Real Rates aren’t gonna be this low forever...Break Evens Lead with Copper. #Reflation

10 yr tsy bonds to moon trade. Crowded like 10 year Tsy Bonds to Zero crowd back in Fall ‘18..Scary Charts back then now it’s Scary Charts to Zero Yields. Truth probably somewhere in middle. CFTC Spec 10 Yr Govt. Bond Longs now ripping to +31K.. vs -756K Short in Fall 18.

#DV01

#DV01

10 Yr Break Evens.🚀

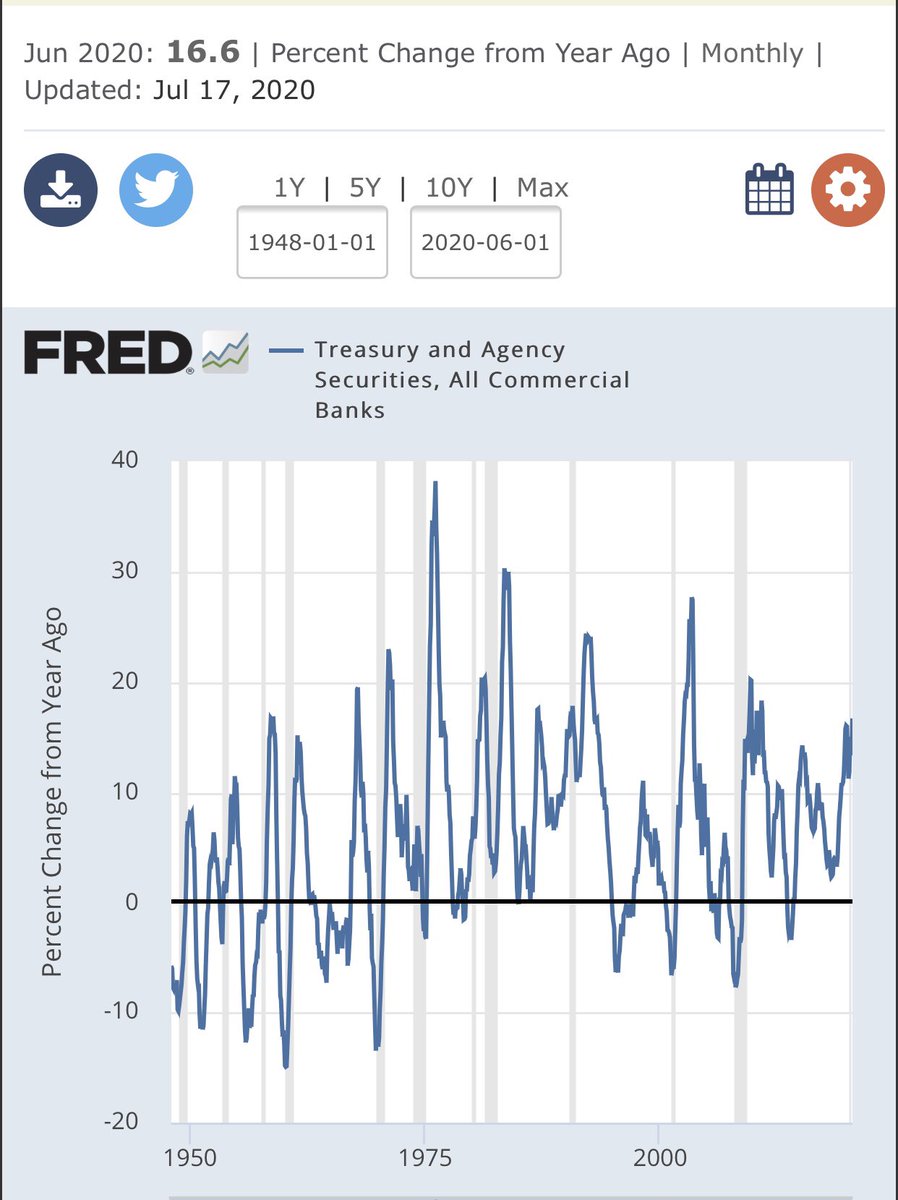

Buffett no dope...adds to Most Asset Sensitive GSIB in US this week..Literally when Long End ripping on huge bid..& unamortized Agency premium charges gonna linger in 3Q.. But Long End erasing Bad Debt with Lower Real Rates.

#RecoveryYr #Sequence

Buffett no dope...adds to Most Asset Sensitive GSIB in US this week..Literally when Long End ripping on huge bid..& unamortized Agency premium charges gonna linger in 3Q.. But Long End erasing Bad Debt with Lower Real Rates.

#RecoveryYr #Sequence

Now CFTC 10 Year Govt. Bond Contracts are at +73K Contracts... Intelligentsia still got them Long Term Charts with Yields breaking down.. just like they did back in Fall ‘18 breaking up.. it’s a Momemtum feeding frenzy.

Trades at 189x P/E.

#DV01 #Reflation

Trades at 189x P/E.

#DV01 #Reflation

3M Cross FX Basis moving back to par.. FRA OIS still flat as a pancake.

10 Year Govt Bond was trading at a 192x P/E.

Bye bye

10 Year Govt Bond was trading at a 192x P/E.

Bye bye

10 yr at 197x P/E...Like cautionary tale of getting too close to the wall of Jedi Transition..getting too close to perfection can sadly end very poorly for even the best aviators. Sometimes don’t let great get in the way of good enuff.

@BlacklionCTA #FatherCrowleyOutlook

@BlacklionCTA #FatherCrowleyOutlook

If u have been short from 100+ back in March on no Depression 2.0..now 93..u can never go broke booking a gain & cashing in..Severely over shorted with CFTC Specs now -7K..& come back later. gains can also be on econ strength as 10 yr < 200x PEs get DV01d at some point.

LIBOR OIS has now collapsed to 24bps from over 90bps back in March...there is some bank to bank risk... NII starting in 4Q20 could stabilize with better economic news. strength doesn’t have to be on weakness imho @SantiagoAuFund

#Reflation

#Reflation

• • •

Missing some Tweet in this thread? You can try to

force a refresh