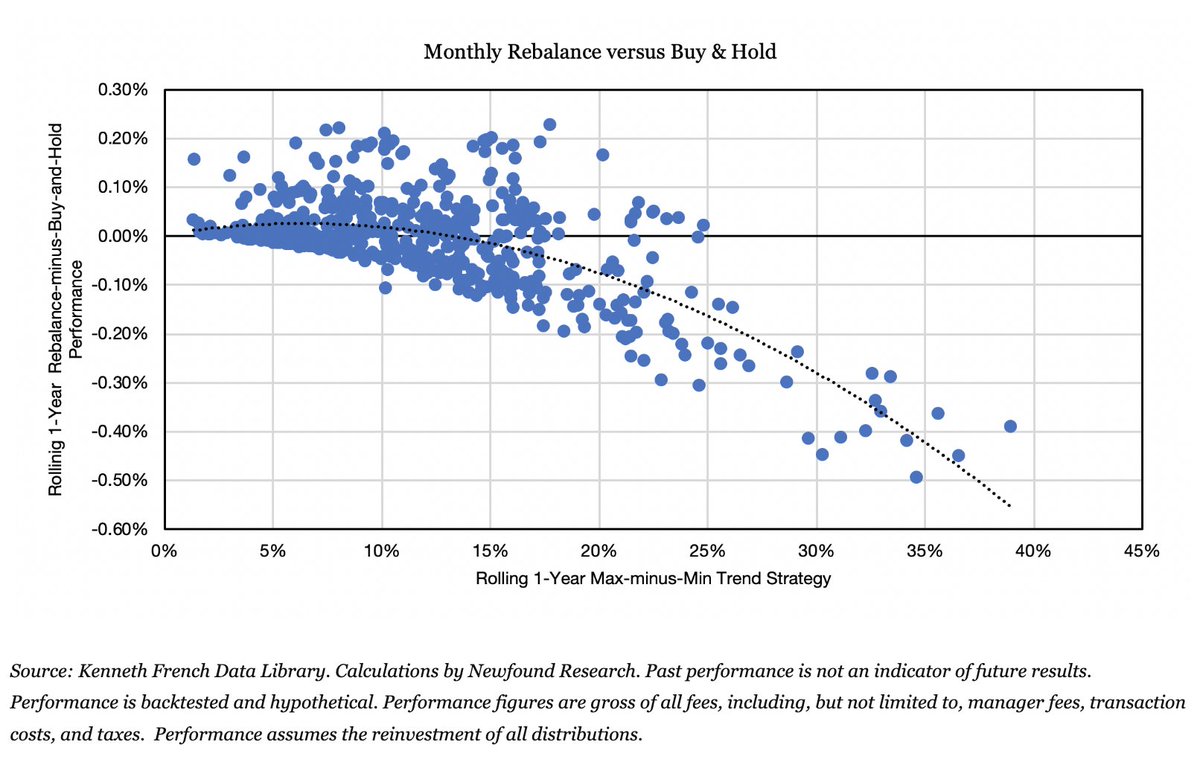

1/ So this week's research note (blog.thinknewfound.com/2019/12/timing…) was pretty brief, so I want to write a few more words about this graph, which was buried within.

