1/ A few random thoughts on the idea of a "stock picker's market"...

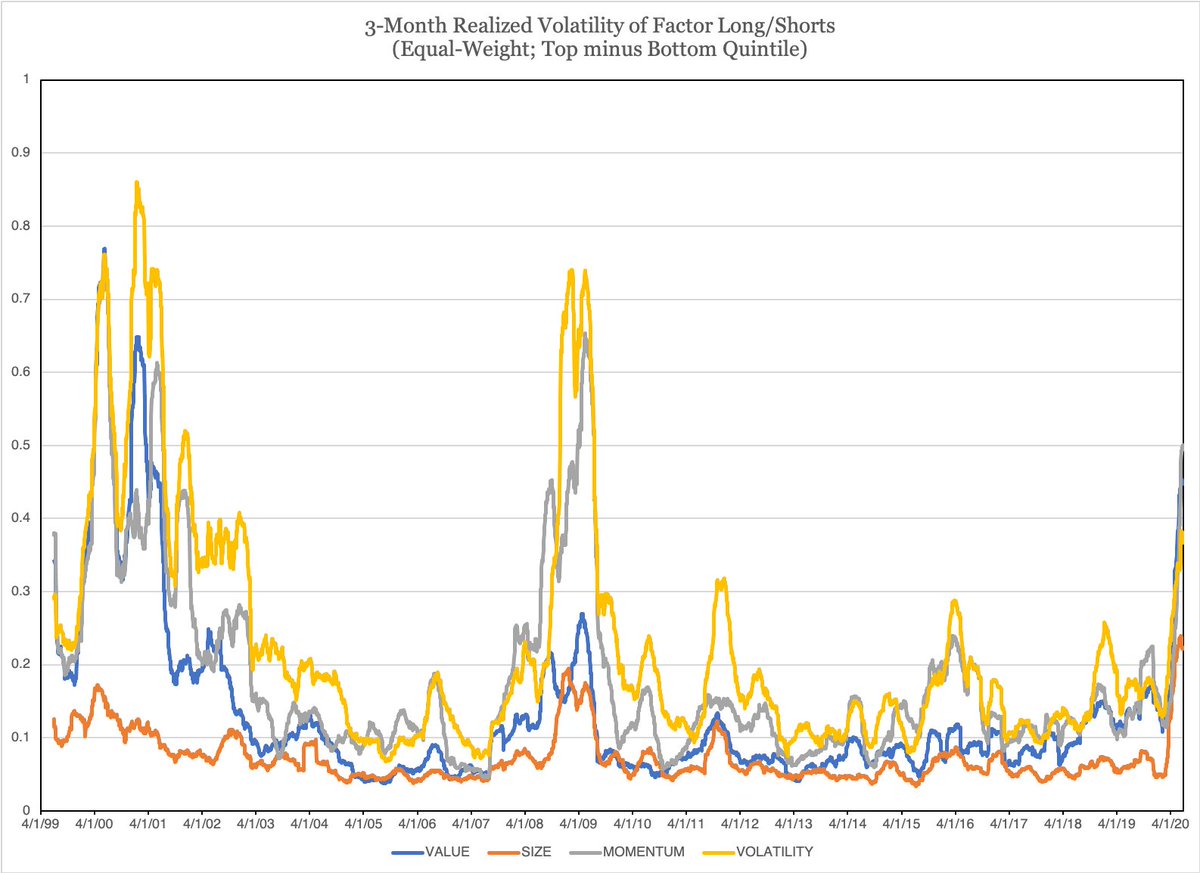

Below I plot two long/short value strategies. Both use a composite set of measures, rebalance monthly, and buy the top quintile / short the bottom quintile.

But one peaks in 2013 and the other 2017.

Below I plot two long/short value strategies. Both use a composite set of measures, rebalance monthly, and buy the top quintile / short the bottom quintile.

But one peaks in 2013 and the other 2017.

2/ The only difference? One is market-cap weighted and one is equal-weighted.

