A lot of folks are talking about #ITC these days and I have also seen some specific concerns which people raise again and again when the name of the company is taken.

I have tried to highlight some important facts which revolve around these concerns..

I have tried to highlight some important facts which revolve around these concerns..

1. Cigarette Business has become weak

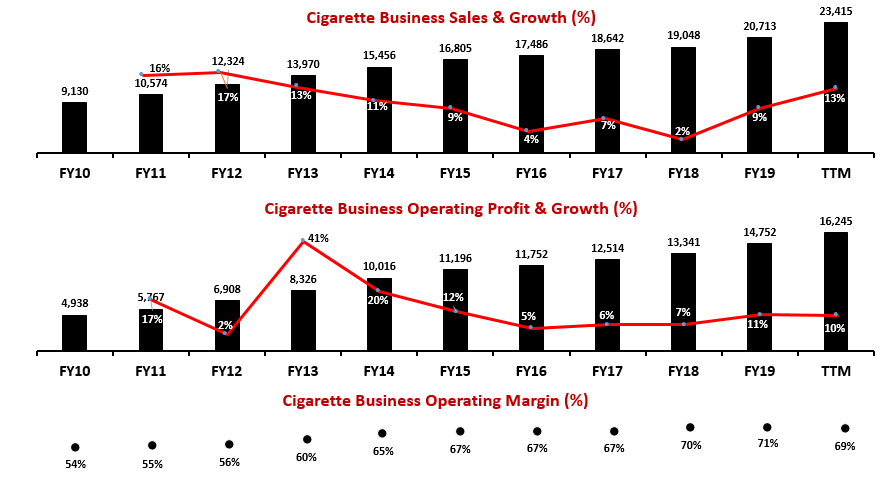

Cigarette business is and continues to remain a very strong cushion which lets #ITC go out and take risks. It gives the company a tremendous capacity to suffer.

Here is what history has to say..

Cigarette business is and continues to remain a very strong cushion which lets #ITC go out and take risks. It gives the company a tremendous capacity to suffer.

Here is what history has to say..

2. Diworsification - Hotel Business

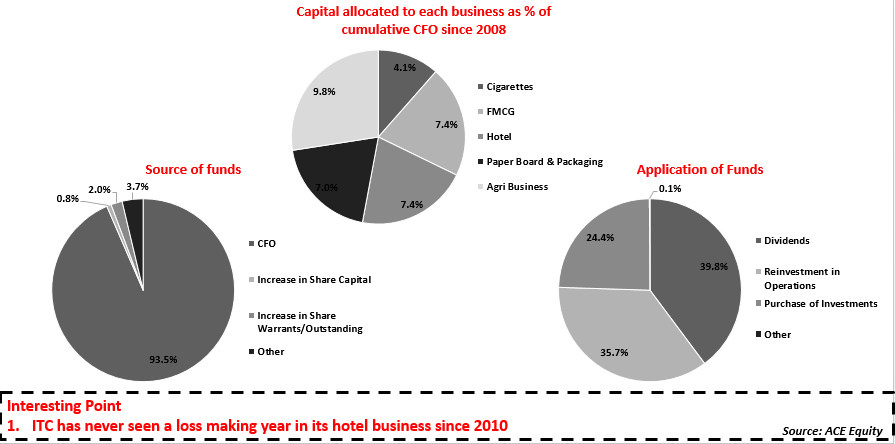

Hotel is not regarded as a good business among investors, because low ROCE.. But the question is, is it worth focusing too much upon in context of ITC? #ITC has only invested 7% of its cumulative CFO into the hotel business since 2008.

Hotel is not regarded as a good business among investors, because low ROCE.. But the question is, is it worth focusing too much upon in context of ITC? #ITC has only invested 7% of its cumulative CFO into the hotel business since 2008.

3. Foreign investors are selling!

Yes, that is true but their holding still stays at Median

Also, steep graph of DIIs' says that they have not only absorbed the pressure but have bought even more.

