Glad @mengxilu flagged this. Affirm's rated securitization is a great spring board to chat (type?) about FinTech capital markets, valid-when-made and true lender issues.

Lots of recent developments in this space. Anyone else up for a thread? Then let's read on!

Lots of recent developments in this space. Anyone else up for a thread? Then let's read on!

As a baby lawyer, I worked on MSB, CDO and eventually ABS card and auto deals. I was both law firm and in-house counsel. And I dealt with Reg AB, SEC Form ABS-15G reporting and also how to deal with risk retention.

ABS or asset-backed securitization has long been a critical funding tool for non-bank lenders, and even fledgling bank lenders.

Capital One, where I worked in 2011 and 2012, regularly funded its card portfolio via ABS. It was such an important and low-cost funding tool that at certain points they were issuing ABS notes several times a month. Their docs are here ir-capitalone.gcs-web.com/abs-reporting

A lot of chatter on Twitter about neo banks buying bank charters. But the money’s not in deposits. It’s in lending. Watch who’s doing heavy ABS issuance as a sign of which FinTech is likely to fish for a bank charter.

Anyway, back to ABS issuance. 2009 through 2013 was a goofy period for MBS, card and auto deals. Large banks were awash in cheap deposits and it was more expensive for most of that period to do ABS deals. See Cap One with no Class A issuance.

Things picked back up in 2014. Hedge funds, family offices and others were looking for yield. In addition to ABS, they started to buy up all types of FinTech assets.

LC, Prosper, Square and others started to sell structured notes, MCAs, whole loans and everything in between to funds like Colchis, Moore, Victory Park and Stoneridge.

Then the spring of 2015 hit, and it sucked.

In Spring 2015, a series of cases now called Madden v. Midland started to spring up in NY.

The initial case was a woman (Madden) suing Midland Funding, LLC (Midland). Midland was a debt collection agency. Madden was a credit card debtor living in New York state.

Madden was initially a customer of BofA, with whom she opened a credit card account. By 2008, Madden owed ~$5k in uncollectable debt.

As is common, the lender (now FIA Card Services, N.A., due to some re-orging by BofA) sold off Madden’s debt.

Oh yeah, that’s right -- I said (typed?) sold.

For those of you who have never lost track of a debt, or haven’t had the pleasure of phantom debt, you may not know that lots of lenders sell their charged off debt.

Side tangent -- Ebay is currently trying to collect $8 from me due to me not watching my longstanding listing of a TMNT Casey Jones toy from the 90s (still in box, please stop bidding full listing price to ding me the fees).

Back to banking -- Past due for too long? Banks and other lenders will sell the debt for pennies on the dollar to specialized debt collection firms.

Those firms then do all sorts of things, politely categorized as “squeezing blood from stones” to try and get about 3x what they paid for the bad debt.

It’s a big business and sometimes sleazy. But not everyone is bad. @ohad’s @trueaccord is working hard to offer a consumer-friendly alternative. Here's a pic of Ohad from his Insta.

So back to this Madden thing. There’s Madden, not paying her bills, when in 2010 Midland (who bought her debt) swoops in and hits her with a letter saying she owed $5K PLUS an extra 27% interest per year. But this is where Midland got into trouble.

This is nuanced and worth repeating - Midland charged *EXTRA* interest on top of what BofA/FIA had charged Madden. They weren’t just squeezing blood from stones. They were squeezing blood from the blood of stones.

(Midland also had bad lawyers - plug to always hire good lawyers)

(Midland also had bad lawyers - plug to always hire good lawyers)

So Madden does what any good red-blooded American does. She pays her debts!

Just Kidding!

She sues!

And she claims Midland is subject to (and violating) NY Usury laws, and also the Fair Debt Collection Practices Act.

She sues!

And she claims Midland is subject to (and violating) NY Usury laws, and also the Fair Debt Collection Practices Act.

Quick tangent on Usury. It’s a law that says any fees over a certain interest rate are unconscionable and illegal. You usually get a civil cap, then a slightly higher criminal cap.

I'm only barred to practice in NY, but as a friend I can tell you try not to violate usury laws.

I'm only barred to practice in NY, but as a friend I can tell you try not to violate usury laws.

(Still on tangent) A lot of states have usury laws. But banks get a special power to “preempt” state laws with the laws of their home states. This comes from various federal laws. Another thread for another time.

(Tangent, still) Ever notice your credit card mail comes from Ohio (Chase), Delaware (Barclays) or South Dakota (Citi)? It’s because they have pro-bank usury laws. Banks HQ'ed there can rip your face off with interest, and its lawful!

