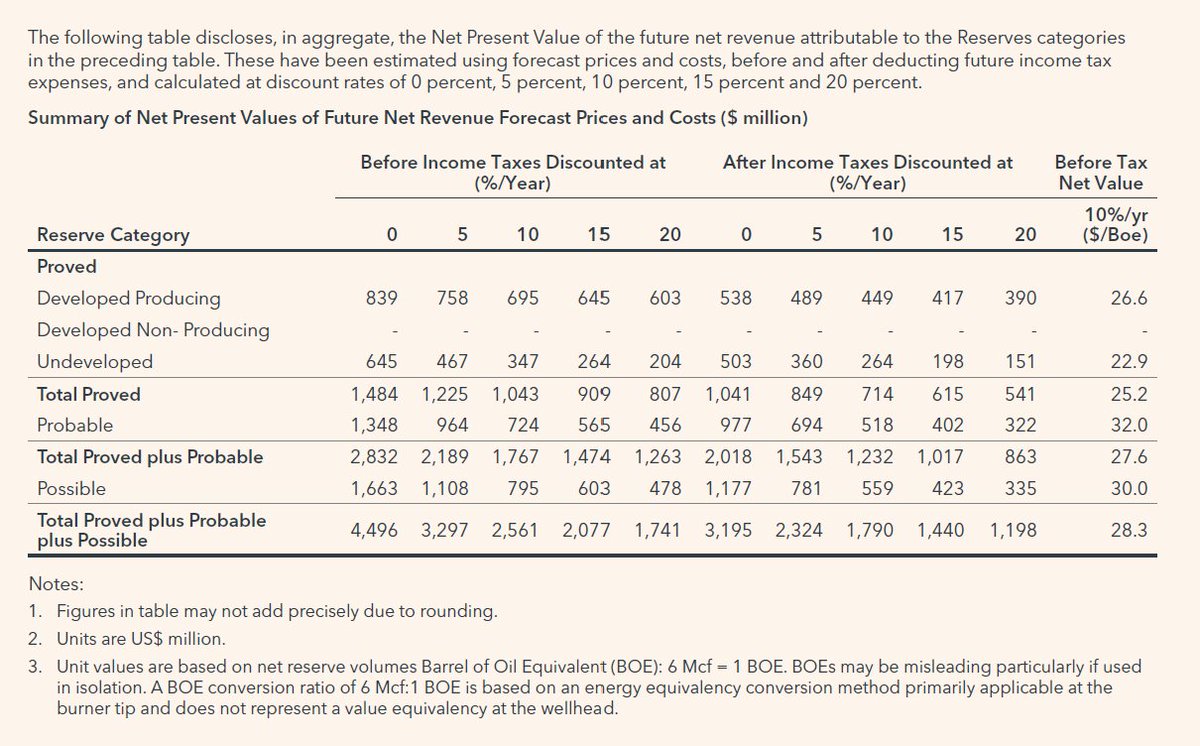

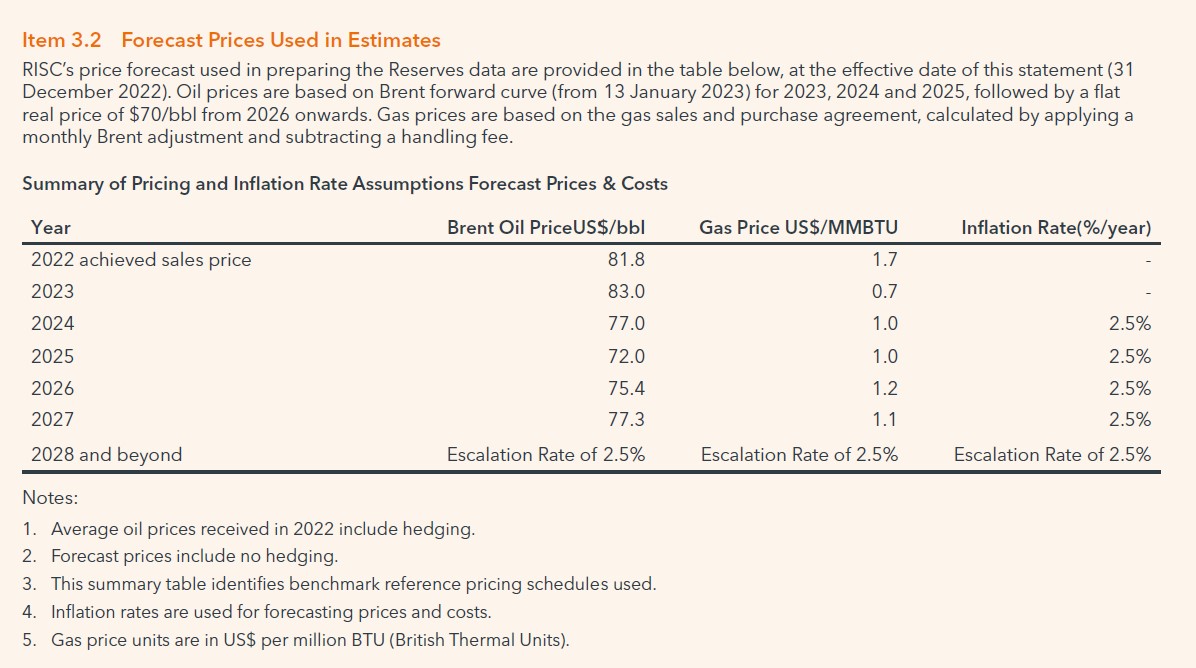

"The move underpins the French supermajor’s plan to fast-track the exploitation of its multi-billion-barrel deep-water oil and gas find on the prolific Orange basin." Here are the net oil and gas reserves of its Prime joint venture, at a conservative price deck in the mid-70s. Shall we apply a 20% discount rate for Nigeria? Let's ignore the fact that the tax rate dropped from 50% to 30% after the reserve statement, greatly boosting NPV.

Here are the net oil and gas reserves of its Prime joint venture, at a conservative price deck in the mid-70s. Shall we apply a 20% discount rate for Nigeria? Let's ignore the fact that the tax rate dropped from 50% to 30% after the reserve statement, greatly boosting NPV.

