1. Folks I got a tax policy paper out today. This one's not about COVID; more about the recent past and the long term.

I do not like the mortgage interest deduction, and I especially do not like it at the higher end of the housing price distribution.

jec.senate.gov/public/index.c…

I do not like the mortgage interest deduction, and I especially do not like it at the higher end of the housing price distribution.

jec.senate.gov/public/index.c…

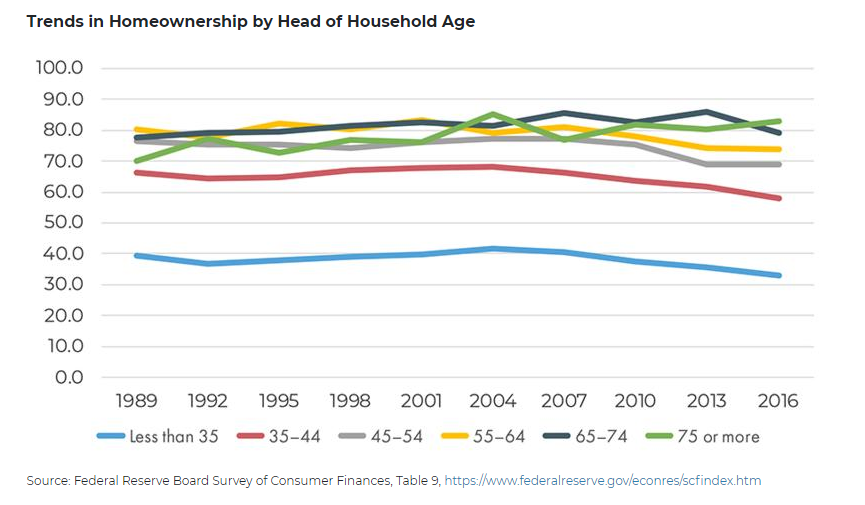

2. But let's back up before we get to that and talk about homeownership generally. It's good for a variety of reasons (mostly, aligning the interests of owner and occupant is great!) and people who aspire to it should get to do it.

But some age groups--the under 45s--struggle.

But some age groups--the under 45s--struggle.

3. Note that they lost ground on this throughout the 2009-2020 expansion(!). It's not just about the 2009 crisis, there's something structural going on that makes it tougher for the younger people--but not so much for the older people, who are owning as much as they always did.

4. If you care about parenthood, also, it's worth noting that 99.75% of kids are delivered by someone under 45.

It's not so much that the owner/renter distinction is important for this in itself, but owner-occupied homes are more likely to have extra bedrooms to give to kids.

It's not so much that the owner/renter distinction is important for this in itself, but owner-occupied homes are more likely to have extra bedrooms to give to kids.

5. Main reason for the struggle: the prices! The green is the simple median, and the blue is a metric that attempts to adjust for quality by looking at repeat sales.

Prices have risen 2.5x since 1989. A little less if you give them credit for extra quality.

Prices have risen 2.5x since 1989. A little less if you give them credit for extra quality.

6. There are two main ways to pay: up front (down payment) and in monthly installments (mortgage payment.)

The up-front cost you pay with existing wealth; the monthly installments, with future income.

How have people's abilities to pay each of these changed over time?

The up-front cost you pay with existing wealth; the monthly installments, with future income.

How have people's abilities to pay each of these changed over time?

