1/ Exploiting Commodity Momentum Along the Futures Curves (De Groot, Karstanje, Zhou)

"Momentum strategies that invest in contracts on the futures curve with the largest expected roll-yield or the strongest momentum earn higher risk-adjusted returns."

papers.ssrn.com/sol3/papers.cf…

"Momentum strategies that invest in contracts on the futures curve with the largest expected roll-yield or the strongest momentum earn higher risk-adjusted returns."

papers.ssrn.com/sol3/papers.cf…

2/ Consistent with Rallis, Miffre, Fuertes (), longer-maturity contracts have higher returns, are less volatile, and are less liquid.

Contracts are fully collateralized (and, later in the paper, will be equally weighted). Returns include T-bill yields.

Contracts are fully collateralized (and, later in the paper, will be equally weighted). Returns include T-bill yields.

3/ Roll yields are calculated between the contract to be traded and the adjacent contract with one month less time.

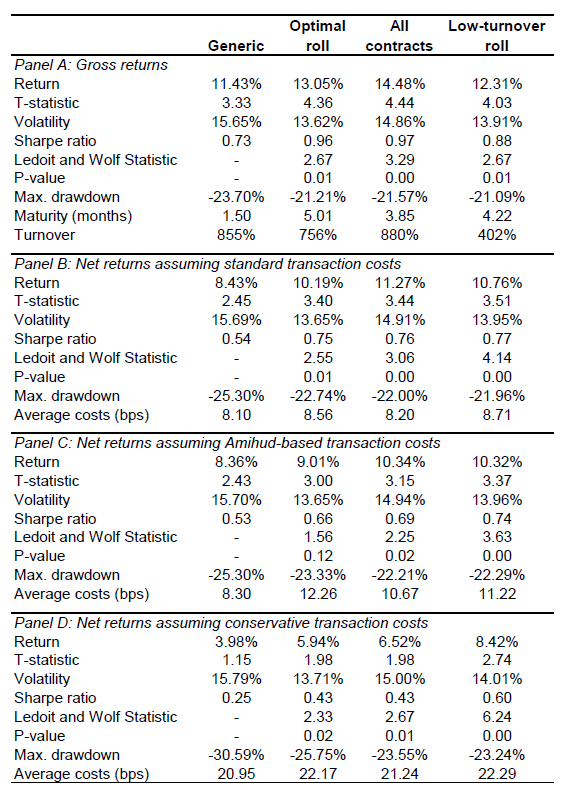

100% turnover = L/S portfolio completely changed once a year

Assumed trading costs >> than the 3.3 bps assumed in other studies.

All three strategies add value.

100% turnover = L/S portfolio completely changed once a year

Assumed trading costs >> than the 3.3 bps assumed in other studies.

All three strategies add value.

4/ Rolling Sharpes are consistently higher for alternative momentum strategies than for the generic strategy that only trades front contracts.

Outperformance survives Amihud-based costs (which assume that 12-month contracts are three times more expensive to trade); see Table 2.

Outperformance survives Amihud-based costs (which assume that 12-month contracts are three times more expensive to trade); see Table 2.

5/ Generic momentum loads on carry (untabulated correlation = +0.56).

Being able to choose contracts on the term structure is diversifying after controlling for momentum and carry.

The optimal-roll and all-contracts strategies are different (untabulated correlation = +0.35).

Being able to choose contracts on the term structure is diversifying after controlling for momentum and carry.

The optimal-roll and all-contracts strategies are different (untabulated correlation = +0.35).

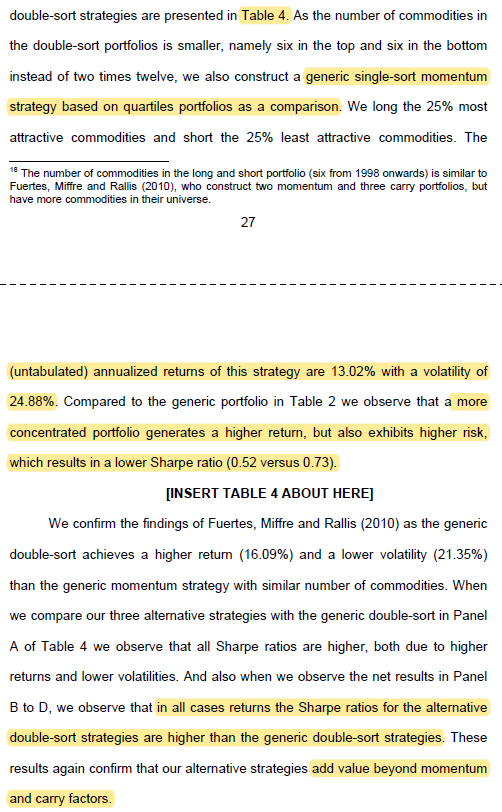

6/ "In all cases, the Sharpe ratios for the alternative double-short strategies are higher than for the generic double-sort strategies. These results again confirm that our alternative strategies add value beyond momentum and carry factors."

7/ When the choice of maturities is limited to contracts ≤6 months out, volatilities increase slightly, leading to slightly lower Sharpe ratios.

For the most part, "the additional profits are not driven by investing in futures contracts at the back end of the curve."

For the most part, "the additional profits are not driven by investing in futures contracts at the back end of the curve."

8/ Choosing only liquid contracts such that a $100 million L/S portfolio trades no more than 25% of a particular contract's volume, which excludes half of the contracts (Table 6) or such that a trade of $1 million has ≤4 bps impact (Table 7) has little impact on Sharpe ratios.

9/ Including a one-day implementation lag has only a small impact.

Examining performance from 2000-2011 leads to higher gross returns and higher volatility (from higher market volatility). This actually helps post-cost Sharpe ratios because of lower transaction costs post-2000.

Examining performance from 2000-2011 leads to higher gross returns and higher volatility (from higher market volatility). This actually helps post-cost Sharpe ratios because of lower transaction costs post-2000.