A Thread-

Chemical Sector - Catalytic Substitution in Play by @swarnabh_m

The Indian Chemical Industry is presently positioned in front of a set of developments that would result in strong growth opportunities in both the overseas and the domestic markets for Indian players.

Chemical Sector - Catalytic Substitution in Play by @swarnabh_m

The Indian Chemical Industry is presently positioned in front of a set of developments that would result in strong growth opportunities in both the overseas and the domestic markets for Indian players.

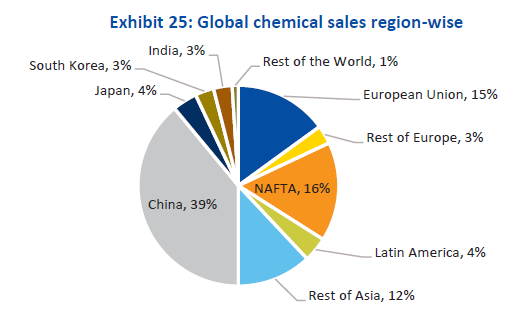

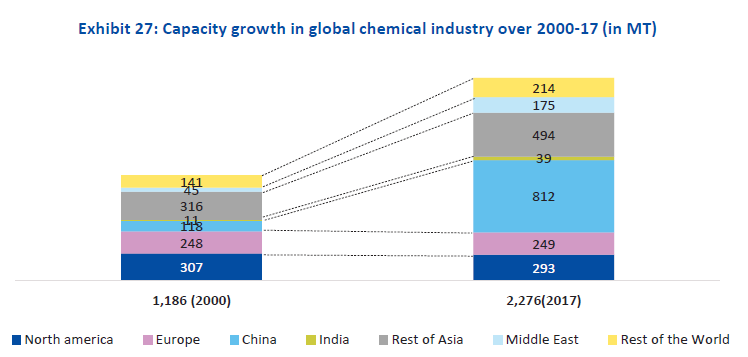

While China is a behemoth in global chemical manufacturing, constituting ~39% of market share, supply chain disruptions which happened over the last few years increasingly prompt global players to de-risk their sourcing strategy to other countries.

India’s low manufacturing cost structure could aid in grabbing a share of this pie, particularly in the specialty chemicals side which already forms a significant share of our exports. Players in specialty chemicals, and those in the contract research/manuf could benefit.

Improving downstream demand opens up room for import substitution - Domestic manufacturers have also shown intent of sourcing raw materials locally and government impetus for chemical and pharmaceutical manufacturing could open opportunities for import substitution

What to play - companies exposed to pharmaceutical and agrochemical industries, which appear to be bright spots, could provide good investment opportunities. Strong technical and technological expertise and track record in the export markets would bode well for long-term growth

Given the strength in business model and earnings visibility of a few, valuation levels may fairly represent the growth and the play will be mostly on their earnings momentum.

