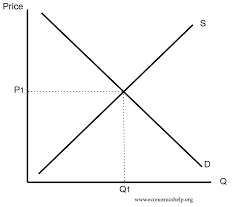

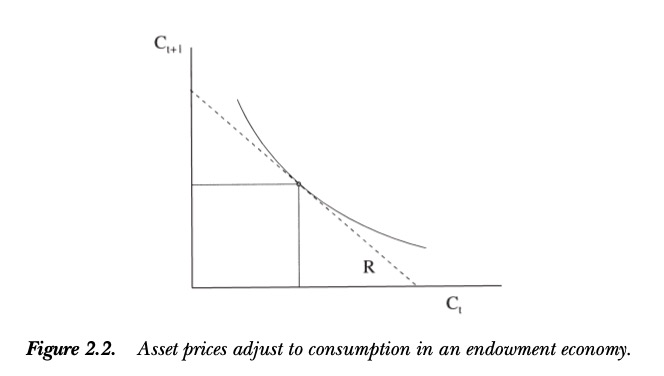

First, let’s contrast two views of market formation. On left is econ supply and demand. On right is Asset Pricing—mkt clearing price is less about quantities; more about equating intertemporal marginal rate of substitution to form a discount rate.

This consumption based paradigm ran into issues immediately. Shiller 1982 for instance finds to reconcile stable consumption + volatile prices you need high sigma S (ie, high discount rates). Prescott-Mehra, Hansen-Jagannathan develop this point further

nber.org/papers/w0838.p…

nber.org/papers/w0838.p…

You can see the core problem in Lucas 1987 (pages.stern.nyu.edu/~dbackus/Taxes…). For representative agent, consumption doesn't change much even in recession. So, at plausible discount rates, recessions shouldn't be that bad -> no reason why asset prices should be, either

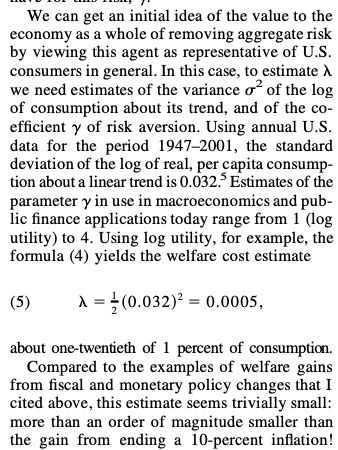

Next 20 years were ways of adding epicycles to get around the fact that stocks are volatile and consumption isn't. My personal favorite—"personal disasters" ie people lose their jobs in recessions. Starts with Mankiw, continues through Schmidt, @sc_cath

Then there is disaster risk, maybe slightly more relevant these days. Idea is you have a "peso problem"—tail risk of extreme shock that's rarely observed in macro series but is behind action. Or habit: missing even a few of my regular cappuccinos makes me unhappy (true story)

Or long run risk—even small changes to consumption forecast large changes in future cashflows, which people are averse to given preferences for early resolution of uncertainty

Or you can flip it around—why isn't consumption volatile, given asset prices are? Maybe mismeasured? So try asset pricing with garbage (@azsavov) and without garbage (so all of asset pricing?). Smoothing of consumption series may play a factor, so use proxies or unsmooth.

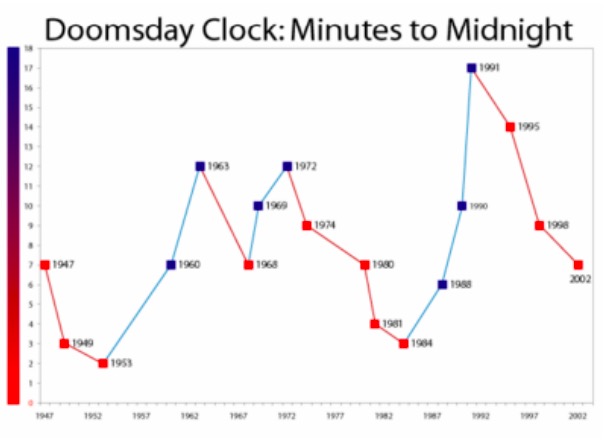

Generic problems with many of these approaches, as Campbell highlighted, is they rely on "dark matter." Hidden state variables, hard to observe, that are driving everything. Campbell fails to match disaster model, for instance, with Doomesday Clock

scholar.harvard.edu/files/campbell…

scholar.harvard.edu/files/campbell…

The other thing missing in all of these approaches is asset *quantities,* which is usually important in IO in trying to pin things down in addition to prices.

