The Yes Bank scare for Mutual Funds (MFs)

Some MFs have significant exposure to subordinated/ perpetual bonds of Yes Bank. These MFs stare at huge valuation losses if the credit rating of these bonds is cut below investment grade. Thread (1/9)

Some MFs have significant exposure to subordinated/ perpetual bonds of Yes Bank. These MFs stare at huge valuation losses if the credit rating of these bonds is cut below investment grade. Thread (1/9)

The following MFs have major exposure to Basel II/ Basel III, subordinated/ perpetual bonds of Yes Bank (market value as at 31st July, 2019) -

a) Reliance Nippon ~ Rs. 2150 Cr.

b) Franklin Templeton ~ Rs. 540 Cr.

c) UTI ~ Rs. 445 Cr.

d) Kotak ~ Rs.115 Cr.

2/9

a) Reliance Nippon ~ Rs. 2150 Cr.

b) Franklin Templeton ~ Rs. 540 Cr.

c) UTI ~ Rs. 445 Cr.

d) Kotak ~ Rs.115 Cr.

2/9

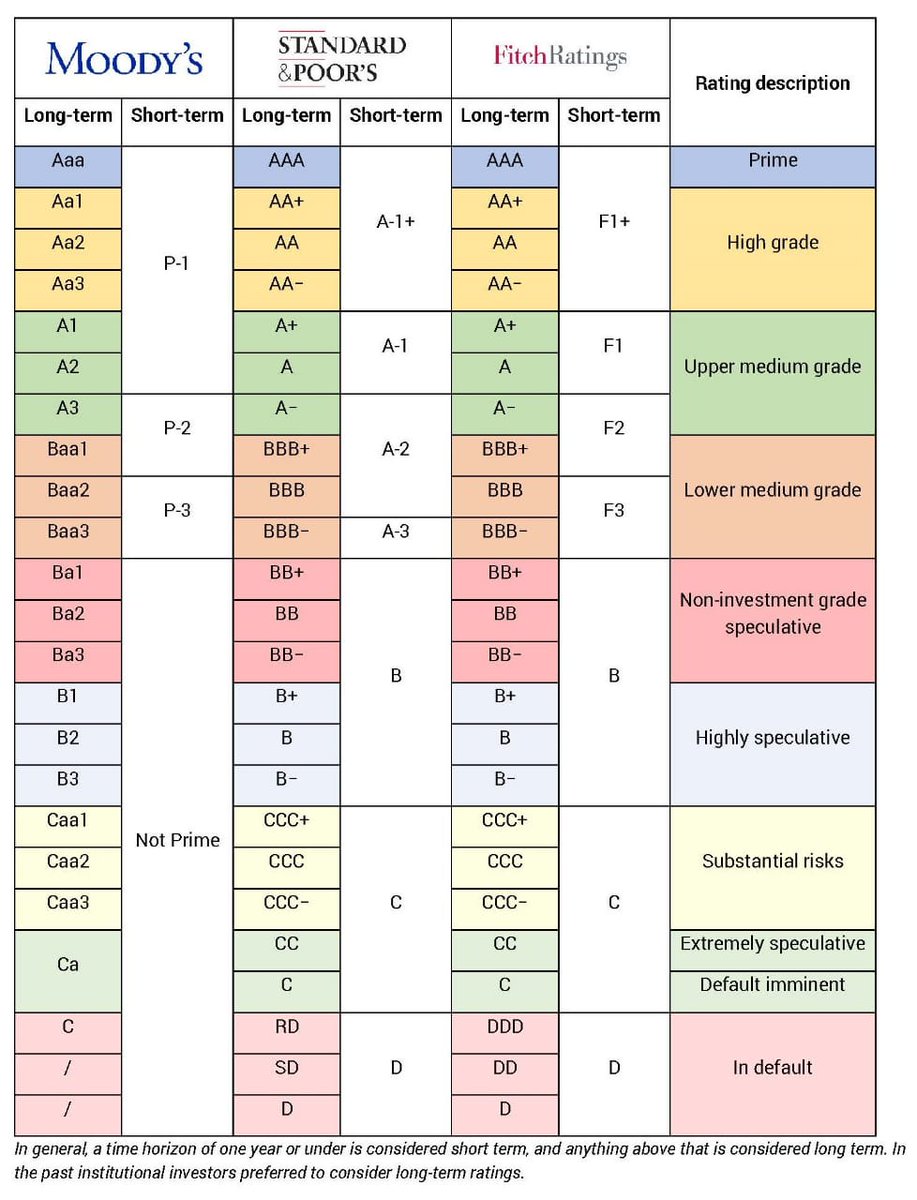

The Credit Rating of Yes Bank Basel III Perpetual (Tier I or AT1) bonds have been downgraded thrice by ICRA in a span of 9 months.

a) Nov 24, 2018 - downgraded to AA- from AA.

b) May 03, 2019 - downgraded to A from AA-.

c) July 24, 2019 - downgraded to BBB from A.

3/9

a) Nov 24, 2018 - downgraded to AA- from AA.

b) May 03, 2019 - downgraded to A from AA-.

c) July 24, 2019 - downgraded to BBB from A.

3/9

There are 2 major threats that the investors of the above MFs face in case the weakening in credit profile of Yes Bank prolongs.

1) If the credit rating goes below BBB-, MFs will slash the value of bonds by 25-100% passing on significant valuation losses to investors.

4/9

1) If the credit rating goes below BBB-, MFs will slash the value of bonds by 25-100% passing on significant valuation losses to investors.

4/9

2) Subordinated/ Perpetual bonds are akin to equity and hence have rights inferior to senior bonds. E.g. a bank that had issued Basel III perpetual (AT1) bonds, can skip coupon, write down value of bonds or convert bonds to equity if the financial condition deteriorates. 5/n

