1/ Flirting with Models (thinknewfound.com/podcast) Season 3 is officially over.

A deep thank you to my guests, all who listened, and @MathewPassy for his unbelievable editing.

I thought I'd do a quick thread on something I learned from each episode.

A deep thank you to my guests, all who listened, and @MathewPassy for his unbelievable editing.

I thought I'd do a quick thread on something I learned from each episode.

2/ Quantifying Conviction with @AQISinvest

Position size is not a great measure of a manager's conviction; we have to normalize against that manager's behavior incentives.

A small, off-style position put on late in the year could mean a lot.

blog.thinknewfound.com/podcast/s3e1-k…

Position size is not a great measure of a manager's conviction; we have to normalize against that manager's behavior incentives.

A small, off-style position put on late in the year could mean a lot.

blog.thinknewfound.com/podcast/s3e1-k…

3/ Evolving Long/Short Equity with @michaelbkrause

Look-ahead bias can be an effective means of measuring the upper limits of your portfolio construction process.

blog.thinknewfound.com/podcast/s3e2-m…

Look-ahead bias can be an effective means of measuring the upper limits of your portfolio construction process.

blog.thinknewfound.com/podcast/s3e2-m…

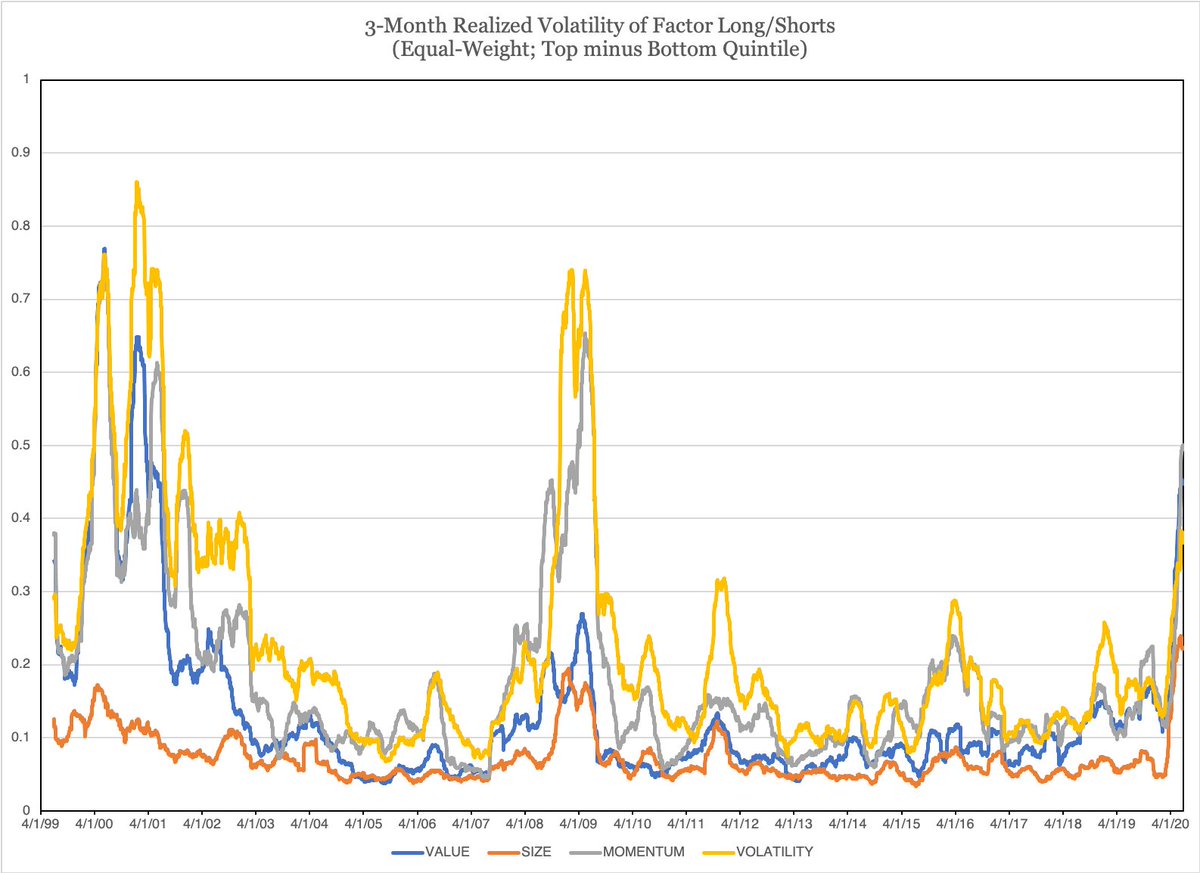

4/ Bad Ideas with @bennpeifert

Options aren't as simple as "I think it's going up" or "I think it's going down." You can get the direction correct and still lose money on your position (see )

blog.thinknewfound.com/podcast/s3e3-b…

Options aren't as simple as "I think it's going up" or "I think it's going down." You can get the direction correct and still lose money on your position (see )

blog.thinknewfound.com/podcast/s3e3-b…

5/ Tactical Asset Allocation with @JimMasturzoII

Building candidate portfolios that emphasize certain regimes or attributes can be an effective way of identifying assets with out-sized sensitivities or portfolio impacts.