One early attempt was Hortacu and Syverson, but IO in financial markets didn't go anywhere for a while

One early attempt was Hortacu and Syverson, but IO in financial markets didn't go anywhere for a while

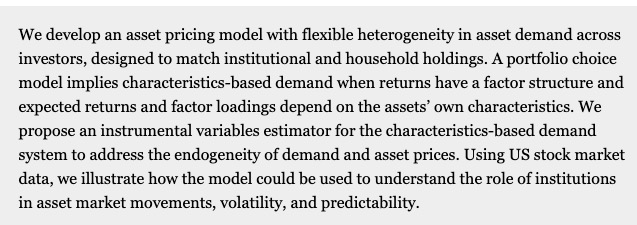

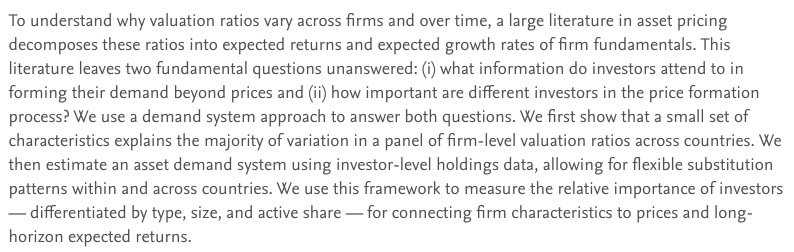

AND THEN Ralph and Moto Yogo figure out you can use 13f (and other) data to figure out asset quantities. Fits in nicely within demand estimation system, suggests intermediary asset demand "matters" for prices. Expand with @rrichmond

papers.ssrn.com/sol3/papers.cf…

papers.ssrn.com/sol3/papers.cf…

papers.ssrn.com/sol3/papers.cf…

papers.ssrn.com/sol3/papers.cf…

Okay, so finance not just a "veil" and specific intermediaries might be impacting price. How to identify?

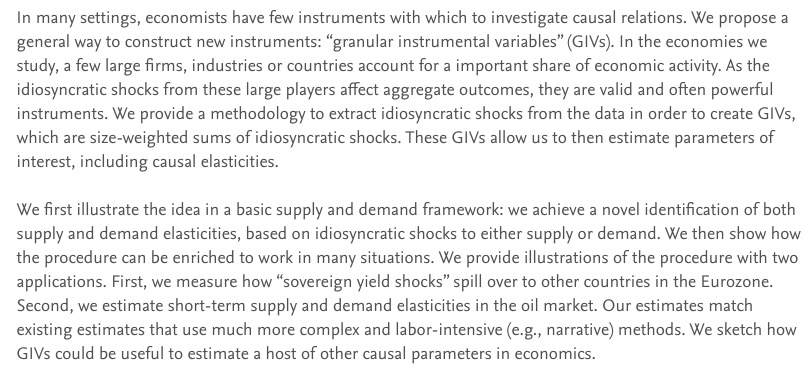

Ralph + Xavier first write this paper on "Granular IV" which uses idiosyncratic shocks from large players for identifying variation

papers.ssrn.com/sol3/papers.cf…

Ralph + Xavier first write this paper on "Granular IV" which uses idiosyncratic shocks from large players for identifying variation

papers.ssrn.com/sol3/papers.cf…

Finally getting to this paper! They:

- take idiosyncratic shocks to intermediaries as instrument for flows

- exogenous flow variation estimates "macro elasticity"—how much market moves in response to given flow

- Find it's super large: $1 (or 1%) move in flow ->5-12$/% impact

- take idiosyncratic shocks to intermediaries as instrument for flows

- exogenous flow variation estimates "macro elasticity"—how much market moves in response to given flow

