In the last tweet thread, we talked about Option Greek Delta. In this thread, we will talk about Option Greek Gamma which is closely related to Delta (∆).

When underlying price moves with respect to a particular option strike, that particular option strike becomes either in-the-money or out-of-the-money and thus changing the Delta of the option. This change in Delta can be explained by Option Greek ‘Gamma’.

Gamma (denoted as γ) is the options Greek that tells us the rate of change of the options delta in response to the change in the underlying price. More specifically, gamma tells us about the options expected delta change relative to a one-point change in the underlying.

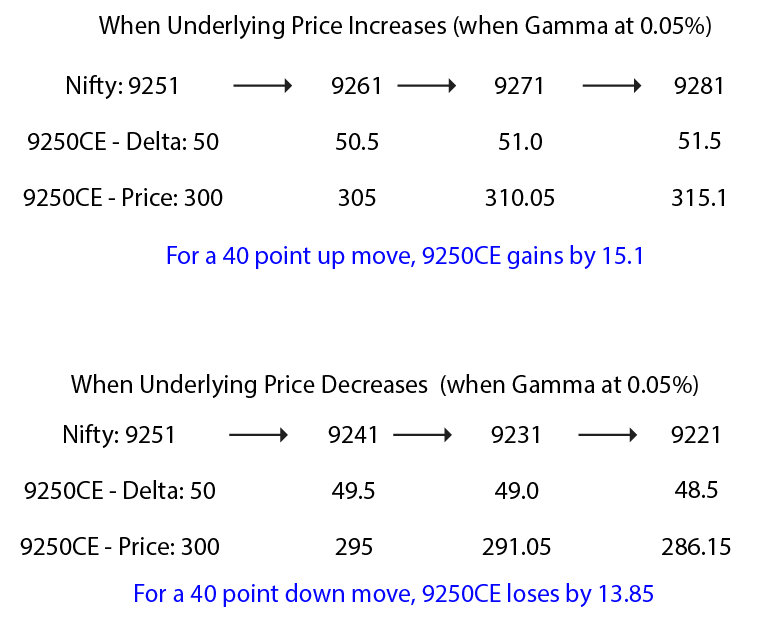

For eg., with Nifty at 9251, a 9250CE strike will have a delta of 50. If the gamma of the strike is 0.05%, then for every 1-pt up move in the underlying, the delta of the 9250CE strike becomes 50.05 (50+0.05) and for a 100-pt up move, the delta becomes 55 (50+100*0.05)

Thus, ∆ increase also affects the options price. The 9250CE price increases at a rate of 50% (∆ of the option) of the underlying increase. And after a 100-point up move, the 9250CE options price will increase at a rate of 55%, which is equal to the new ∆ of 55.

Conversely, if underlying moves down, the ∆ of the call option decreases & eventually becomes out-of-the-money.

As underlying moves up, the ∆ of the call options change faster while ∆ changes slowly when the underlying moves down. This is better illustrated in the fig below.

As underlying moves up, the ∆ of the call options change faster while ∆ changes slowly when the underlying moves down. This is better illustrated in the fig below.

Put options also work in a similar fashion. Since puts have a negative delta, when there is an up move in the underlying, the delta of the put option decreases by the amount of gamma of the option for every point change in the underlying price.

As the underlying price keeps increasing, the put options go further out-of-the-money with a resultant lower delta. Conversely, if underlying moves down, the delta of the put option increases and eventually becomes in-the-money.

When a trader buys options, he accumulates positive gamma and when a trader sells options, he accumulates negative gamma. Gamma causes the options to gain value faster and lose their value slower due to its effect on the delta.

As a result, gamma helps the option buyer as it increases the option value faster if underlying moves in his favor and lose its value slower when underlying moves against the trader.

Gamma works against the option seller as the value of the option moves to zero at a slower rate due to negative γ. The option seller accumulates losses faster if the underlying moves against him. For this reason, option selling is to be avoided like a plague when γ is high.

