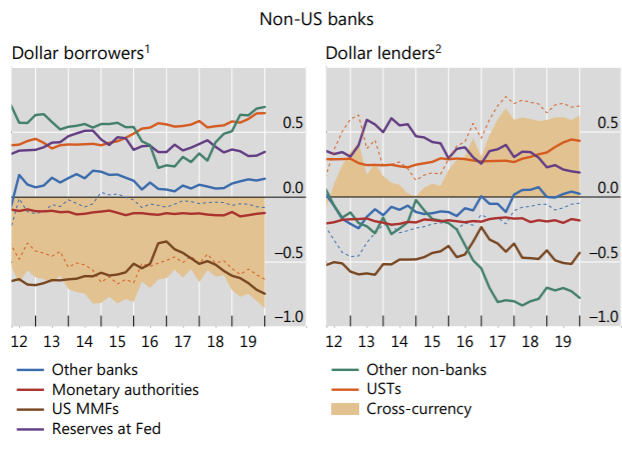

@DanielaGabor @NathanTankus @JWMason1 I am with Daniela here --

a couple of reactions to Nathan's post

a) in the first transaction, it describes what happens in the FX market if Chinese resident wants to buy fx from a US resident. At the end of the transaction, the U.S. resident has CNY, the Chinese resident USD

a couple of reactions to Nathan's post

a) in the first transaction, it describes what happens in the FX market if Chinese resident wants to buy fx from a US resident. At the end of the transaction, the U.S. resident has CNY, the Chinese resident USD

@DanielaGabor @NathanTankus @JWMason1 So a symmetric rise in both bank accounts, assuming no dealer balances.

in conventional macro/ in the "dealer flow" literature, the increased demand for dollar (deposits) from Chinese residents would induce a change in the XR.

the US resident already had all the CNY they want

in conventional macro/ in the "dealer flow" literature, the increased demand for dollar (deposits) from Chinese residents would induce a change in the XR.

the US resident already had all the CNY they want

@DanielaGabor @NathanTankus @JWMason1 So the US resident holding CNY would have a higher CNY balance than desired and would look to also sell CNY for USD (or find someone who wants CNY and has USD, say a Chinese exporter) and that puts upward presssure on the dollar (which drives a CA adjustment)

@DanielaGabor @NathanTankus @JWMason1 but let's assume that there was a symmetric increase US desire for Chinese assets and Chinese demand for US assets so the transaction takes place at unchanged exchange rates -- then you end up with the first set of accounts

@DanielaGabor @NathanTankus @JWMason1 from a BoP point of view the second transaction (Chinese resident changing from dollar deposits to US equity) is BoP neutral. Chinese resident changes the form of the claim on the US but there is no increase in total claims on the US. A US resident trades a US equity for USD

@DanielaGabor @NathanTankus @JWMason1 There tho is no offsetting change in US holdings -- US residents still hold a CNY deposit.

so then you have an increase in both countries gross positions -- with the NIIP influenced by the relative movement of the CNY (on the US deposit) and US stocks (for the Chinese resident).

so then you have an increase in both countries gross positions -- with the NIIP influenced by the relative movement of the CNY (on the US deposit) and US stocks (for the Chinese resident).

@DanielaGabor @NathanTankus @JWMason1 So far though there has been no transaction involving the current account -- this is just an asset swap (americans giving up US equity returns for CNY currency returns).

for the current account one of the parties needs to sell to an exporter/ importer

for the current account one of the parties needs to sell to an exporter/ importer

@DanielaGabor @NathanTankus @JWMason1 In my example, the US resident with a CNY claim on China that it doesn't want might sell to a Chinese exporter whose received dollars in exchange for goods (current account) and wants CNY (to pay salaries).

then the US resident ends up with a new dollar deposit (and no CNY)

then the US resident ends up with a new dollar deposit (and no CNY)

@DanielaGabor @NathanTankus @JWMason1 China ends up with an equity claim, and higher exports (everything balances Financial inflow funds current account outflow rather than a financial outflow)

symmetric financial flows is one outcome but not the only outcome --

symmetric financial flows is one outcome but not the only outcome --

@DanielaGabor @NathanTankus @JWMason1 the overall narrative has echos of a couple strands of fairly conservative thought --

this is Stephen Roach to my ears

"its import spending growth in the United States outpacing import spending growth in these countries which drives the gap between them" -

this is Stephen Roach to my ears

"its import spending growth in the United States outpacing import spending growth in these countries which drives the gap between them" -

@DanielaGabor @NathanTankus @JWMason1 US CA deficit all all high US consumption/ low US savings -- the rest of the world via its exchange rate policies and different fiscal policies has nothing to do with US balance

(Bernanke noted that if this was the case US rates should be high not lowish .. but set that aside)

(Bernanke noted that if this was the case US rates should be high not lowish .. but set that aside)

@DanielaGabor @NathanTankus @JWMason1 and the notion that a financial inflow generates an offsetting financial outflow (absent new information that changes market prices) comes from the efficient market hypothesis --

in a strong version of that fx intervention by a central bank has no impact on the XR ...

in a strong version of that fx intervention by a central bank has no impact on the XR ...

@DanielaGabor @NathanTankus @JWMason1 As Chinese central bank purchases of US assets say drive an equal financial outflow (private US investors hold more Chinese assets) and there is no change in the XR or change in the current account. markets are perfect, they only adjust to new information not to mere flow ...

@DanielaGabor @NathanTankus @JWMason1 I think Gagnon et al effectively refuted this empirically, and the notion that market participants have natural habitats and inducing them out of their comfort zone takes changes in price + frictions across borders (currencies, legal, regulatory) reinforce.

my two cents

my two cents