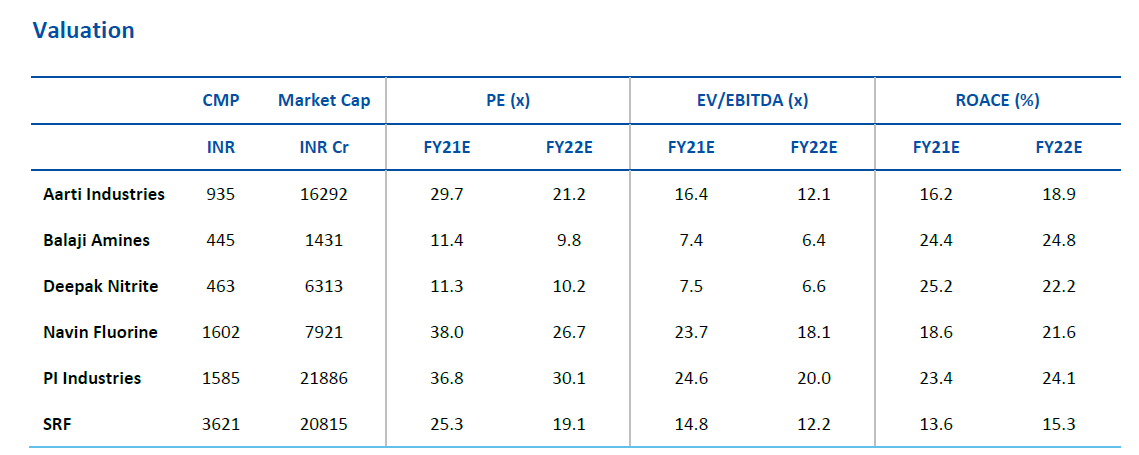

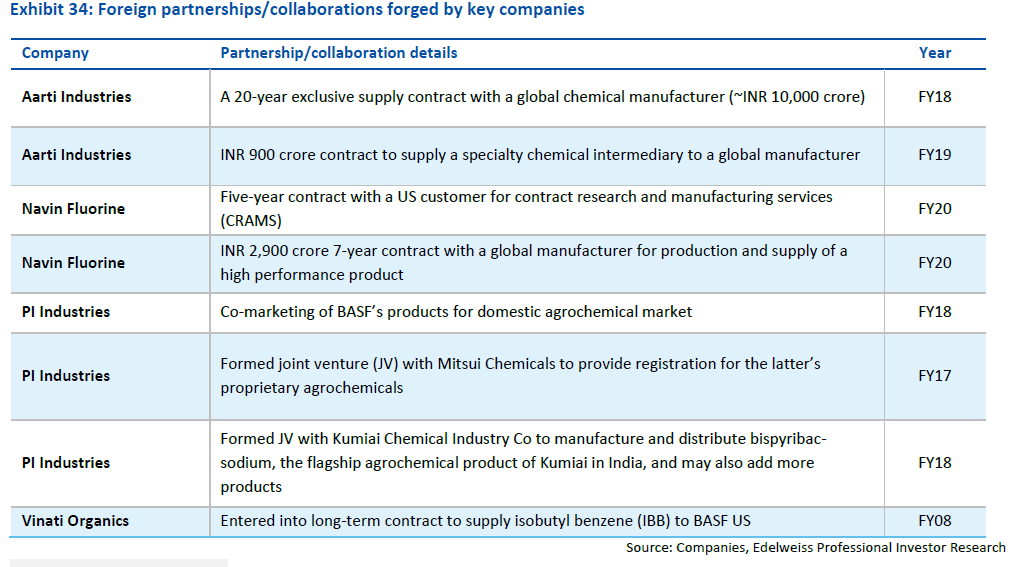

Focus companies - SRF, PI Industries, Navin Fluorine, Aarti Industries, Balaji Amines, Deepak Nitrite.

Focus companies - SRF, PI Industries, Navin Fluorine, Aarti Industries, Balaji Amines, Deepak Nitrite.

Valuations

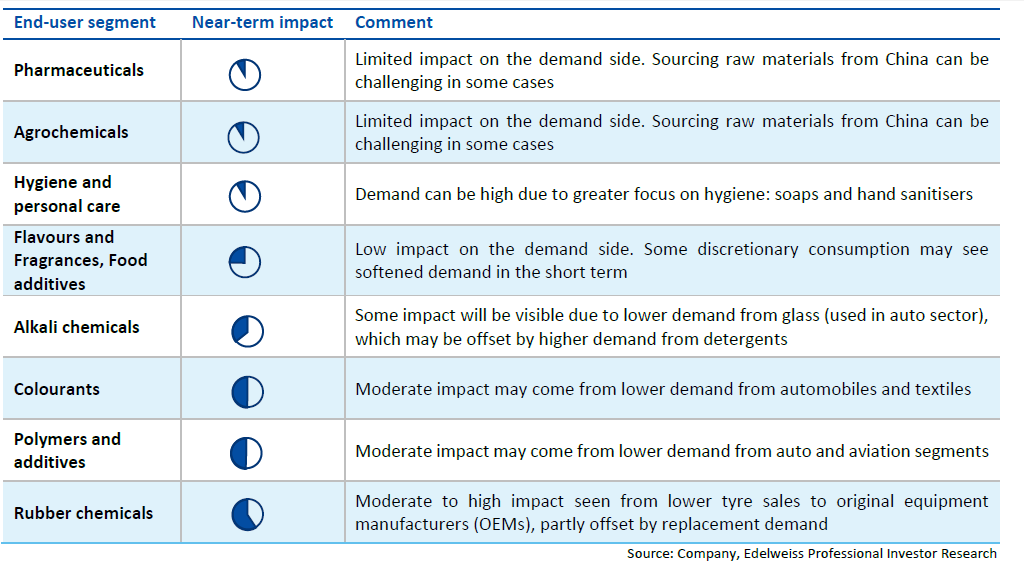

Pharma and agrochemical sectors will see limited impact on demand due to COVID induced lockdown

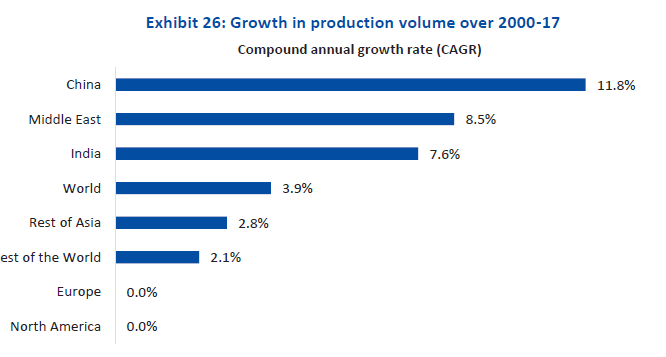

Tailwind over the longer term emerges for India, more so in specialty chemicals - Due to supply-side disruptions emerging out of China (environmental protection, dislocations in the supply chain due to COVID-19), global manufacturers to diversify a part of their sourcing

China commands ~39% share in the global chemical market; tough to replicate capacities in bulk chemicals; but a small shift from China to India could also be a major boosts as China's global market share is >10X of India.

A lower cost base, availability of technically skilled manpower and stronger intellectual property laws position Indian companies as capable partners for global players.

