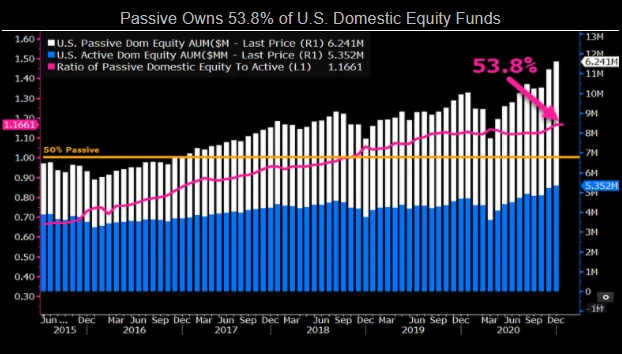

Market efficiency is created by active managers all trying to fairly value securities. Passive assumes the market is highly efficient and attempts to free-ride on it. But obviously this assumption will not hold if passive drives out the very agents enforcing it.

Market efficiency is created by active managers all trying to fairly value securities. Passive assumes the market is highly efficient and attempts to free-ride on it. But obviously this assumption will not hold if passive drives out the very agents enforcing it.