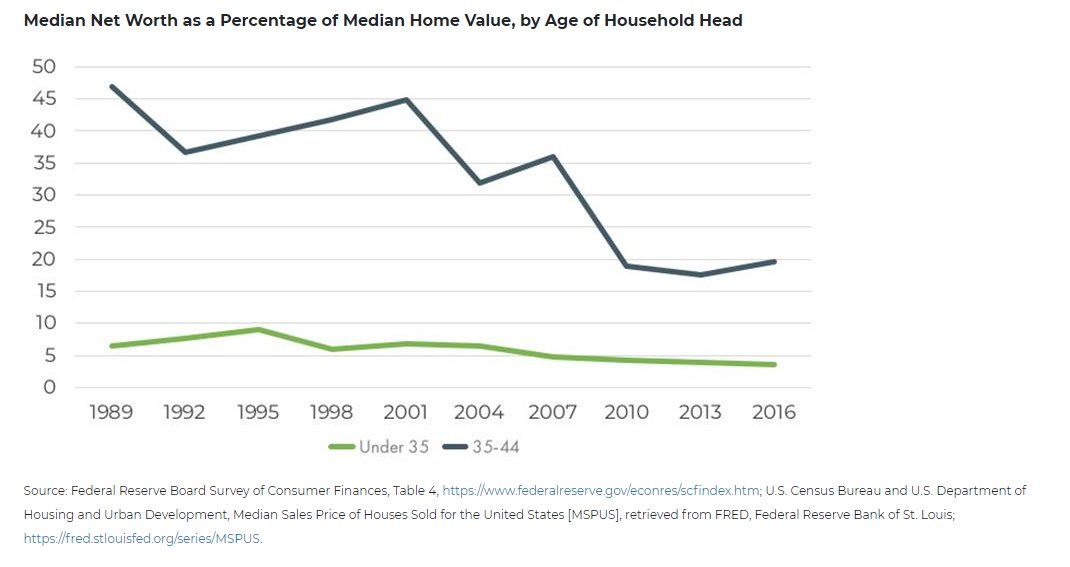

7. This is median net worth as % of median home value.

Think of it as the max down payment the median young household could put on the median home if they used every cent.

Net worths haven't kept pace with prices, mostly because careers start later and prices increased fast.

Think of it as the max down payment the median young household could put on the median home if they used every cent.

Net worths haven't kept pace with prices, mostly because careers start later and prices increased fast.

8. (There are some other things going on too. Marriages start later, which generally makes it harder to buy. But I'm not personally gonna go out and tell people to get married, I'm just trying to work with the families we have here, and stay in my tax policy lane.)

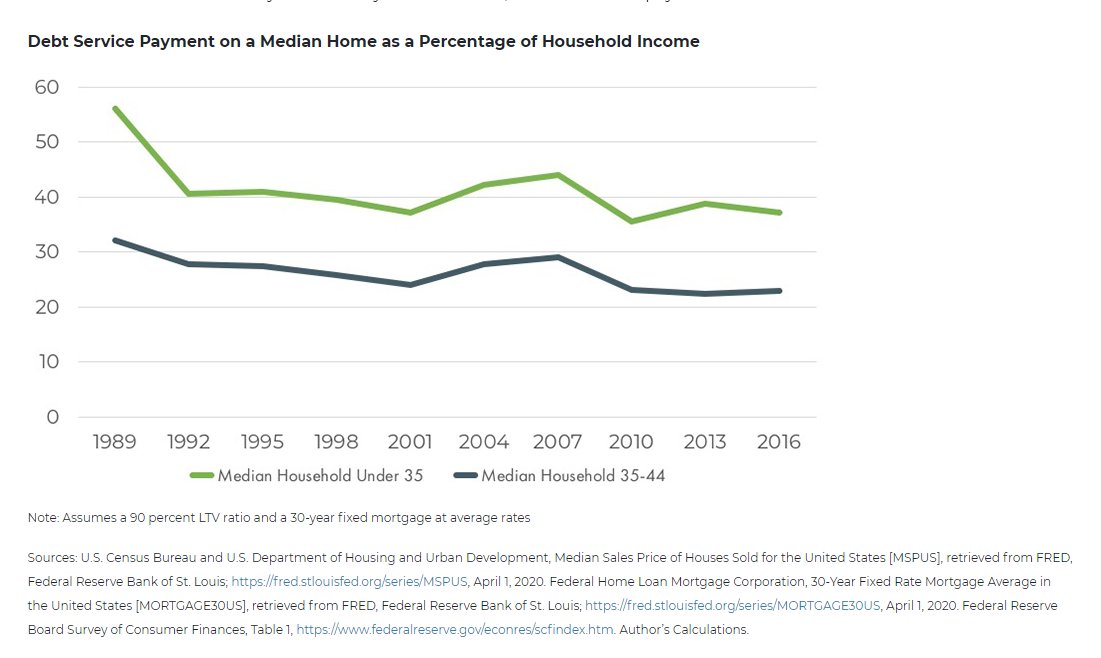

9. When it comes to the monthly payments (as opposed to the down payments) people are really doing pretty okay.

Two reasons:

1. Interest rates have come way, way down.

2. Incomes have risen.

This is more than enough to offset the greater sticker price.

Two reasons:

1. Interest rates have come way, way down.

2. Incomes have risen.

This is more than enough to offset the greater sticker price.