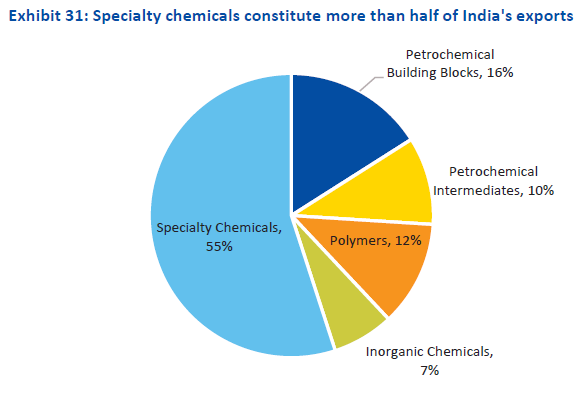

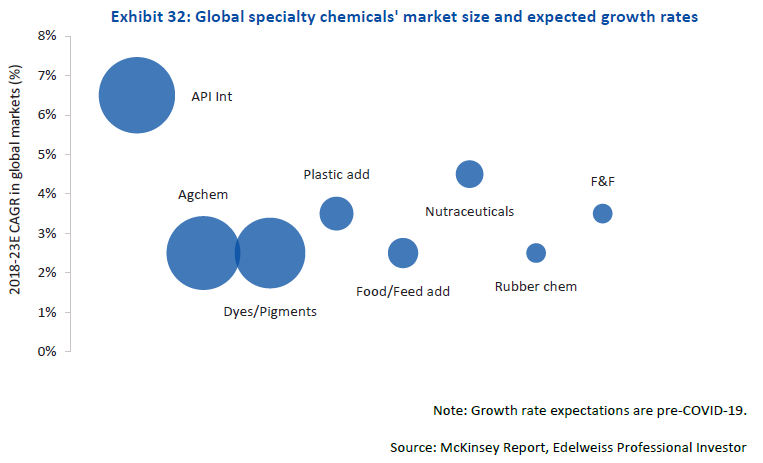

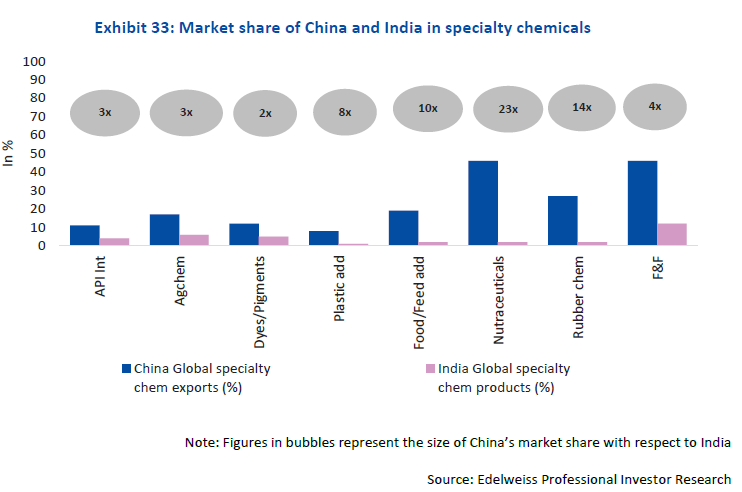

Speciality Chemical could be India's dark horse. Specialty chemicals form the largest share of exports for Indian chemical manufacturers (>50%), but accounts for <3% of global export value less than 25% of China's share.

The situation is not as low as in the case of bulk chemicals, implying a better market penetration for Indian players. Agrochemicals, dyes and pigments, and intermediates for active pharmaceutical ingredients (API) are key segments in terms of specialty chemicals being exported.

Import substitution - Indian manufacturers import a large share of their raw materials and API intermediates from China. Significant government impetus is visible in this area, outlined by the recent bulk drug policies that

emphasizes on development of integrated bulk drug parks

emphasizes on development of integrated bulk drug parks

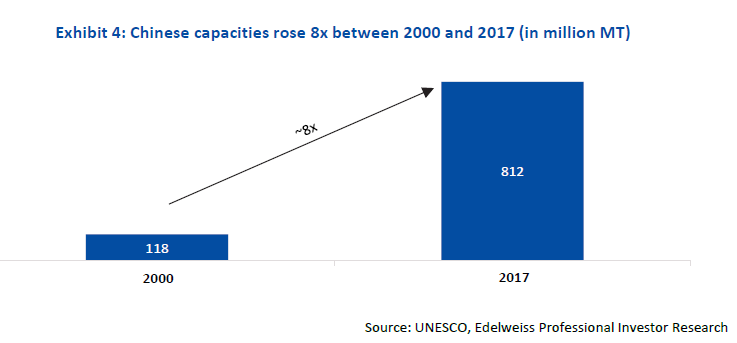

The ‘China’ tailwind – India gains from disruptions. Chinese capacities are so large that other (including India) can gain from any supply disruptions, and there have been many lately