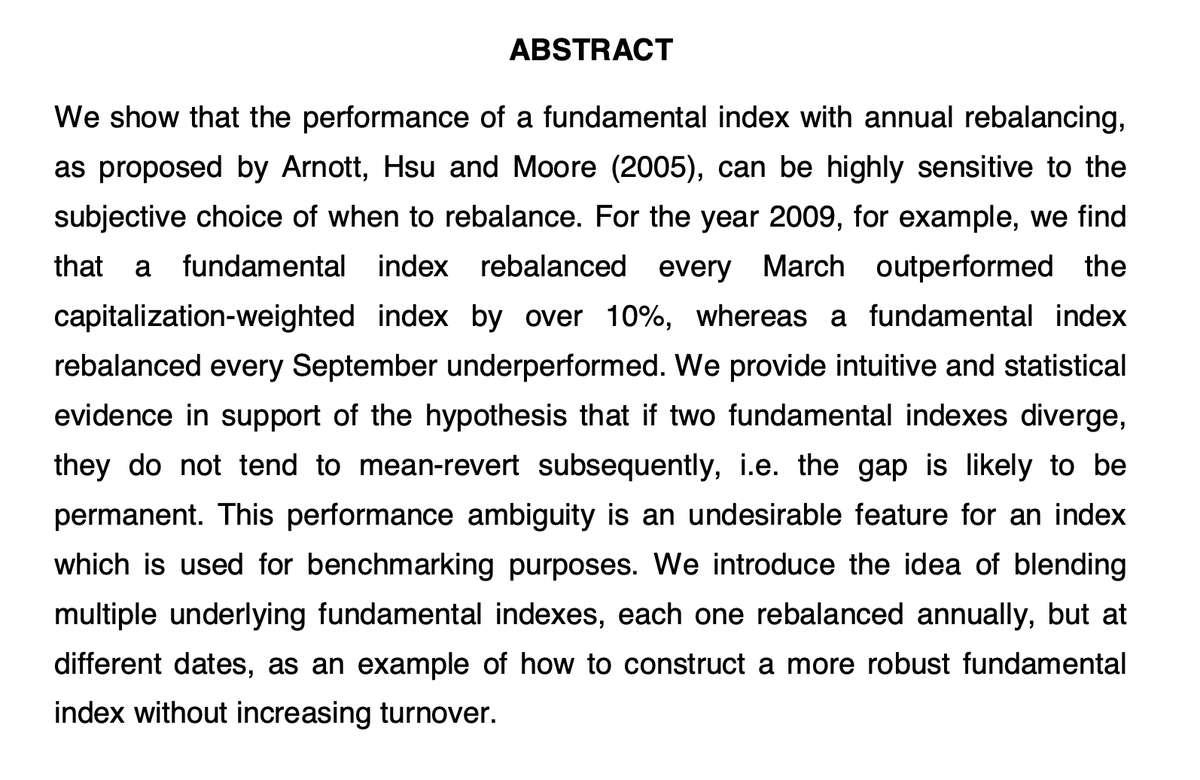

2/ This graph shows rolling 1-year returns of a multi-manager portfolio that rebalances equally across different trend managers each month versus one that lets exposures drift (reset annually).

3/ We can see a concave payoff structure: when returns between managers are extreme (x-axis), rebalancing hurts. When returns between managers are similar, rebalancing helps.

Thus, we can think of rebalancing as selling insurance against the tail risks of an individual manager.

Thus, we can think of rebalancing as selling insurance against the tail risks of an individual manager.

4/ One of the cool things about publishing research is you get feedback. This time, @paradoxinvestor's peer Winfried Hallerbach sent me his paper Disentangling Rebalancing Return (papers.ssrn.com/sol3/papers.cf…)

5/ Some interesting conclusions within:

6/ The paper then goes on to derive an approximation of the volatility return for a 1/N portfolio, which is precisely how we implemented our multi-manager portfolio.

7/ Using this equation, I estimate that a naively diversified combination of virtual trend equity managers generates 0.5% volatility return per year.

"Virtual rebalancing" is an interesting potential benefit of ensemble approaches.

"Virtual rebalancing" is an interesting potential benefit of ensemble approaches.

