The following thread will set out my summary responses to the briefing statement given to MPs in response to NC1 and NC31.

This should be read with my even more concise summary in an earlier tweet.

This should be read with my even more concise summary in an earlier tweet.

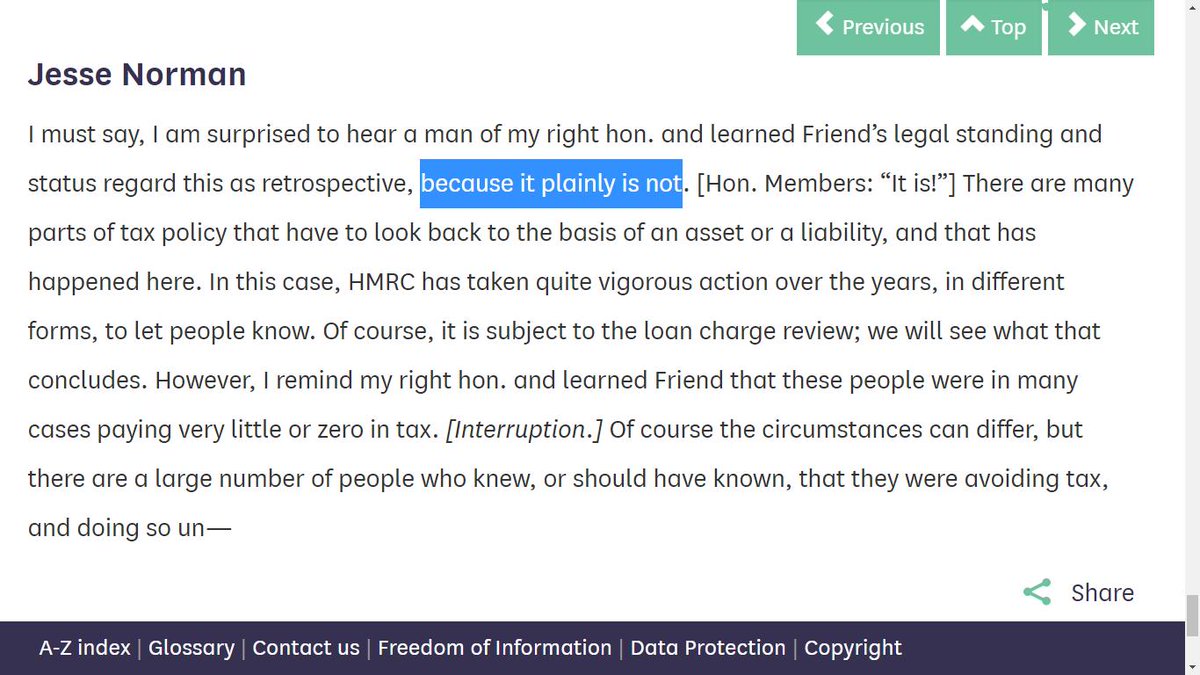

On NC1, the briefing note carefully sidesteps the well-known flaws in aspects of the Morse Review.

It also implies that a Government report would be adequate. It forgets the whitewash report given in early 2019 which, despite its flaws, was still effectively debunked by Morse.

It also implies that a Government report would be adequate. It forgets the whitewash report given in early 2019 which, despite its flaws, was still effectively debunked by Morse.

