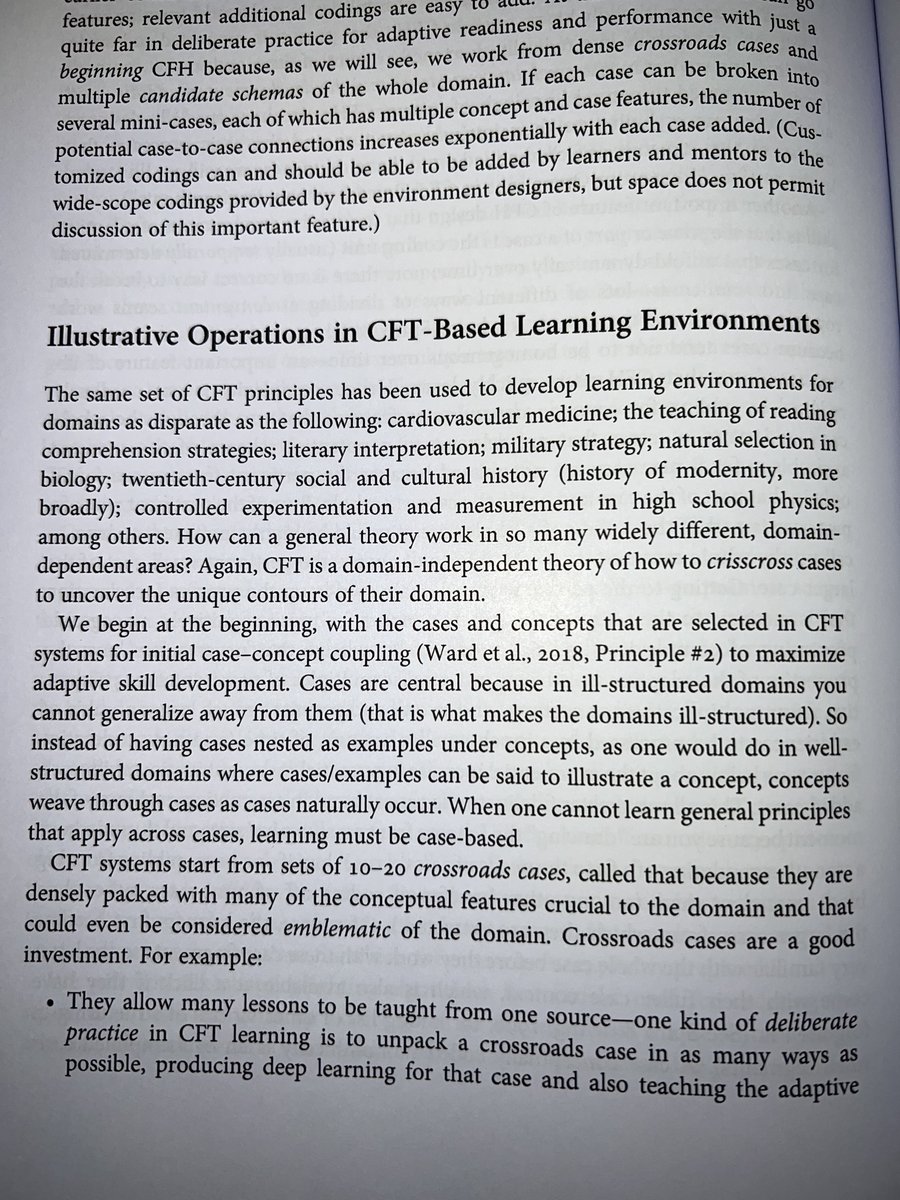

Half the people in this thread understand the capital allocator playbook.

The other half do not.

And Andrew is laughing all the way to the bank.

The other half do not.

And Andrew is laughing all the way to the bank.

https://twitter.com/awilkinson/status/1268212340173836288

The capital allocator playbook is simple to grok. Build a free cash flow generating business. Wait. Take the FCF and then use it to purchase another FCF-generating business. Wait. Use those cash flows to buy yet another FCF generating business. Wait.

Rinse and repeat.

Rinse and repeat.

There are many variations of this, of course. The model I described above is pretty much the one @awilkinson uses; it's also the Berkshire model.

Many more variations in amazon.com/Outsiders-Unco…

Many more variations in amazon.com/Outsiders-Unco…

In software, the two companies that are most famous for using this playbook are Robert Smith's Vista Equity Partners (uses a lot of debt) and Mark Leonard's Constellation Software (uses equity sales).

Still, similar playbook: acquire defensible high FCF businesses. Use FCF.

Still, similar playbook: acquire defensible high FCF businesses. Use FCF.

Smith is operationally excellent, though. He has a team in Vista that slashes costs and moves engineering to cheaper cities. He then uses the FCF from the business to service the debt load. It's a more typical PE playbook. Only diff is that it's software — so high, high margins.

Leonard's trick is looking for 'vertical market' software companies. Think: power plant software. Who's going to throw out and switch their power plant software provider? Nobody. So it's got a moat.

Same playbook, with variations: Constellation sold equity to fund purchases.

Same playbook, with variations: Constellation sold equity to fund purchases.

More info on Leonard: 25iq.com/2018/04/07/bus…

And Smith: 25iq.com/2018/03/23/bus…

Both from the inimitable @trengriffin.

And Smith: 25iq.com/2018/03/23/bus…

Both from the inimitable @trengriffin.

Another solid book on this topic is @farnamjake1's The Rebel Allocator. It's written as a novel, so it's easy to read. Worth the 10 bucks!

People in startups don't usually see this side of the business world, I think.

But the playbook is public if you know where to look.

People in startups don't usually see this side of the business world, I think.

But the playbook is public if you know where to look.

Whoops, totally forgot to link to it: amazon.com/Rebel-Allocato…

One possible reason people in startupland don't get the capital allocator playbook is that it's not really an operator-oriented worldview.

Nearly everyone I've mentioned in the thread above sets up their org so that other people run their companies. They themselves do not.

Nearly everyone I've mentioned in the thread above sets up their org so that other people run their companies. They themselves do not.

So: Smith has an ops arm, Leonard, Wilkinson, Buffett and, urm, every CEO mentioned in The Outsiders delegated the operator function to someone else. They just ran capital allocation decisions.

Two more, just for fun:

Jeff Bezos runs Amazon with bits borrowed from the capital allocator playbook. (Why does he insist on absolute free cash flow?)

Barry Diller runs IAC similarly, but divests successful, FCF-producing subsidiaries after they hit a certain scale.

Jeff Bezos runs Amazon with bits borrowed from the capital allocator playbook. (Why does he insist on absolute free cash flow?)

Barry Diller runs IAC similarly, but divests successful, FCF-producing subsidiaries after they hit a certain scale.

Sorry, *absolute dollar free cash flow, to be exact. 25iq.com/2014/04/26/a-d… (Google "Tren Griffin + Bezos + absolute dollar free cash flow" and you'll get a number of hits)

• • •

Missing some Tweet in this thread? You can try to

force a refresh