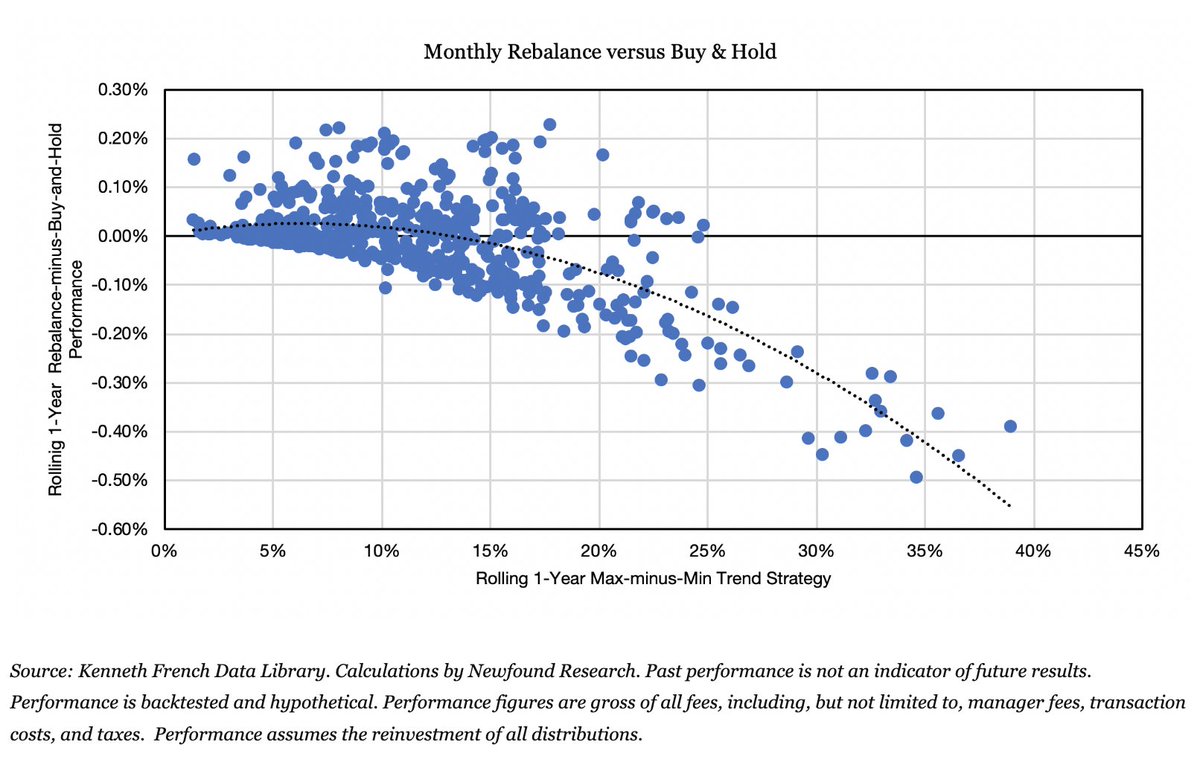

Now consider this graph that shows a long/short portfolio that is equal-weight the top 10 stocks by market cap and short the bottom 990 (R1K proxy universe).

Now consider this graph that shows a long/short portfolio that is equal-weight the top 10 stocks by market cap and short the bottom 990 (R1K proxy universe).

3/ Not surprisingly, many of these "top 10" stocks find themselves in the bottom decile of value.

And when we market-cap weight our legs, we end up with significant short exposure to them.

Equal-weight still shorts them, but doesn't do so in an out-sized manner.

And when we market-cap weight our legs, we end up with significant short exposure to them.

Equal-weight still shorts them, but doesn't do so in an out-sized manner.

4/ Why does this matter for long-only stock pickers?

Recall that a long-only portfolio can be decomposed into two pieces:

Benchmark + Active Share x Active Bets

where Active Bets is a dollar-neutral long/short portfolio capturing over- and under-weights.

Recall that a long-only portfolio can be decomposed into two pieces:

Benchmark + Active Share x Active Bets

where Active Bets is a dollar-neutral long/short portfolio capturing over- and under-weights.

5/ A big difference between the implicit long/short embedded in a long-only portfolio and an explicit long/short portfolio is that in the former you can only go as short as market-cap allows you.

e.g. You can implicitly short a lot more AAPL than UA.

e.g. You can implicitly short a lot more AAPL than UA.

6/ What happens when the top 10 stocks keep growing?

Today, a neutral view on this top 10 would require us to put 30% of our portfolio into them, reducing our potential active share!

Today, a neutral view on this top 10 would require us to put 30% of our portfolio into them, reducing our potential active share!

7/ And if we do that, then we need to reduce our explicit fee. Otherwise, at least 30% of our portfolio is basically just beta, which costs 0.

eg If we charge 1% and go from 100% active share to 70% active share, our hurdle rate goes from 1% to 1.42%!

blog.thinknewfound.com/2017/11/longsh…

eg If we charge 1% and go from 100% active share to 70% active share, our hurdle rate goes from 1% to 1.42%!