blog.thinknewfound.com/podcast/s3e4-j…

Building candidate portfolios that emphasize certain regimes or attributes can be an effective way of identifying assets with out-sized sensitivities or portfolio impacts.

blog.thinknewfound.com/podcast/s3e4-j…

6/ Tail Reaper with @chanep

Intra-day trend following seeks to exploit the hedging / de-risking of institutional players that must happen during market hours.

blog.thinknewfound.com/podcast/s3e5-e…

Intra-day trend following seeks to exploit the hedging / de-risking of institutional players that must happen during market hours.

blog.thinknewfound.com/podcast/s3e5-e…

7/ Commodity Convexity with @jeff_l_baird

When building a portfolio of convex positions, a correct directional bet means a position becomes less convex and introduces greater delta risk, requiring a manager to "re-convexify" their portfolio.

blog.thinknewfound.com/podcast/s3e6-j…

When building a portfolio of convex positions, a correct directional bet means a position becomes less convex and introduces greater delta risk, requiring a manager to "re-convexify" their portfolio.

blog.thinknewfound.com/podcast/s3e6-j…

8/ All-Weather Portfolios with Trend Following with Eric Crittenden

CTA portfolio robustness can be tested by removing different futures markets and sectors and re-running backtests.

blog.thinknewfound.com/podcast/s3e7-e…

CTA portfolio robustness can be tested by removing different futures markets and sectors and re-running backtests.

blog.thinknewfound.com/podcast/s3e7-e…

9/ Full Stack Machine Learning with @madsingwar and Martin Oberhuber.

"How do you calculate the covariance matrix?" may be one of the best questions you can ask a quant firm.

blog.thinknewfound.com/podcast/s3e8-m…

"How do you calculate the covariance matrix?" may be one of the best questions you can ask a quant firm.

blog.thinknewfound.com/podcast/s3e8-m…

10/ Institutional Trends in Factor Investing with Michael Hunstad

Unintended bets can plague factor construction. When combining multiple factors, you have to think about which parts of the distribution to use to best match turnover speeds.

blog.thinknewfound.com/podcast/s3e9-m…

Unintended bets can plague factor construction. When combining multiple factors, you have to think about which parts of the distribution to use to best match turnover speeds.

blog.thinknewfound.com/podcast/s3e9-m…

11/ Alternative Risk Premia with Sandrine Ungari

Explicit risk transfer from banks to institutional investors (e.g. offloading risk at a discount for regulatory reasons) may be a new, interesting frontier of alternative risk premia.

blog.thinknewfound.com/podcast/s3e10-…

Explicit risk transfer from banks to institutional investors (e.g. offloading risk at a discount for regulatory reasons) may be a new, interesting frontier of alternative risk premia.

blog.thinknewfound.com/podcast/s3e10-…

12/ Quant-Aware Discretionary with Omer Cedar

Discretionary managers should explicitly focus on trying to harvest idiosyncratic risk and utilize factor models to recognize the latent style risks that may add meaningful unintended bets.

blog.thinknewfound.com/podcast/s3e11-…

Discretionary managers should explicitly focus on trying to harvest idiosyncratic risk and utilize factor models to recognize the latent style risks that may add meaningful unintended bets.

blog.thinknewfound.com/podcast/s3e11-…

13/ Positional Option Trading with @SinclairEuan

Equity factors may represent an interesting source of return for option traders as well.

blog.thinknewfound.com/podcast/s3e12-…

Equity factors may represent an interesting source of return for option traders as well.

blog.thinknewfound.com/podcast/s3e12-…

14/ "...But Not So Open Your Mind Falls Out" with @CliffordAsness

"The more risk you take out, the more leverage you need." e.g. Not taking industry bets may be great, but it might require more leverage to hit the same return as before.

blog.thinknewfound.com/podcast/s3e13-…

"The more risk you take out, the more leverage you need." e.g. Not taking industry bets may be great, but it might require more leverage to hit the same return as before.

blog.thinknewfound.com/podcast/s3e13-…

15/ Thank you again to all my guests and for everyone who has taken the time to listen.

If you have the time, we'd sincerely appreciate it if you'd share the podcast with a friend and give us a rating or review on iTunes (podcasts.apple.com/us/podcast/fli…).

If you have the time, we'd sincerely appreciate it if you'd share the podcast with a friend and give us a rating or review on iTunes (podcasts.apple.com/us/podcast/fli…).