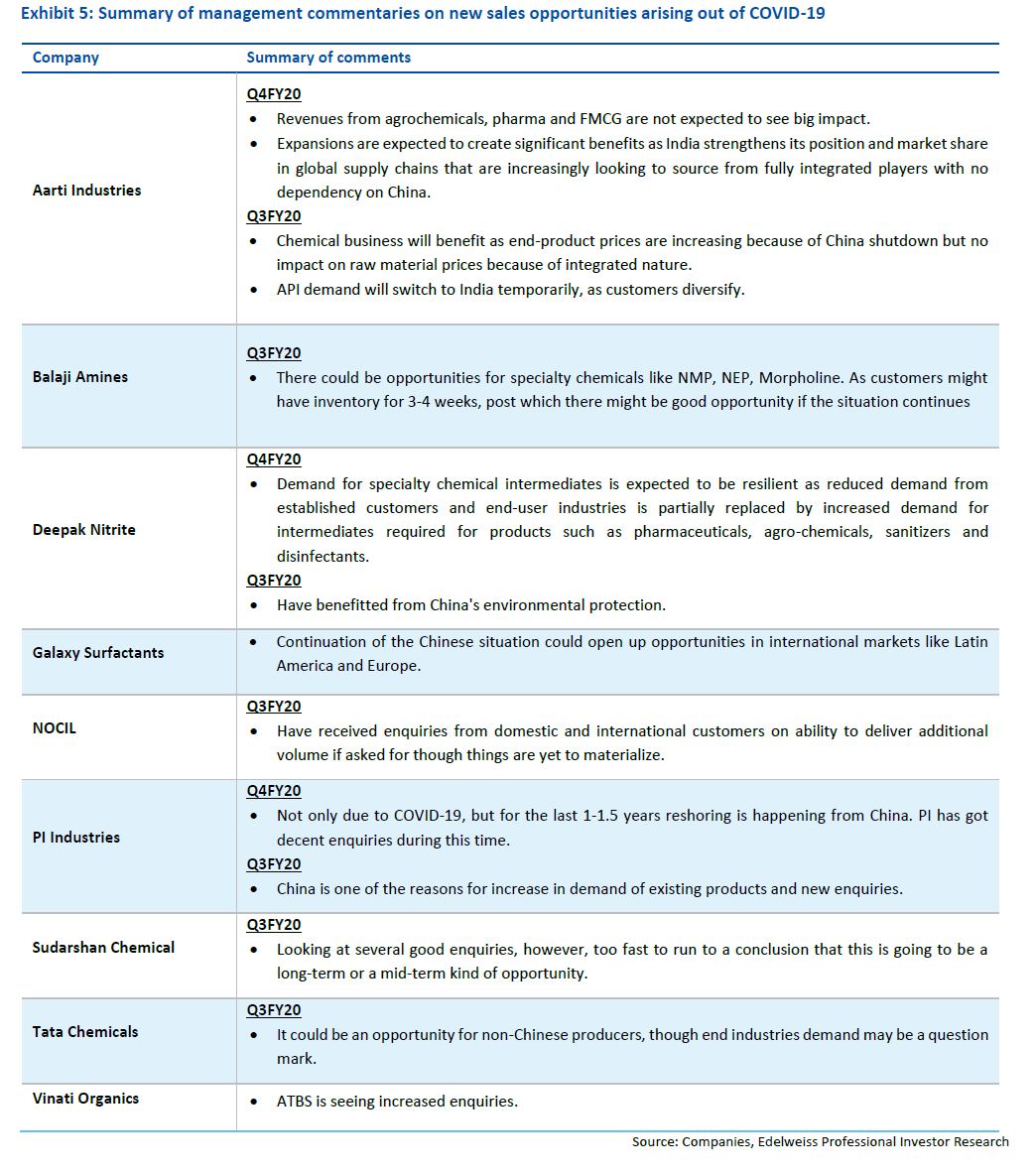

COVID led supply disruptions in China had a short term drag across the globe due to Chinese integration across global supply chain. Indian companies also suffered. Things have recently begun to imporve. Here is what companies are saying.

Companies have made headways in diversifying raw material sourcing from China. Several players have focused on sourcing raw materials from other geographies or have alternative arrangements in place in case of disruptions.

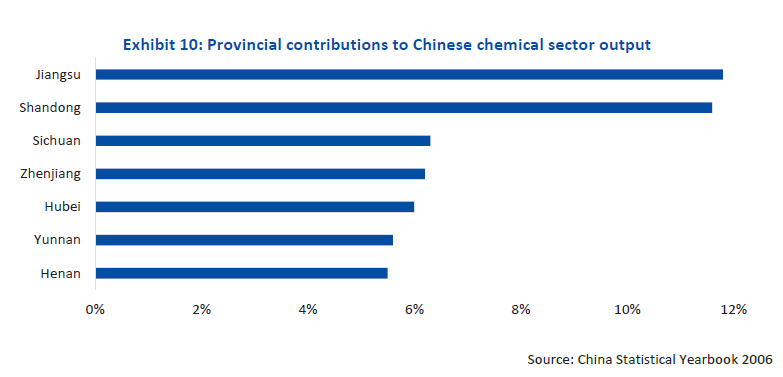

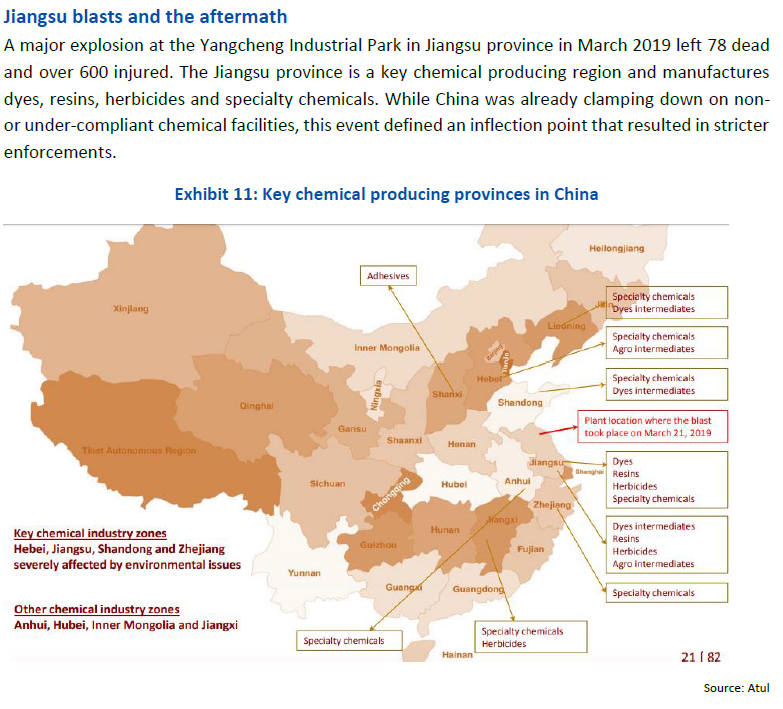

Environmental controls increased in China. Regulations been strict, the enforcement has been strong. Closure of chemical plants, relocation of industry were the goals. To have ~90% of plants within chemical parks by 2025 vs under 50% in 2018.