Delta is a first-order derivative of the value of the option with respect to the underlying price while Gamma is a second-order derivative of the same.

Just like delta, which not only changes but changes with a different rate in response to the underlying price change, gamma also changes and is not a constant. Moneyness, time to expiration, and volatility of the option all affect the gamma of the option.

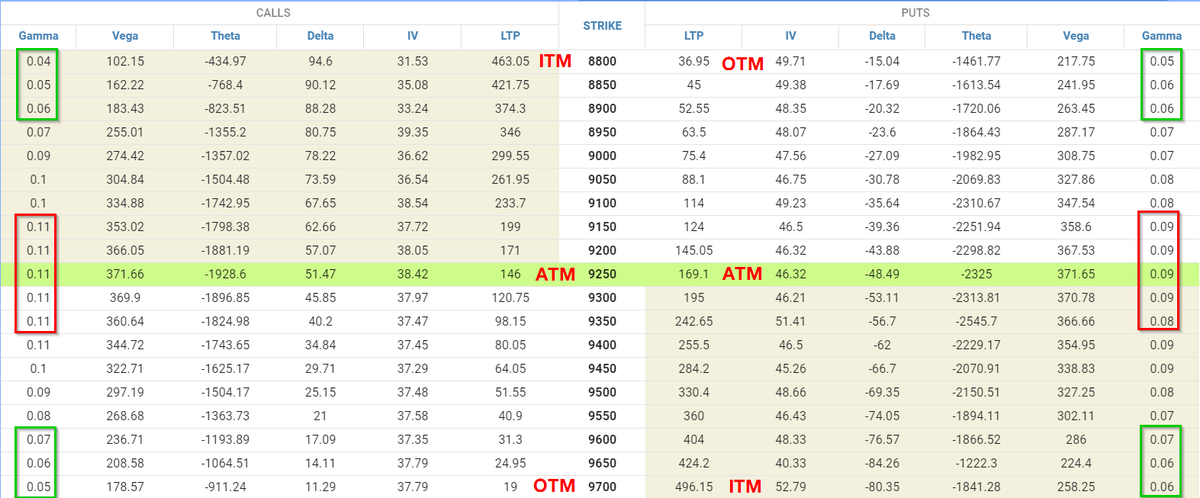

ITM options with ∆ close to 100 & OTM options with ∆ close to zero change their value at a very slow rate with respect to small underlying price changes. But ATM options have a higher sensitivity to smaller changes in underlying price due to a faster change of delta.

This phenomenon is explained by the fact that ITM and OTM options have lower gamma while ATM options have higher gamma thus changing the delta at a faster rate for the ATM options. This is illustrated in the option chain given in the figure.

