Rana Kapoor's Grandstanding

The Economic Times, today, on its front page, carried a news item proclaiming 'Rana Kapoor holding companies pre-pay part of loans'. Nothing can be more misleading than the use of word 'pre-pay'. Thread 1/8

m.economictimes.com/markets/stocks…

The Economic Times, today, on its front page, carried a news item proclaiming 'Rana Kapoor holding companies pre-pay part of loans'. Nothing can be more misleading than the use of word 'pre-pay'. Thread 1/8

m.economictimes.com/markets/stocks…

The article quotes Mr. Kapoor's statement that bonds issued by promoter hold cos - Yes Capital and Morgan Credits, have been pre-paid ahead of maturity dates i.e. Oct 2020 and Apr 2021 respectively. 2/8

The clever use of 'maturity date' to imply voluntary prepayment hides the fact that these facilities were probably pre-paid owing to the pressure of fund managers (Franklin and Reliance MF) on account of failure of these hold cos to meet the obligations under the facility. 3/8

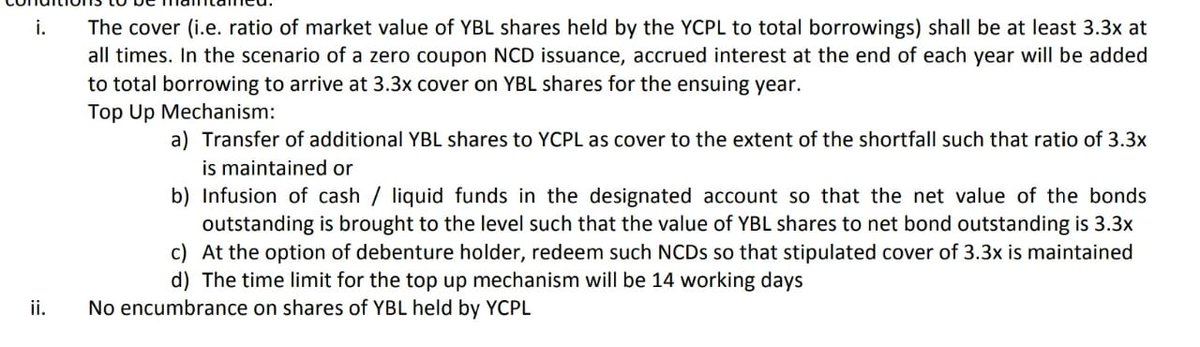

The conditions set out in the terms of the facilities (captured by credit rating rationales) have been breached many times since Sept 2018. The cures stipulated for breach were transferring additional Yes Bank shares or infusion of cash. None of these cures was done on time. 4/8

Further, both these facilities - Yes Capital and Morgan Credits, had embedded PUT options. For Morgan Credits facility there is a PUT option every three months while for Yes Capital facility, there was a PUT option in March, 2019. 5/8

A PUT option is an option with investors to exit a debt facility. With so many breaches in the facility, it would be quite startling that the Fund Managers holding these securities would not have sought to exit especially since these facilities yield a mere 9-9.5% p.a.. 6/8

It is common knowledge that when a debt facility is in jeopardy, the fund managers engage informally with issuers to resolve the issue. Usually strong arm tactics of threatening to exercise the PUT option or calling an 'Event of Default' is used to get the money back. 7/8

So, if on account of breaches in the facilities, a fund manager pressurises an issuer to give the money back and the issuer complies reluctantly, it cannot not be termed as pre-payment. Mr. Kapoor is trying to make a virtue of a necessity. 8/8

@kayezad @ActusDei @_soniashenoy @andymukherjee70

@invest_mutual @BMTheEquityDesk @rohitchauhan

@contrarianEPS @shyamsek @chokhani_manish @pvsubramanyam @BalakrishnanR @Sanjay__Bakshi

@TamalBandyo @TheMFGuy1 @CafeEconomics

@menakadoshi @latha_venkatesh

@AmolPlanRupee

@invest_mutual @BMTheEquityDesk @rohitchauhan

@contrarianEPS @shyamsek @chokhani_manish @pvsubramanyam @BalakrishnanR @Sanjay__Bakshi

@TamalBandyo @TheMFGuy1 @CafeEconomics

@menakadoshi @latha_venkatesh

@AmolPlanRupee

@deepakshenoy @dugalira @Iamsamirarora

@SunilBSinghania @mrinagarwal @IamMisterBond

@NagpalManoj @SalariedTaxpay1 @YashwantSinha

@ayushmitt @prashantmET @NishanthV_ET @malinibhupta @dhirendra_vr @rachitaprasadET @PankajMathpal @babarzaidiET @jashkriplani @larissafernand

@SunilBSinghania @mrinagarwal @IamMisterBond

@NagpalManoj @SalariedTaxpay1 @YashwantSinha

@ayushmitt @prashantmET @NishanthV_ET @malinibhupta @dhirendra_vr @rachitaprasadET @PankajMathpal @babarzaidiET @jashkriplani @larissafernand

#RanaKapoor #YesBank #MorganCredits #YesCapital #RelianceNippon #FranklinTempleton #promoter #debt #debentures

@threadreaderapp unroll

• • •

Missing some Tweet in this thread? You can try to

force a refresh