- Find it's super large: $1 (or 1%) move in flow ->5-12$/% impact

Remarkably, no one has quite done this before. There is a large literature on micro rebalancing—ie substitution between stocks, that suggests fairly sizable estimates. But this "macro" elasticity is more about substitution between stocks and, say, bonds

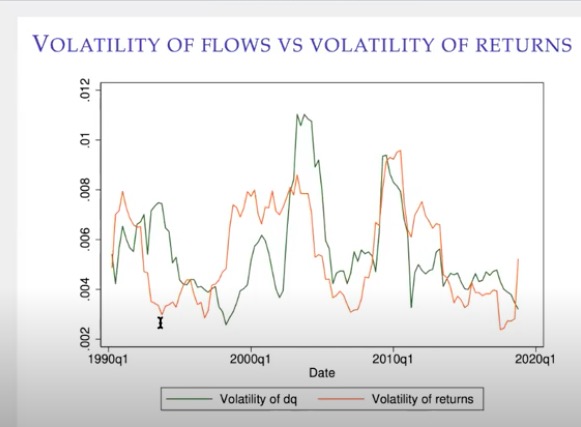

There are a few things you'd want to check out if this is true. For instance—how does flow volatility move together with asset prices? Pretty well! Suggests first order reason for asset price volatility is cyclical flows out of markets in bad times paired with inelastic demand

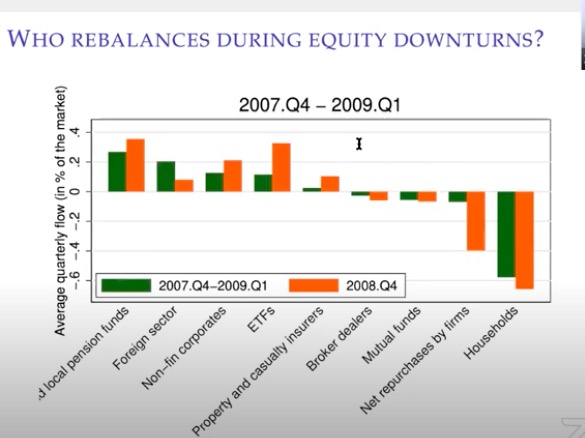

Basically in recessions, households are getting out of market (caveat: category also includes hedge funds). Limited set of arbitrageurs on other side; most mutual funds for instance are at constraint all the time -> price drops a lot before pensions, foreigners can make up slack

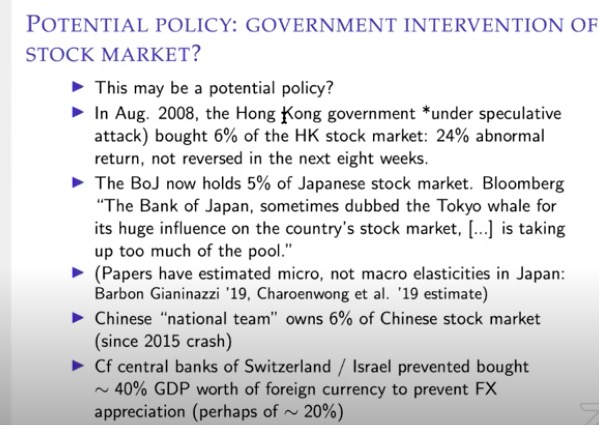

This evidence is also consistent with what happens under large-scale stock purchases, and even suggests a possible policy! Given relatively small flows tank markets, relatively small central bank purchases could keep markets stable

It's a sweeping change in how to think about markets—not efficient and elastic, but inelastic and institutional demand driven.

Another implication: addresses this "puzzle" of why US gov debt is holding value. Fed is buying a ton

papers.ssrn.com/sol3/papers.cf…

Another implication: addresses this "puzzle" of why US gov debt is holding value. Fed is buying a ton

papers.ssrn.com/sol3/papers.cf…

Might also help address other boom/bust cycles—in real estate, for instance, you may have relatively small number of speculators really moving house prices pre-2008 crisis

This doesn't kill the other asset pricing theories. But provides additional moment—flows—to match. Could imagine ie unemployment risk is the primitive causing those flows. Opens more doors for research, like this, using micro data to figure out those flows