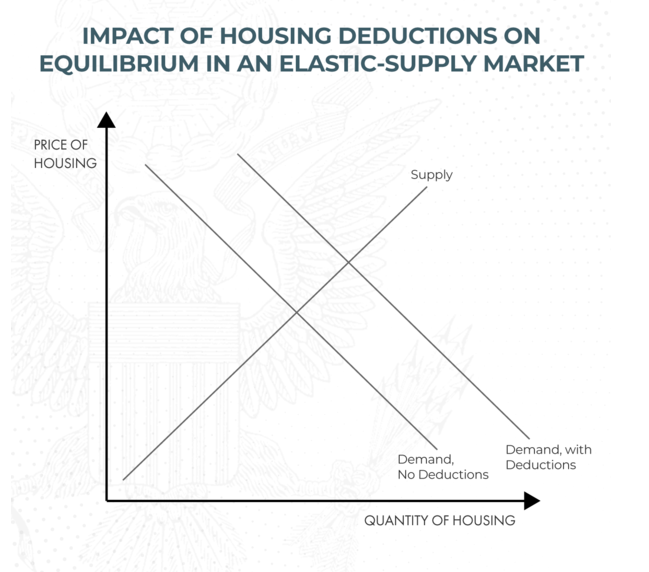

10. So how does this tie into the mortgage interest deduction? (And related: property tax deduction.) Consider the first-order effect: these deductions help on the monthly payment, not the down payment!

At best, this is mistargeted help: on the easier part, not the tough part.

At best, this is mistargeted help: on the easier part, not the tough part.

11. But it gets worse when you consider the second and third order effects. All buyers become more willing to pay for houses.

(There's some math for this in a theoretical model, but common sense works too. Of course you'll pay more if the purchase gets you some tax deductions.)

(There's some math for this in a theoretical model, but common sense works too. Of course you'll pay more if the purchase gets you some tax deductions.)

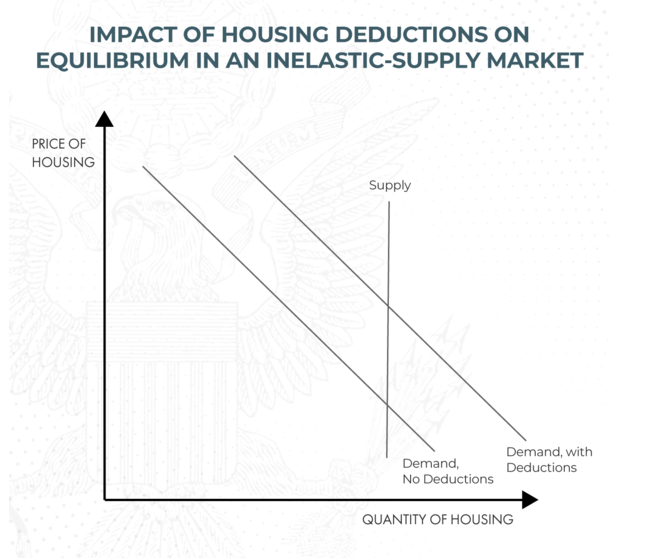

12. The higher willingness-to-pay can translate into more houses, or better houses--but *only if supply is elastic.* That is, only if builders can respond by constructing more or better houses. (left)

Otherwise, buyers just get into bidding war over existing ones. (right)

Otherwise, buyers just get into bidding war over existing ones. (right)

13. What does the real world look like? Gruber, Kleven, and Jensen (2017), more sophisticated at econometrics than I am, say that in Denmark, mortgage interest deductibility mostly increased prices and expanded housing quality, but not so much quantity.

henrikkleven.com/uploads/3/7/3/…

henrikkleven.com/uploads/3/7/3/…

14. Here in the US, our own 2017 tax bill can provide another natural test of theories about housing tax deductions and house prices.

It limited housing tax deductions at the high end of the distribution. (For example, mortgage interest deductibility beyond 750k of principal.)

It limited housing tax deductions at the high end of the distribution. (For example, mortgage interest deductibility beyond 750k of principal.)

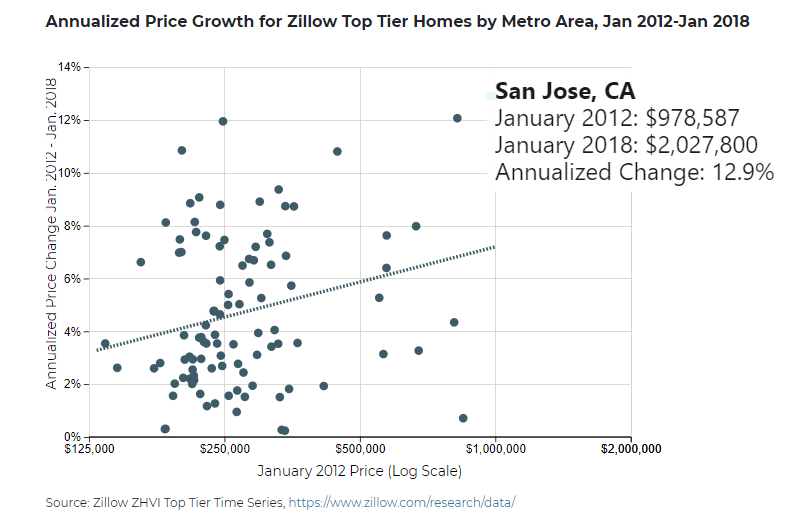

15. Here was the high end of the housing market, by metro area, prior to the tax bill being signed. This corresponds roughly to the 83rd percentile in each metro area market.