On NC31 – bullet 1

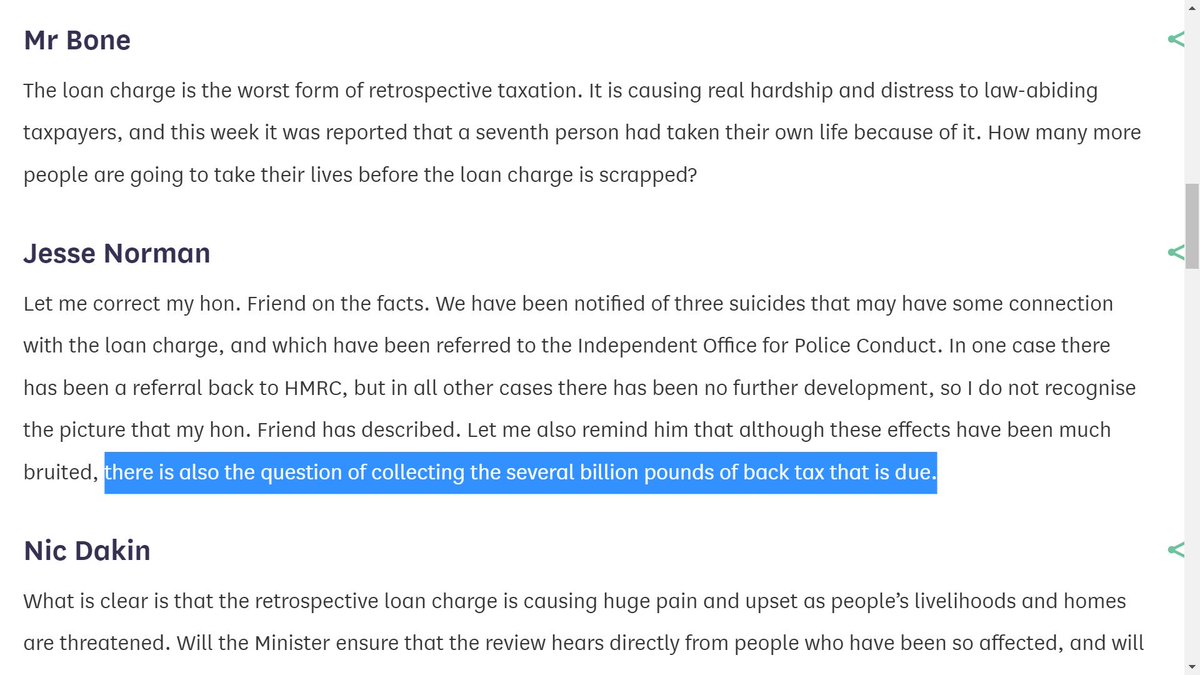

•Emphasises avoidance and offshore trusts for political effect.

•Ignores the fact that the loan charge has done nothing to curb these schemes.

•Emphasises avoidance and offshore trusts for political effect.

•Ignores the fact that the loan charge has done nothing to curb these schemes.

On NC31 – bullet 2

•Suggests that HMRC cannot make an assessment without knowledge of a taxpayer’s state of mind.

•Ignores the fact that this is already a standard and long-established rule elsewhere in the tax code, where HMRC can make an assessment based on ...

•Suggests that HMRC cannot make an assessment without knowledge of a taxpayer’s state of mind.

•Ignores the fact that this is already a standard and long-established rule elsewhere in the tax code, where HMRC can make an assessment based on ...

... what they believe to be a person’s knowledge.

•This is a wholly disingenuous reason for objecting to NC31.

•This is a wholly disingenuous reason for objecting to NC31.

On NC31 – bullet 3

•This is a non-sequitur.

•It overlooks the fact that the loan charge was an additional provision to cast aside standard safeguards applicable to all other taxpayers (even those who have participated in tax avoidance schemes).

•NC31 does not allow ...

•This is a non-sequitur.

•It overlooks the fact that the loan charge was an additional provision to cast aside standard safeguards applicable to all other taxpayers (even those who have participated in tax avoidance schemes).

•NC31 does not allow ...

...any taxpayers to “escape tax” but simply restores their right to the usual range of statutory safeguards.

On NC31 – bullet 4

•Repeats reference to avoidance and offshore trusts for political effect.

•Repeats misstatement that NC31 exempts taxpayers from tax. It exempts them only from the loan charge leaving them exposed to HMRC’s full range of assessment powers, subject to ...

•Repeats reference to avoidance and offshore trusts for political effect.

•Repeats misstatement that NC31 exempts taxpayers from tax. It exempts them only from the loan charge leaving them exposed to HMRC’s full range of assessment powers, subject to ...

... the standard range of statutory safeguards.

•The final sentence is just plain wrong. If HMRC had knowledge of knowing evasion by HMRC, the taxpayer would not be protected by NC31

•The final sentence is just plain wrong. If HMRC had knowledge of knowing evasion by HMRC, the taxpayer would not be protected by NC31

On NC31 – bullet 5

•Re the first part “intent”, see objections to bullet 1.

•Re the second part of the sentence “removes everybody”, it overlooks the fact that NC31 was limited to pre-April 2016 loans.

•The final part of the sentence (after semicolon) is just meaningless.

•Re the first part “intent”, see objections to bullet 1.

•Re the second part of the sentence “removes everybody”, it overlooks the fact that NC31 was limited to pre-April 2016 loans.

•The final part of the sentence (after semicolon) is just meaningless.

• • •

Missing some Tweet in this thread? You can try to

force a refresh