1. WASDE yield projections in May, June, and July always a source of market conversations/controversy. Corn yield forecast was 178.5 bpa in May and June for the US. What will it be in the July WASDE that will be released on Friday, July 10?

2. Since 2013, WASDE yield projections for May-July have been based on a crop weather regression model. In our experience, the model and how it is used is not very well understood. So we wrote a #FDD last week to try to explain the model. farmdocdaily.illinois.edu/2020/07/unders…

3. First thing to get straight is that the WASDE/WAOB May-July corn yield forecasts are model-based, while NASS Aug-Nov yield forecasts are survey-based. Completely different methodologies. Only looking at WAOB model here.

4. We first set out to replicate the original crop weather model first published in this USDA publication back in 2013. ers.usda.gov/publications/p… It does a pretty good job of explaining the modeling but some details left out.

5. Did our best to collect the data and specify variables the same as in the USDA pub. Model is actually pretty simple. Explanatory variables for US avg corn yield include: trend, planting progress, June precip shortfall, July precip, July temp.

6. We came very close but could not quite exactly replicate the original 1988-2012 regression estimation results in the USDA pub. See for yourself below. Differences probably due to slight differences in the data.

7. Next thing we wanted to do was to see if we could replicate the 2020 May and June forecast of 178.5 bpa. Updated data through 2019 and re-estimated model.

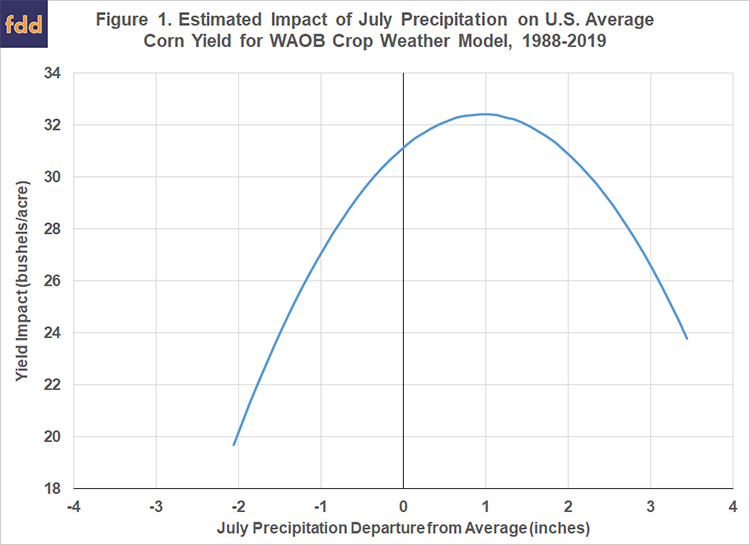

8. To forecast for 2020 using this version of the WAOB corn model, plugged in 33 for trend, 10 year avg planting progress (excluding 2019), avg July temp 1988-2019, and avg July precip. The last one is a bit tricky because July precip is a non-linear quadratic in the model.

9. Tricky think here is that we want average yield across all precip observations. This is not the point given by avg precip (zero in chart). Reason is that low precip pulls down yield more than high precip pulls it up. Details in article how we handled.

10. With the non-linear July precip adjustment, we exactly replicated the current WAOB/WASDE estimate of 178.5. Hopefully that was not just luck! Anyway, there you have it. That is how the WAOB makes its corn yield forecasts in May, June, and July.

• • •

Missing some Tweet in this thread? You can try to

force a refresh