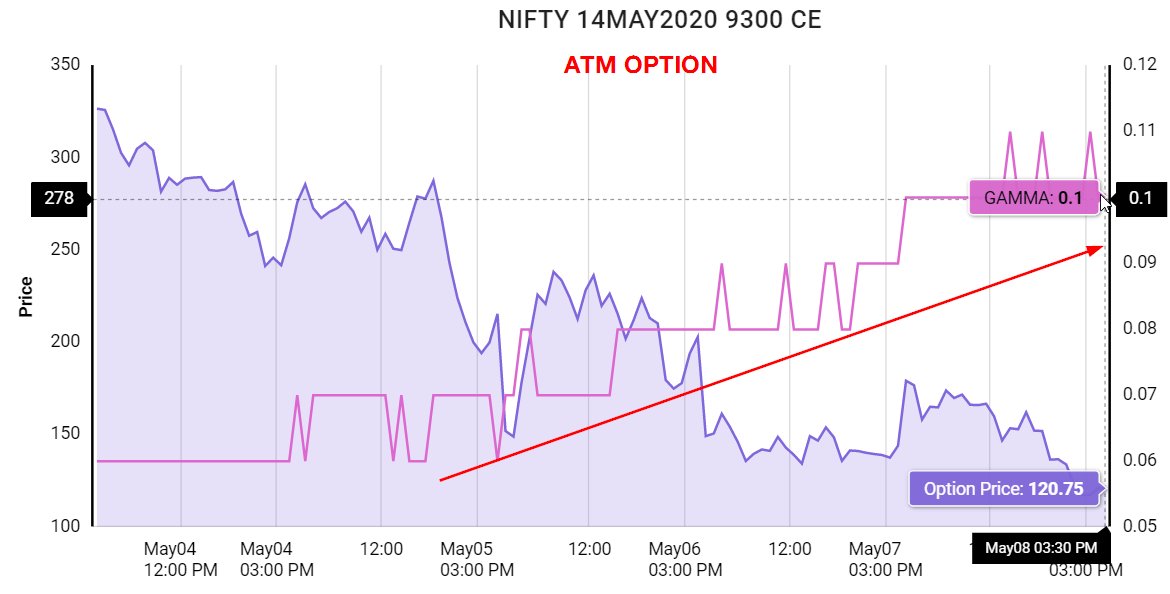

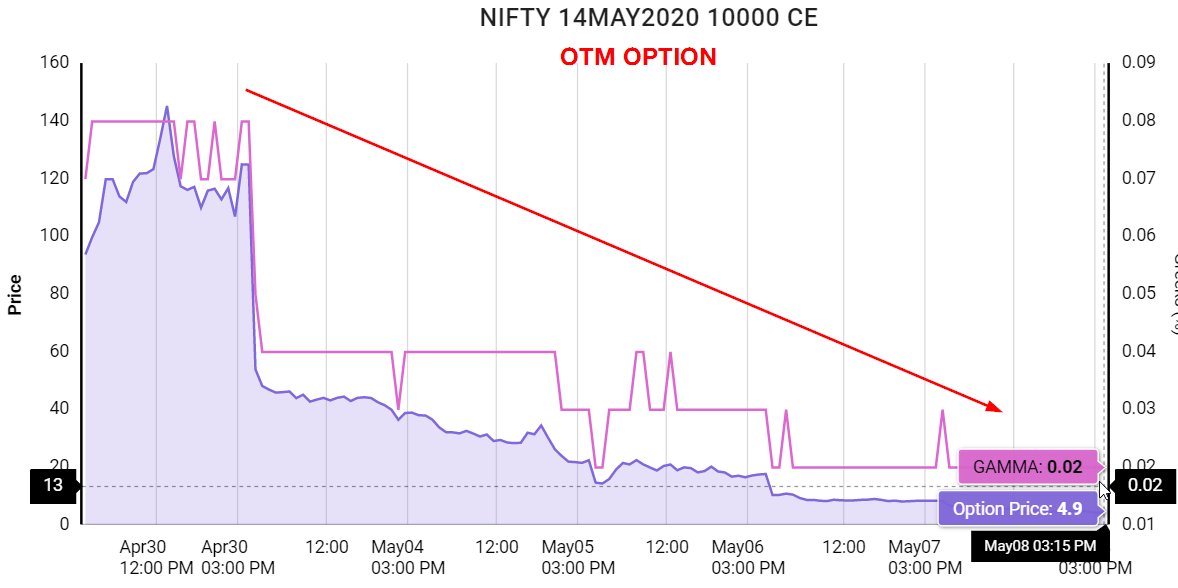

As we approach closer to expiry, the certainty of OTM and ITM options remaining OTM & ITM increases while the moneyness of ATM options remains uncertain and as a result, ATM options have higher gammas.

Therefore, when the expiration of the options near, the gamma of ITM and OTM options decrease while the gamma of ATM options increases.

This is illustrated by the Gamma charts of ATM and OTM options of NIFTY 14May2020 expiration in the figures below.

This is illustrated by the Gamma charts of ATM and OTM options of NIFTY 14May2020 expiration in the figures below.