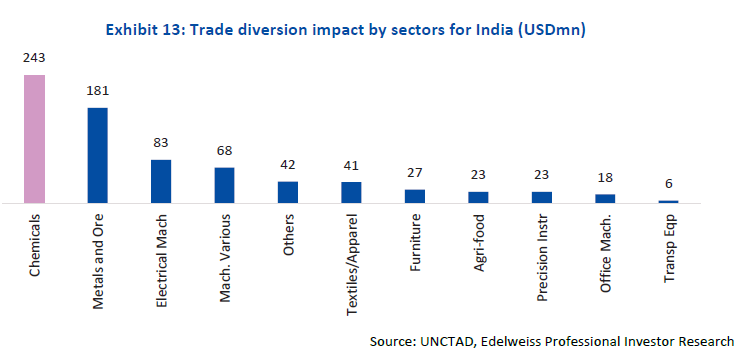

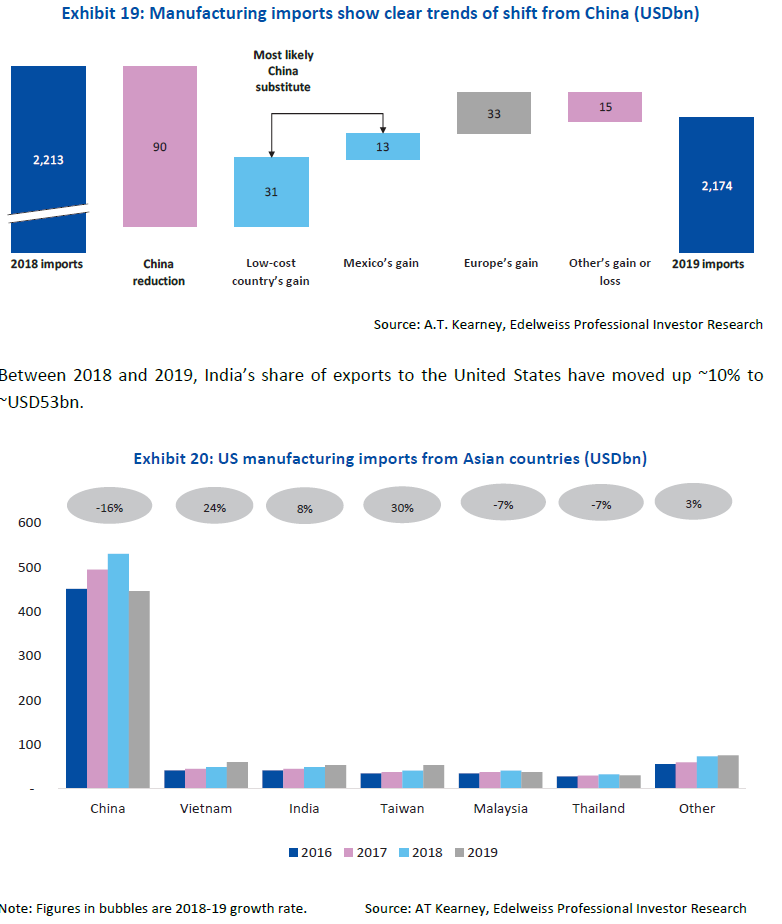

US China trade war - led to supply disruptions and shifting out of China. As per UNCTAD, Taiwan was the biggest beneficiary, accounting for $4.2bn of additional exports to US in H1CY19. Mexico, EU, Vietnam, Japan, Korea and Canada were other countries ahead of India

But in chemical sector, India was a clear beneficiary. Of the $755mn additional exports by India to the US in H1CY19, the sector saw the highest contribution of $243mn. This was 2nd only to Japan ($342mn). It constituted 11% of the total benefits from diversion of trade in H1CY19

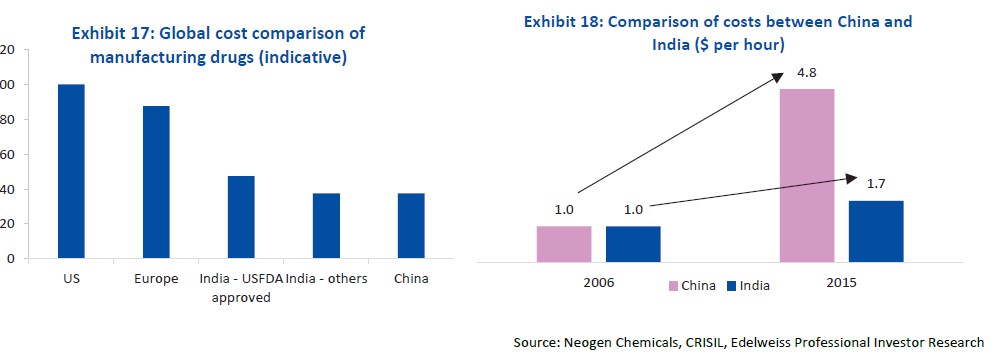

India scores well on the labour cost front - Cost of manufacturing in India is among the lowest globally. While costs are low for China as well, they are expected to increase due to high overheads for adhering to stricter environmental rules.

The cost of production of APIs in China continues to remain 20-30% lower than India, aided by lower cost of raw materials and utilities. India fares well in terms of labour cost, which is almost half of Chinese manufacturers. Labour costs in China has continuously increased.

Analysis from AT Kearney shows that of the USD90bn fall in Chinese imports (across products in the US, around a third (USD30bn) has moved to low-cost Asian countries.

