1. New #FDD out this week on estimating 2020 corn trend yield for the US. It would seem simple to agree on the "right" trend but it is not. farmdocdaily.illinois.edu/2020/06/how-se…

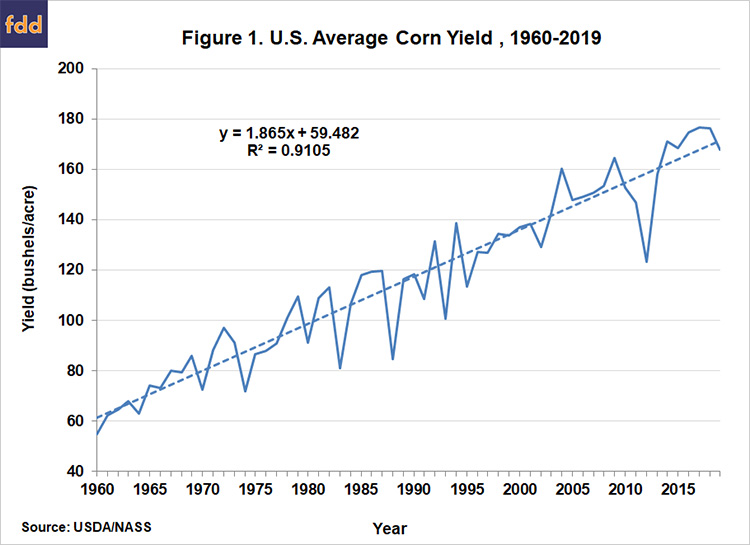

2. History of US average corn yield since 1960. We ask what year should be the first in the sample used to estimate a trend line? Only discussed in bits and pieces as far as I could find. We take a systematic look.

3. We first estimated trend line for 1960-2019 and used that line to project a trend yield for 2020. Just project the line in the chart out one more year. This gives an "unconditional" trend estimate of 173.2 bpa.

4. We then drop 1960 from the sample and do the same thing. Sample is 1961-2019. Projected 2020 trend yield is 173 bpa. We keep moving the starting year forward one year at time until 2000. Last sample is 2000-2019.

5. This chart shows the projected 2020 trend yield for US corn by starting year of the sample estimation period. All samples end in 2019. The pattern is very interesting (at least it was to me).

6. Lowest 2020 trend yield for corn uses samples starting in the 1960s and the highest use samples starting in the 1980s. The 80s result makes sense. Drought years in 80, 83, 88 pull down the starting yields for those samples and make the lines slope more steeply.

7. Notice also that latest samples (90s) do not show the highest trend yields. That is curious given all the talk about an increased rate of growth in trend yields due to genetic improvements. Maybe just not enough data yet. Still.....

8. Finally, note that USDA used a projected trend yield of 178.5 bpa for 2020. Can get close only if you start your sample in 1988. Maybe only a coincidence but that is the year sample starts for WAOB crop weather model that is the base for USDA trend projection.

• • •

Missing some Tweet in this thread? You can try to

force a refresh