This implies that if the bank slips into a 'near bankruptcy' situation, the rights and returns on these bonds held by MFs would suffer drastically. Further, in any debt settlement process these MFs would be the last in queue owing to the inferior stature of these bonds. 6/n

In addition to Subordinated/ Perpetual debt of Yes Bank, a couple of MFs, also hold promoter debt of Yes Bank viz.

a) Reliance MF - Rs. 700 Cr (Morgan Credits)

b) Franklin MF- Rs. 300 Cr (Yes Capital)

These promoter structures rely heavily on the price of Yes Bank shares. 7/9

a) Reliance MF - Rs. 700 Cr (Morgan Credits)

b) Franklin MF- Rs. 300 Cr (Yes Capital)

These promoter structures rely heavily on the price of Yes Bank shares. 7/9

A credit event in Yes Bank could push down the share price significantly which in turn would weaken the credit profile of Yes Bank promoter debt. 8/9

However, let me qualify my comments by stating that Yes Bank, in a recent equity raise, was able to mobilise ~ Rs. 2000 Cr. If the bank is able to attract more equity capital, all the apprehensions expressed above would be unfounded. 9/9

@kayezad @ActusDei @_soniashenoy @andymukherjee70 @invest_mutual @BMTheEquityDesk @dmuthuk @rohitchauhan @contrarianEPS @shyamsek @chokhani_manish @pvsubramanyam @BalakrishnanR @Sanjay__Bakshi @TamalBandyo @CafeEconomics @menakadoshi @latha_venkatesh @AmolPlanRupee @deepakshenoy

@dugalira @Iamsamirarora @SunilBSinghania @mrinagarwal @IamMisterBond @NagpalManoj @SalariedTaxpay1 @YashwantSinha @ayushmitt

#MutualFundsSahiHai #mutualfunds #bondmarket #CreditRiskFund #mutualfunds #bonds #perpetualbond #yesbank #subordinatedbonds #RelanceNippon #FranklinTempleton

@threadreaderapp unroll

• • •

Missing some Tweet in this thread? You can try to

force a refresh