Indian chemical industry is small- India contributes ~3% of global chemical sales despite being the sixth

largest chemical industry globally. India is the 3rd largest consumer of polymers, 4th largest producer of agrochemicals and 6th largest producer of chemicals in the world

largest chemical industry globally. India is the 3rd largest consumer of polymers, 4th largest producer of agrochemicals and 6th largest producer of chemicals in the world

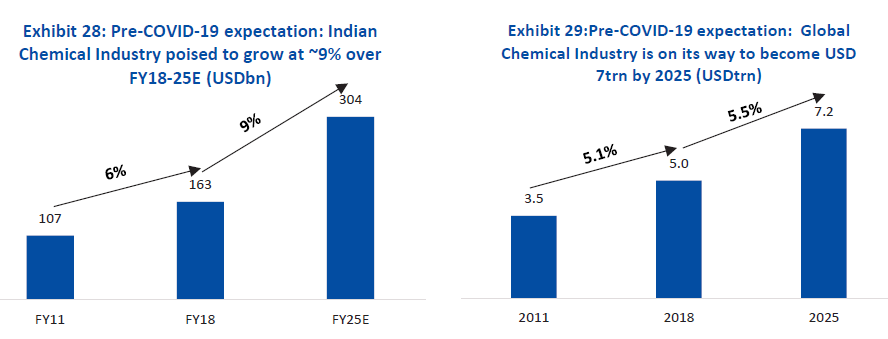

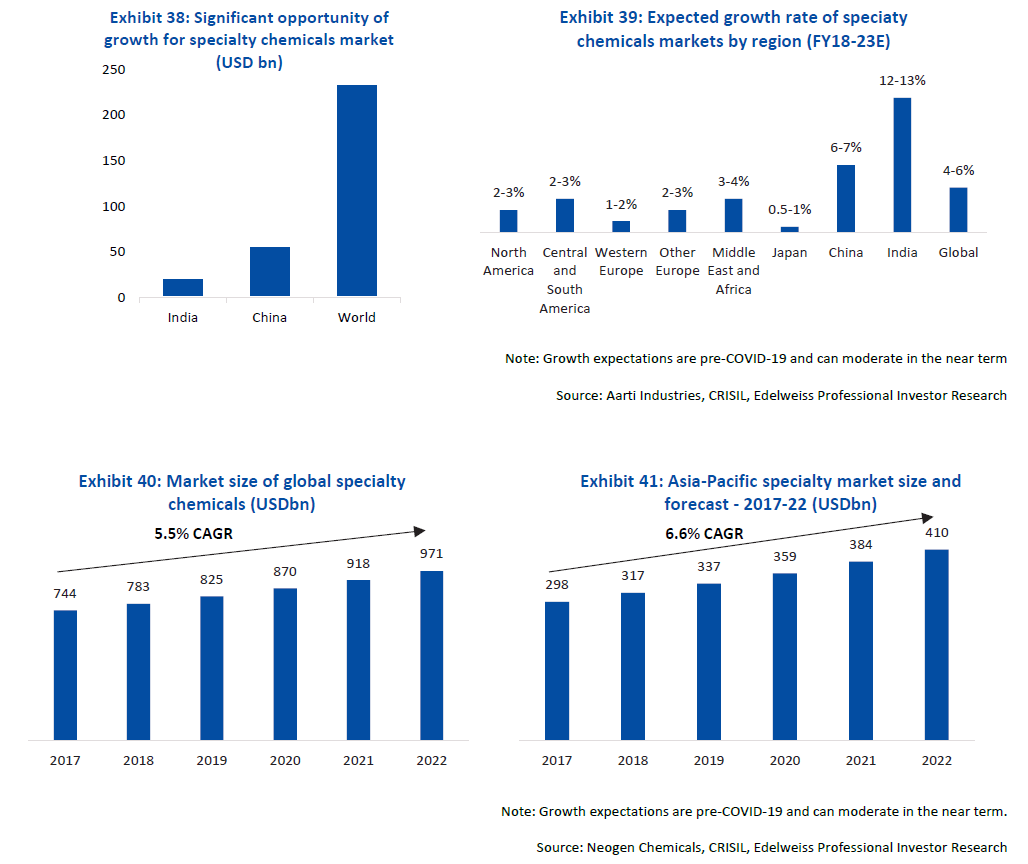

Indian chemical sector- Contributing ~15% to Indian manufacturing sector and ~2% of GDP. The sector had a total market size of $163bn in FY18, is expected to grow ~9% to $300bn by FY25. Of this, specialty chemicals industry is expected to contribute ~5% of global sales by FY21

India is well positioned to harness growth in global specialty chemical. India’s share in the specialty chemical global market is in low single-digits. This

is about a quarter of China’s capacity. Intermediates for APIs, agrochemicals and colourants are the key export segments

is about a quarter of China’s capacity. Intermediates for APIs, agrochemicals and colourants are the key export segments

Chemical companies with existing global relationships to benefit. Global manufacturers would try to de-risk their supply chain by moving a part of their supply

chain to countries other than China. India could be a key beneficiary of this trend.

chain to countries other than China. India could be a key beneficiary of this trend.

This would in effect be a structural shift, a portion of which would come to Indian companies, and would aid those who have: a) Developed scale; b) Proven technical expertise; c) Existing customer relationships; and d) Demonstrated track record of delivery.