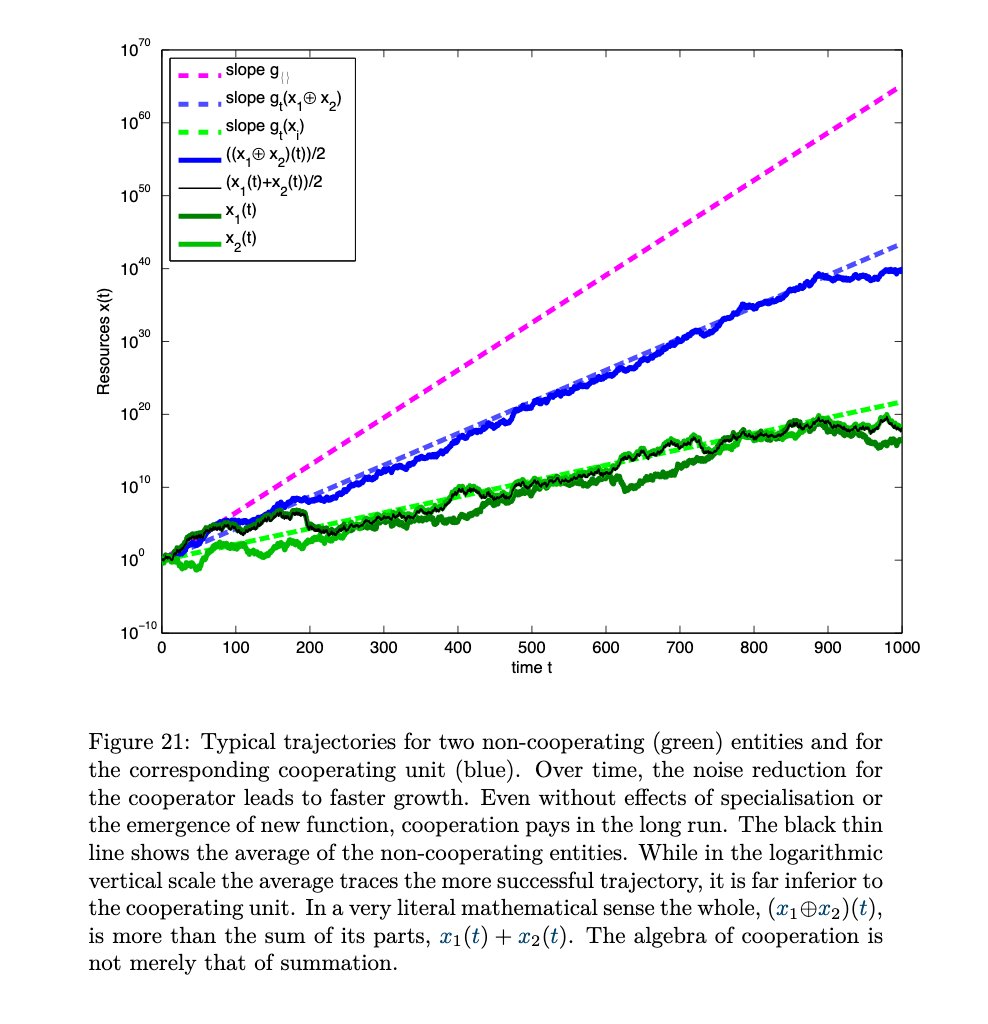

8/ In section 4.1 of the lecture notes provided by @ole_b_peters (ergodicityeconomics.com/lecture-notes/), we can see that "cooperating entities" can have a higher growth rate than selfish entities because their time-average growth rates benefit from lower volatility.

9/ Entity 1 should "cooperate" (pool + share resources; i.e. rebalance) with Entity 2 if:

10/ For our virtual managers, expected growth rates (mu) and volatility (sigma) are, ex-ante, likely to be very close and rebalancing makes sense.

But even if we believe one manager is inferior (e.g. fast trend vs slow trend), the ensemble can still benefit!

But even if we believe one manager is inferior (e.g. fast trend vs slow trend), the ensemble can still benefit!

11/ Hallerbach (2014) points out that the cost of rebalancing is the "dispersion discount."

var(g*) is the weighted variance of the securities’ growth rates around their weighted average.

var(g*) is the weighted variance of the securities’ growth rates around their weighted average.

12/ If we expect our virtual managers to all have similar growth rates, however, then we would expect the realized dispersion discount to be small.

13/ To quote Hallerbach (2014):

"However, when rebalancing is applied to a set of securities with comparable growth rates, the dispersion discount will be small and hence the volatility return is likely to dominate and generate a positive rebalancing return."

"However, when rebalancing is applied to a set of securities with comparable growth rates, the dispersion discount will be small and hence the volatility return is likely to dominate and generate a positive rebalancing return."

14/ I think this is an under-discussed potential benefit of an ensemble model approach and actually increases the hurdle rate that single-model approaches need to clear.

FIN

FIN