NOTE: Insurance companies dominate the DII holding

Yes, that is true but their holding still stays at Median

Also, steep graph of DIIs' says that they have not only absorbed the pressure but have bought even more.

NOTE: Insurance companies dominate the DII holding

4. FMCG Business is not doing anything

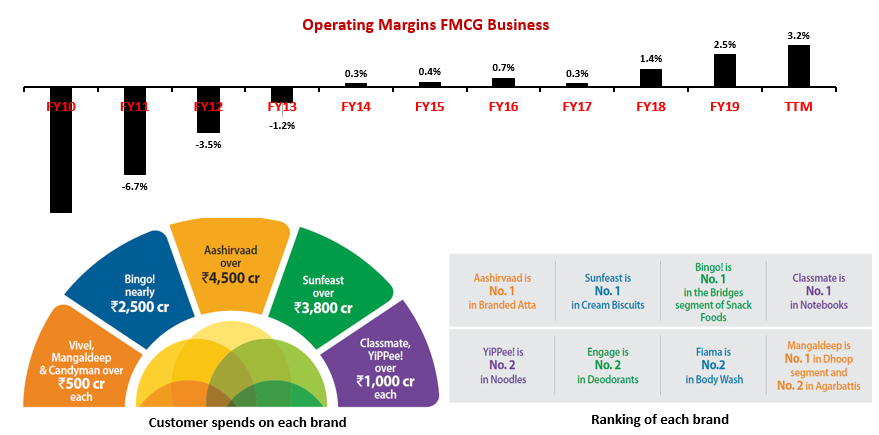

FMCG part of #ITC has been under pressure but it has started to show a lot of promise.

FMCG should become more stable and promising. Not to forget the powerful innovation engine which powers FMCG.

FMCG part of #ITC has been under pressure but it has started to show a lot of promise.

FMCG should become more stable and promising. Not to forget the powerful innovation engine which powers FMCG.

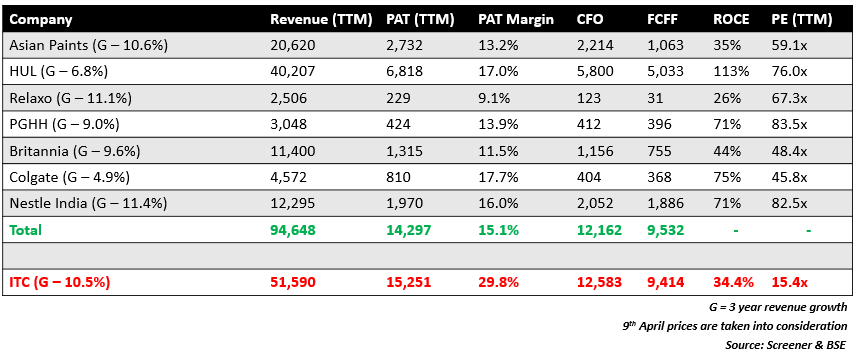

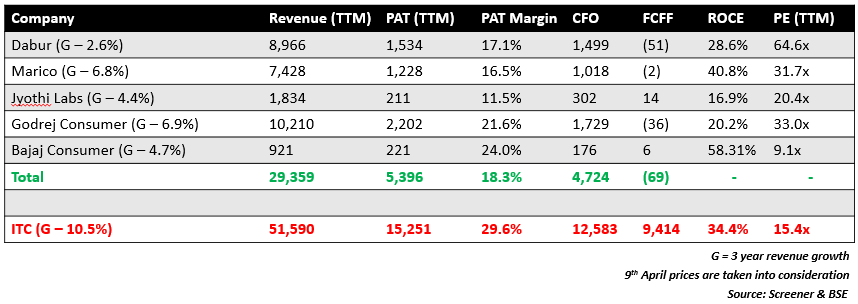

5. ITC is not able to grow like the darlings of the market!

Basic comparison with market darlings shows that #ITC is not lagging behind in terms of growth or any other parameter, baring 2 companies (Still the difference is less than 2%)

But Valuations..