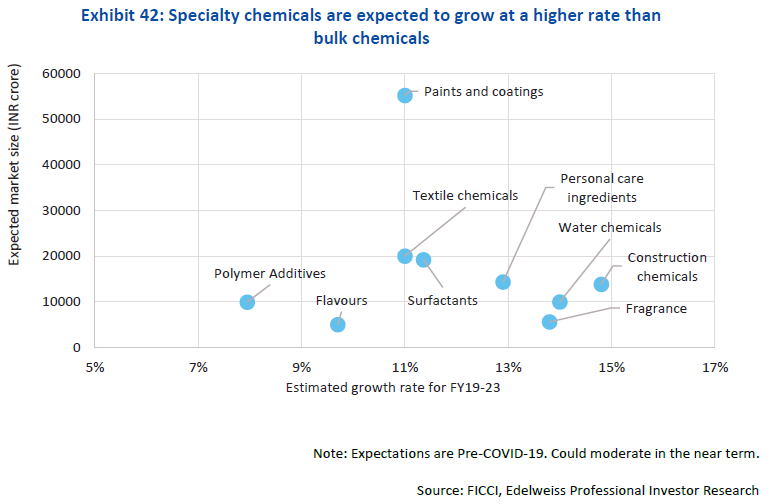

Specialty chemicals to grow faster than bulk chemicals in domestic markets - As end-user industries in India undergo changes in terms of value addition in product categories, demand for specialty chemicals is expected to grow at a faster rate

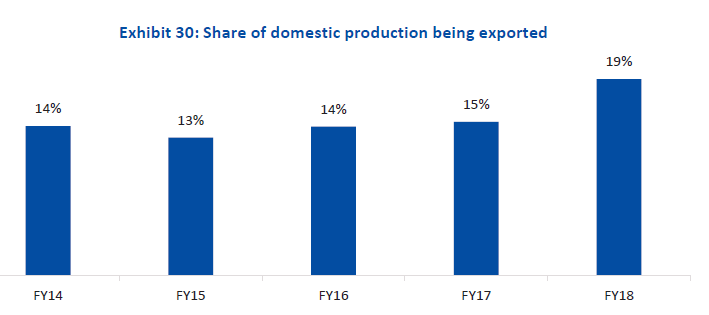

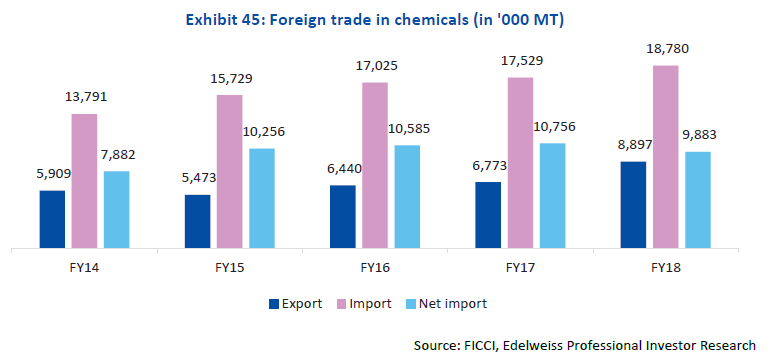

Domestic production of bulk chemicals is not sufficient to meet internal demand - In order to meet this shortfall, India imports a large volume of chemicals, as compared to exports. With imports pegged at 18,780 thousand MT in FY18, India remains a net importer of chemicals.

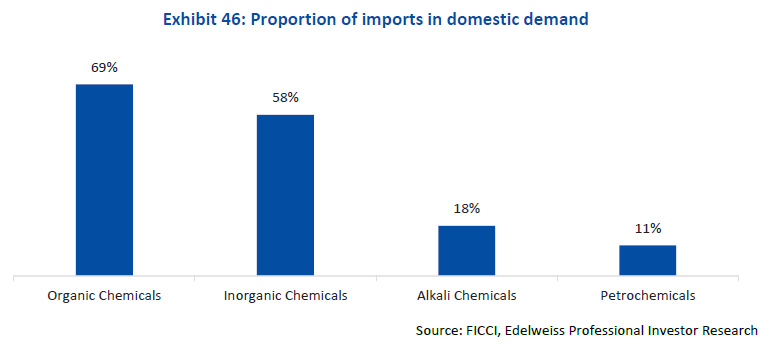

India’s largest share of imports are in organic and inorganic chemicals, which are close to 70% and 60%

respectively. For alkali and petrochemicals, the import share is at around 18% and 11% respectively

respectively. For alkali and petrochemicals, the import share is at around 18% and 11% respectively

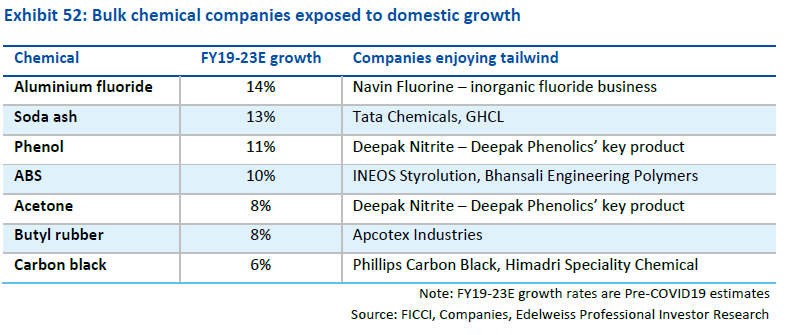

Future growth rate to be higher than past - Recent impetus on domestic production is expected to fuel the growth rate in the chemical industry going forward. A study by FICCI estimates (pre-COVID-19) FY19-23 growth rates of ~13/9/9/8% for alkali/ inorganic/organic/ petrochemicals