Because of the higher gamma of ATM options closer to the expiry, an ATM option seller can quickly make losses due to faster change in delta and value of the option if the underlying moves against the trade. This is called ‘The Gamma Effect’.

It is advised to all the traders who sell options as a strategy to roll over their positions to the next expiration to avoid the gamma effect and cut the risk of a larger unfavorable underlying move.

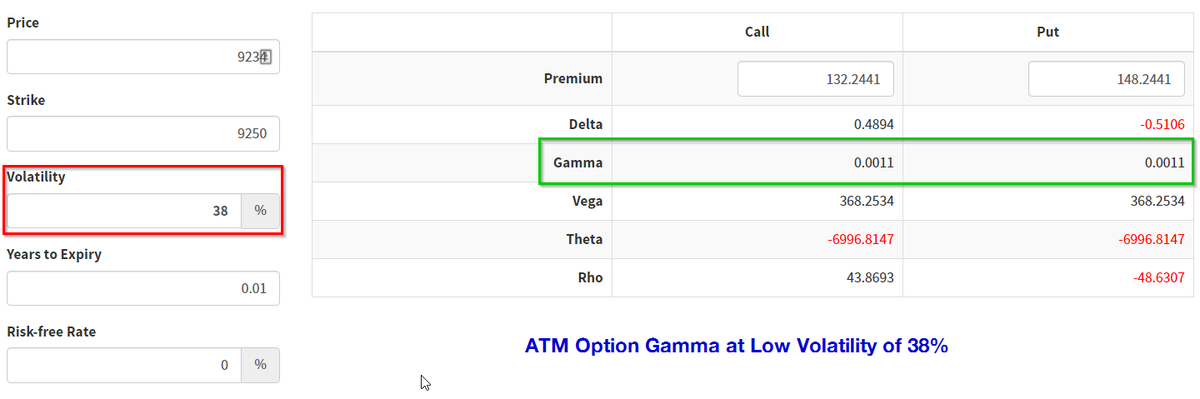

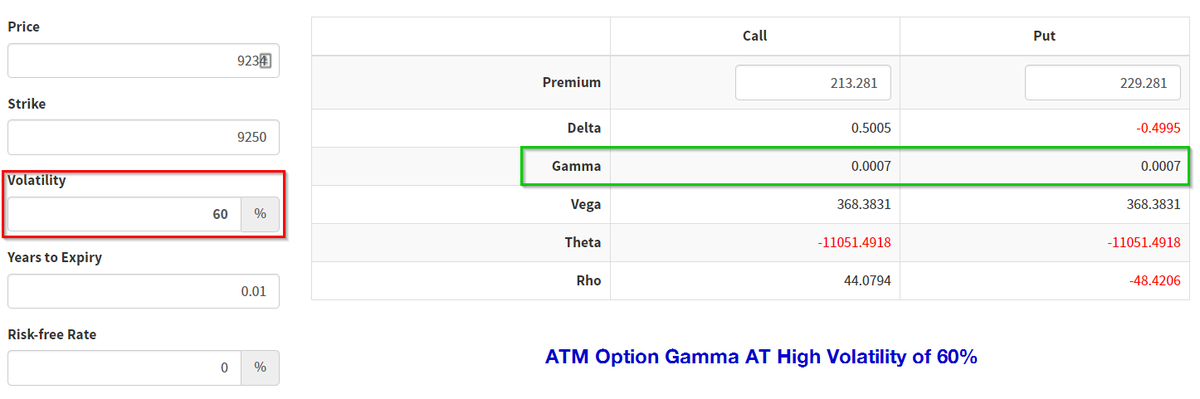

Under normal conditions, ATM strikes have the highest gamma, and OTM and ITM options have the lowest γ. But when there is an increase in the volatility, it causes the gamma curve to flatten causing the decrease in the γ of ATM strikes and an increase in the γ of OTM & ITM strikes

This can be illustrated with the ATM strike gamma at two different volatilities.

Forgot to link Delta thread in the first post.

This is the link to Delta tread

This is the link to Delta tread