To mouse over this plot and look at interesting cities, go here: jec.senate.gov/public/index.c…

To mouse over this plot and look at interesting cities, go here: jec.senate.gov/public/index.c…

16. Pre-2018 there was a trend where high-priced markets like San Jose were pulling away from the rest of the country.

(Arguable whether this trend is truly statistically significant or not, but I'm just establishing a baseline of what the pre-TCJA world looked like.)

(Arguable whether this trend is truly statistically significant or not, but I'm just establishing a baseline of what the pre-TCJA world looked like.)

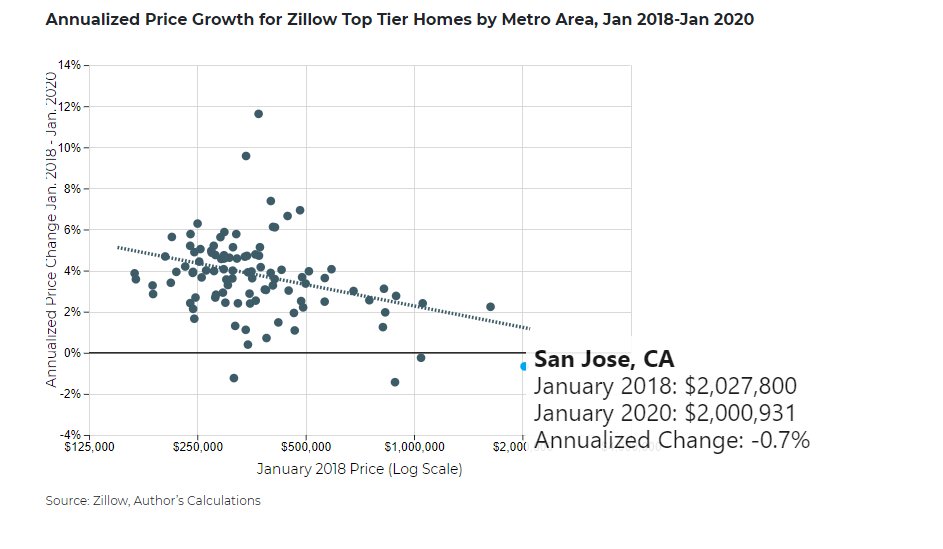

17. Here's the post-TCJA world.

After 2018, the whole trend reversed. The expensive markets really cooled down on price, and the affordable markets had their day in the sun.

Once again, find the mouseover ability on the website, here:

jec.senate.gov/public/index.c…

After 2018, the whole trend reversed. The expensive markets really cooled down on price, and the affordable markets had their day in the sun.

Once again, find the mouseover ability on the website, here:

jec.senate.gov/public/index.c…

18. Why do we care about these high-end markets and their price trends?

The argument is this: the MID for >$750,000 of principal was largely capitalized into the value of existing homes in San Jose, NYC, and so on. It "passed through" to the incumbent high-end homeowners there.

The argument is this: the MID for >$750,000 of principal was largely capitalized into the value of existing homes in San Jose, NYC, and so on. It "passed through" to the incumbent high-end homeowners there.

19. While this is good for the incumbent owners, it is quite literally the opposite of an affordability provision for those looking to break into the market.

Also: I don't usually make strong distributional arguments but if you are a homeowner in San Jose you're doing pretty OK.

Also: I don't usually make strong distributional arguments but if you are a homeowner in San Jose you're doing pretty OK.

20. At @JECRepublicans, @SenMikeLee has charged us with researching how to make it more affordable to have a family.

Housing tax deductions are often couched in the language of family affordability by proponents.

Empirically, though, they don't seem to help, and may even hurt.

Housing tax deductions are often couched in the language of family affordability by proponents.

Empirically, though, they don't seem to help, and may even hurt.

21. Therefore, I think highly of the general approach of limiting these deductions at the high end, and making life affordable for families in other ways.

There are many proposals that fit this description in one way or another, and I'm not picky between them. They're all good.

There are many proposals that fit this description in one way or another, and I'm not picky between them. They're all good.