(They don't, but the pic is still fun)

(They don't, but the pic is still fun)

(End tangent, back to Madden v. Midland)

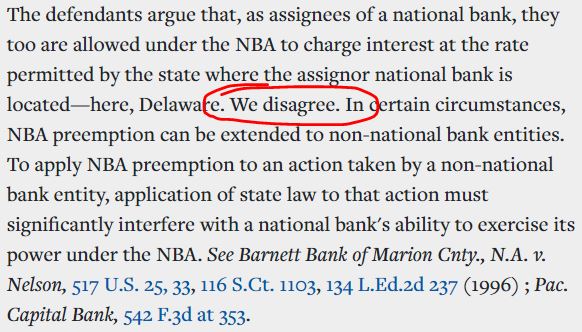

Midland initially gets the case dismissed. They bought the debt from a bank. Bank debt is -- key term coming up -- “Valid when made.”

Midland initially gets the case dismissed. They bought the debt from a bank. Bank debt is -- key term coming up -- “Valid when made.”

“Valid when made” means the asset is good + enforceable even after its sold. You get to take the debt and enforce it as if you had all the same powers of the bank.

Powers like . . . preempting NY’s interest rate laws with those of Delaware (where BofA and FIA had set up shop).

Powers like . . . preempting NY’s interest rate laws with those of Delaware (where BofA and FIA had set up shop).

Come close -- I’m going to let you in on a secret.

Valid-when-made underpins the supermajority of debt in the U.S.

Get a mortgage? Most often it's sold to Fannie or Freddie. They’re not banks, but it’s OK because the loan note was . . . valid when made!

Get a credit card? That debt is often sold into securitization trusts like Capital One’s. The trust gets to collect on your debt when you don’t pay because the debt was . . . valid when made!

Sound good. But then in May 2015, an appeals court hears Madden’s appeal and *record scratch* stops the party and shits in everyone’s punch bowl.

Before they left the turd, they politely affirmed that banks can do whatever they want with interest rates. But then they hiked up their robes, dropped their shorts and proceeded to poop on valid when made.

See, the key standard on whether federal banking laws preempt state law depends on whether the state law interferes with a bank’s ability to be a bank.

Here's the appeals court in Madden affirming that.

Here's the appeals court in Madden affirming that.

But then they did the turd thing. In Madden, the appeal court looked around and was like “oh, the bank can just keep its debt . . . so we don’t need to preempt usury for third-party debt collectors.”

They basically said “valid when made . . . but only sometimes.”

Now the decision is nuanced, and the court didn’t say Madden won. There was a choice-of-law claim to decide. New York doesn’t license debt collectors, so technically Midland could have prevailed in its claim to say Delaware law should have applied. But the damage was done.

I was closing a partnership for SMB lending in May 2015. And also working on capital markets deals to buy SMB assets. The counsel, banks and hedge funds on the other side made it out like the sky was falling and we were all going to die.

(pic of my response to them at the time)

(pic of my response to them at the time)

The next few months sucked. I spent weeks explaining how Midland was charging EXTRA interest (remember 73 tweets ago?). Our product only collected what the bank had charged. And under choice of law, most states would find Utah law applies due to lack of state licensing reqs.

We closed those deals. And you know what -- the sky didn’t fall. Especially not for SMB lending.

There’s a couple of reasons for this. The first is that most SMB lenders deploy arbitration clauses. An airtight arbitration clause forces clown-like class actions like Madden into arbitration where you can win in front of a rationale panel of arbitrators.

The second is most SMB lenders don’t squeeze blood from stones. We don't harrass folks. We don't try and charge extra. We seek what's owed.

How did Midland turn out? They appealed to the Supreme Court. The executive branch, including OCC, asked the Court to take the case. The court said no thanks. I think largely due to being pissed that the Senate hadn’t filled Scalia’s seat.

Side tangent. When Scalia died, the Supreme Court took a lot fewer cases. I think they basically went on strike in response to Mitch McConnell playing politics with their roster.

That was 2016. A few weeks ago in 2020, both the OCC and FDIC finally stepped in to fill the void on this topic with a rulemaking. Valid-when-made is now officially blessed by both agencies.

This is important because under other Supreme Court precedent (Chevron), agency rules have deference and the force of law. This is as good as a law from Congress. And it fixes the key issue in Madden.

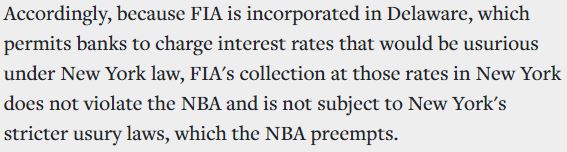

So what does this have to do with Affirm’s ABS issuance? Let’s tie it back together.

Affirm originates its installment (or instalment for you Brits and Swedes) loans via Cross River Bank and Celtic Bank.

When it puts those loan assets into its securitization trusts, those assets are now deemed valid-when-made. That means the next dead beat like Madden can’t weasel out of the debt by claiming Affirm’s note can’t be enforced because Affirm (and its ABS trust) aren’t banks.

So happy ending, right? Maybe.

Just like Prince Eric has yet to learn he married an underage princess, there’s one more issue lurking in the capital markets -- true lender.

What’s the deal with true lender? We’ll cover that another day ;)

What’s the deal with true lender? We’ll cover that another day ;)