Basic comparison with market darlings shows that #ITC is not lagging behind in terms of growth or any other parameter, baring 2 companies (Still the difference is less than 2%)

But Valuations..

While doing this comparison, I thought it will be interesting to compare #ITC with companies which have lagged behind in growth. Result pertaining to other parameters wasn't surprising.

But Valuations..

But Valuations..

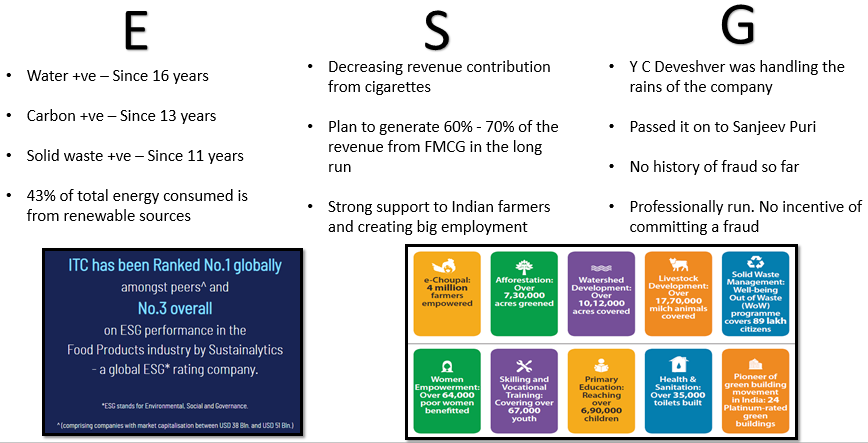

6. ESG Concerns

Yes, Cigarette can be a socially questionable business but isnt #ITC doing the right thing by moving away from the business?

But they are actually doing a lot of things which ticks the ESG box. In fact, most of the companies globally fail to meet ITC’s standards

Yes, Cigarette can be a socially questionable business but isnt #ITC doing the right thing by moving away from the business?

But they are actually doing a lot of things which ticks the ESG box. In fact, most of the companies globally fail to meet ITC’s standards

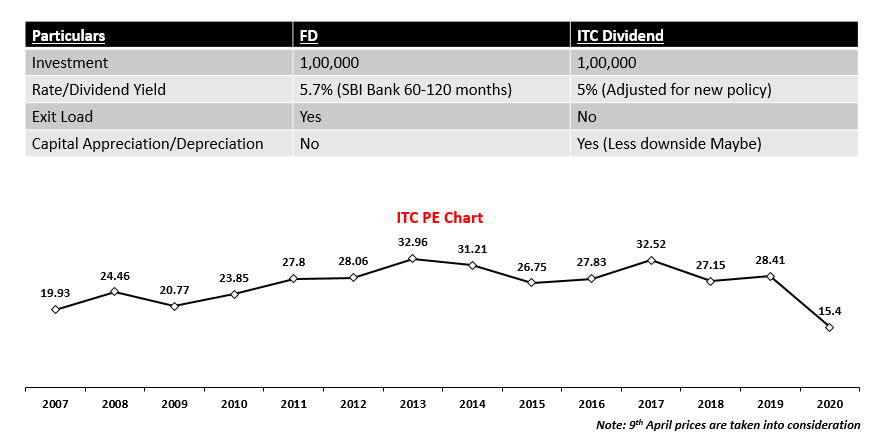

After taking the new dividend distribution policy into account, buying #ITC is like buying an undervalued stock + FD as it offers an attractive 5% dividend yield which is roughly doing an FD with SBI for 60 – 120 months.

ITC is currently at the lowest PE since 2007.

ITC is currently at the lowest PE since 2007.