Watching Fin TV just makes my head hurt.. it’s like nothing about fundamentals just stuff like Put/Call ratio ad nauseum.

... all Fed support... market propped up.. they just refuse to look at economic or earnings fundamentals... just take a look at .. or so many other cyclicals that are ratifying.. Retail Sales, PMIs, Housing HPI, Housing Starts, Mortg Apps, IP Up off trough (lag orders)...

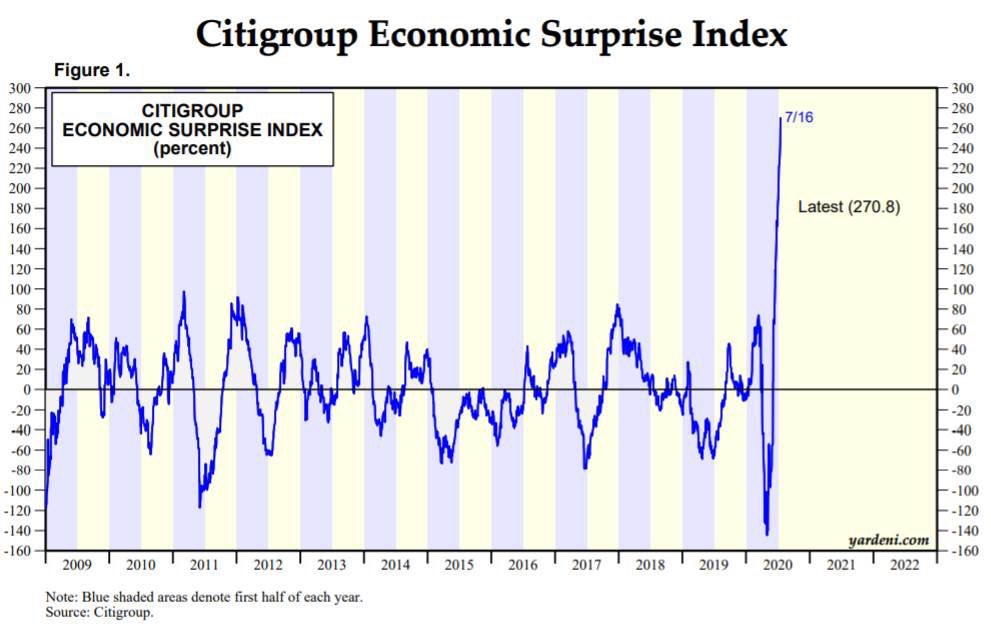

.. Capex orders turning, U Michigan inflation exp up to 3+%. Jobless Claims declining substantially, Savings Rate 33->23% still high but speeding up, Commodities ripping, Inventory high but coming down... Look at this Chart! Geez..👇👇👇👇👇👇👇👇

This is the economy👇👇👇👇👇👇

This is the economy👇👇👇👇👇👇

For someone to look at this chart & say the stock market is disconnected from the market is delusional... Just stop already. This is a V off trough.

👇👇👇👇👇👇👇👇👇👇👇👇

#RateOfChange

👇👇👇👇👇👇👇👇👇👇👇👇

#RateOfChange

• • •

Missing some Tweet in this thread? You can try to

force a refresh