blog.thinknewfound.com/2017/11/longsh…

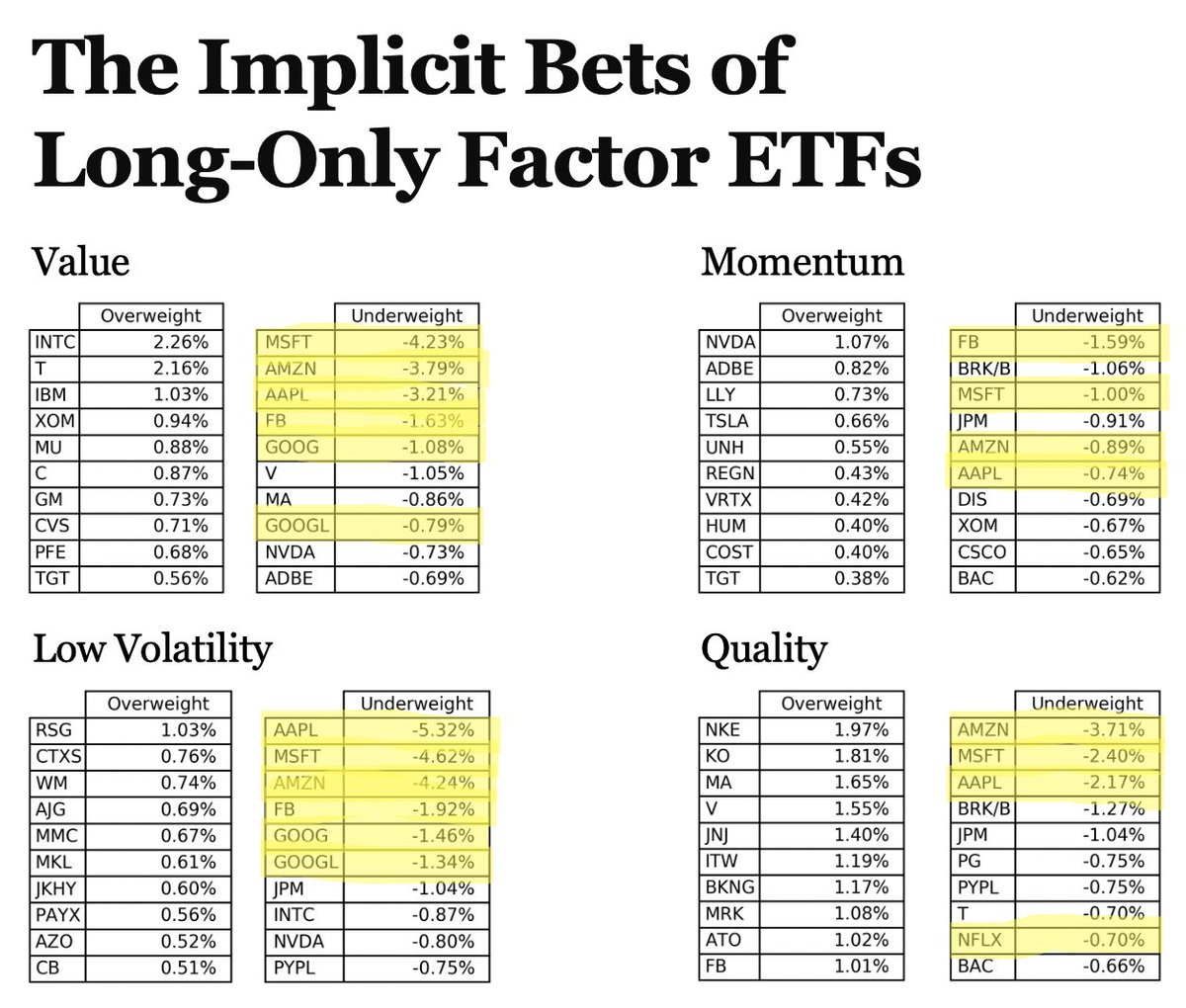

8/ Most long-only portfolios won't passively weight the top 10%, though.

Not only are FANMAG stocks on the -ve side of many factors, but their sheer size + the portfolio construction of many factor portfolios forces us to implicitly short them!

(See thinknewfound.com/style-dashboar…)

Not only are FANMAG stocks on the -ve side of many factors, but their sheer size + the portfolio construction of many factor portfolios forces us to implicitly short them!

(See thinknewfound.com/style-dashboar…)

9/ Consider a simple, equal-weight portfolio.

As FANMAG becomes a larger and larger part of the index, our equal-weight portfolio creates a larger and larger implicit short against them.

As FANMAG becomes a larger and larger part of the index, our equal-weight portfolio creates a larger and larger implicit short against them.

10/ So why have factors been under-performing?

It's not just that the factors are betting against FANMAG, but also that the construction methodology often creates an (unintended?) implicit tilt against them.

It's not just that the factors are betting against FANMAG, but also that the construction methodology often creates an (unintended?) implicit tilt against them.

11/ Which brings us back to the original picture:

Long-only investors are inherently constrained to active bets that look more like the market-cap weighted long/short than the equal-weight long/short.

Long-only investors are inherently constrained to active bets that look more like the market-cap weighted long/short than the equal-weight long/short.

12/ Here's where I'll raise a salacious question...

In some circles, it's often said that passive is distorting the market.

But here we're seeing that long-only factor investors have been structural sellers of FANMAG.

In some circles, it's often said that passive is distorting the market.

But here we're seeing that long-only factor investors have been structural sellers of FANMAG.

13/ Is it possible that increased adoption of "smart beta" has led to a steady stream of structural selling of FANMAG, actually causing them to be *under-priced* over the last 5-10 years?

I'll just lob that one out there to incite debate (riots?).

I'll just lob that one out there to incite debate (riots?).

14/ But I do think it's important to consider that any discussion of a "stock picker's market," when measured against a benchmark, cannot be absent of a discussion of the benchmark's compositions and the forced bets active investors must make.

FIN.

FIN.

cc @profplum99