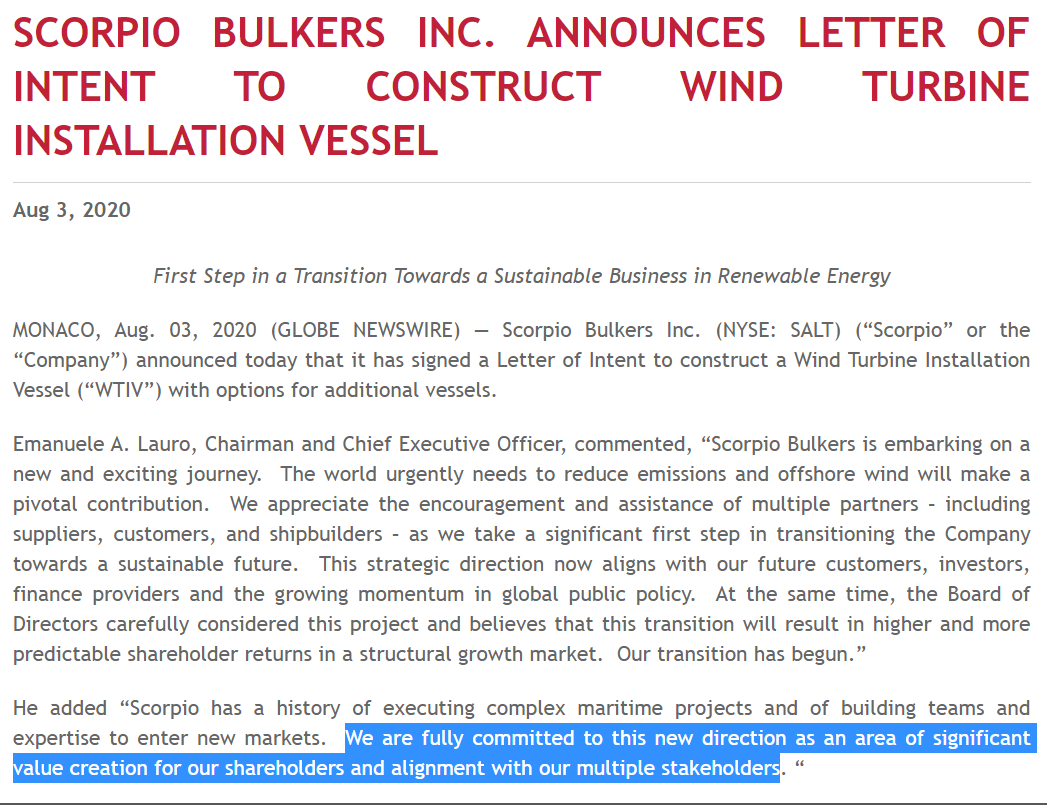

In marketing transactions to investors, neglecting costs, either implicit (e.g., cash cost of deal and time value of delaying capital returns) or explicit (e.g., opportunity cost of buyback, etc.), is a common way of varnishing them to detract from motivating agency conflicts.

In marketing transactions to investors, neglecting costs, either implicit (e.g., cash cost of deal and time value of delaying capital returns) or explicit (e.g., opportunity cost of buyback, etc.), is a common way of varnishing them to detract from motivating agency conflicts.

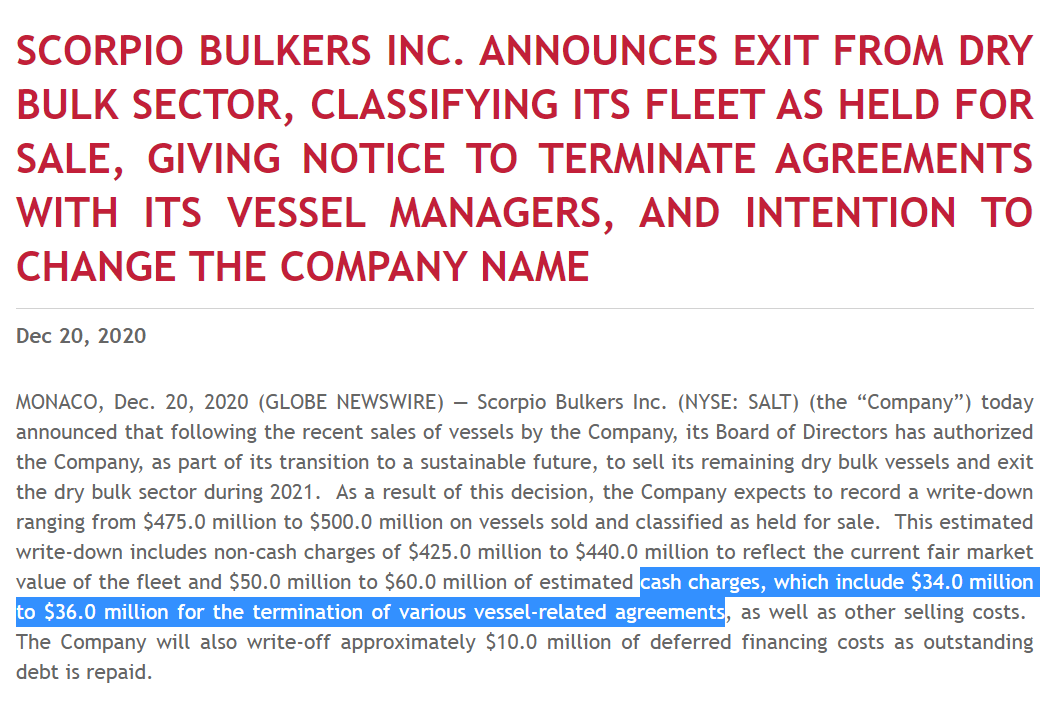

Figure 1 (2 April 2020): Form 20-F provides for "change of control fees" for termination of vessel management contract with related party. 3 months' fees unless resulting from a "change of control", stipulated to include the sale of all vessels.

Figure 1 (2 April 2020): Form 20-F provides for "change of control fees" for termination of vessel management contract with related party. 3 months' fees unless resulting from a "change of control", stipulated to include the sale of all vessels.