Government initiatives to be pivotal for growth. Under Govt Make in India Petroleum, Chemicals and Petrochemicals Investment Regions (PCPIR) to provide integrated chemical manufacturing hubs with feedstock anchors have been set up. National policy on Petchem, 100% FDI will be key

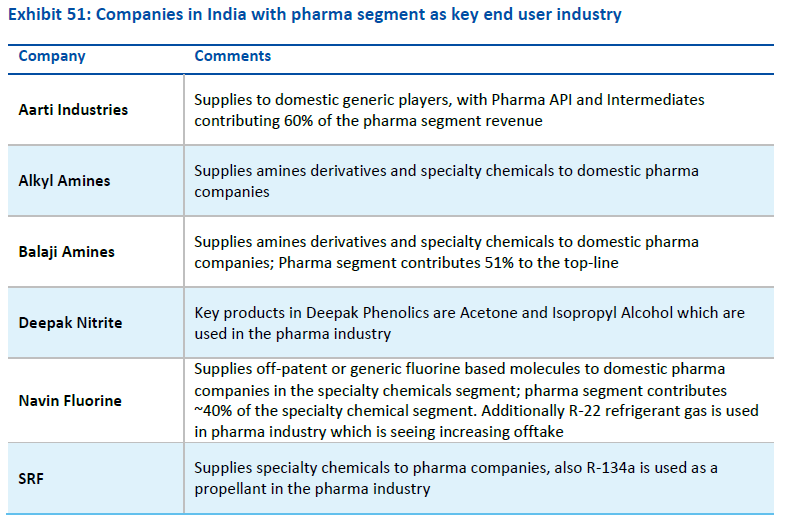

New Bulk Drug Promotion Policy could aid chemical players in the pharma chain - government impetus on domestic API manufacturing, EODB and faster clearances for capex would be pivotal for growth of the sector. Mega bulk drug parks could be a booster.

India currently imports 70% of APIs from China, which has

resulted in challenges during the supply chain disruption. We believe that bulk drug manufacturers may source critical raw materials for their products from domestic suppliers.

resulted in challenges during the supply chain disruption. We believe that bulk drug manufacturers may source critical raw materials for their products from domestic suppliers.

Import substitute products are also seeing increased capacity expansions in India - expect demand traction from domestic players as capacities of

more import substitutions are added.

more import substitutions are added.

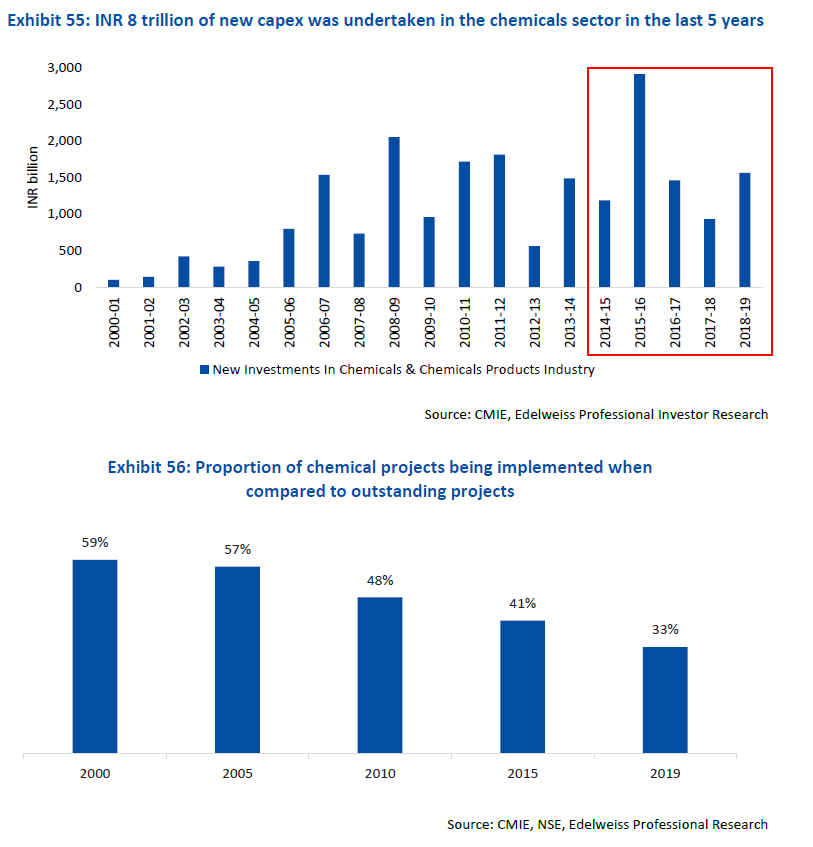

Capex is being undertaken to capitalise on this shift - Capital expenditures have increased as companies started getting overseas mandates for manufacturing and identified domestic import substitution and export opportunities.

Playing the themes in the chemical sector - urge investors to look at the stocks in this sector with a longer-term investment horizon. Many companies are reasonably

valued in the market, due to the quality of their business model and earnings visibility.

valued in the market, due to the quality of their business model and earnings visibility.

We recommend 2 approaches

1. invest in players who have already proven their mettle or are in the process. SRF, NAVIN, PI, Aarti

2. players who are rampingup substantial capex or are currently undertaking large capex to respond to the domestic demand. Balaji, Deepak Nitrite

ends

1. invest in players who have already proven their mettle or are in the process. SRF, NAVIN, PI, Aarti

2. players who are rampingup substantial capex or are currently undertaking large capex to respond to the domestic demand. Balaji, Deepak Nitrite

ends