1/2

Fantastic news from #SRB this morning. Having now achieved "the most critical stage" of the licensing for Coringa, the path is now open to a doubling of production.

This company makes $3.5m profit a quarter at 8,500 oz production and $1,710 gold

londonstockexchange.com/news-article/S…

Fantastic news from #SRB this morning. Having now achieved "the most critical stage" of the licensing for Coringa, the path is now open to a doubling of production.

This company makes $3.5m profit a quarter at 8,500 oz production and $1,710 gold

londonstockexchange.com/news-article/S…

2/2

I don't believe gold goes below that fig. in Q4 before pushing onto new highs.

A return to 11,000 oz in Q4/Q1 2021 will see SRB making significantly higher profits/cash flows, lowering their debt needs for Coringa.

If all goes to plan, I expect big things in 2021.

I don't believe gold goes below that fig. in Q4 before pushing onto new highs.

A return to 11,000 oz in Q4/Q1 2021 will see SRB making significantly higher profits/cash flows, lowering their debt needs for Coringa.

If all goes to plan, I expect big things in 2021.

2A

A further note on #SRB after yesterday's brief post.

"MANAGEMENT’S DISCUSSION AND ANALYSIS

For the 3 and 6 month periods

ended 30 June 2020" page 14 ;

Dated 4th August.

A further note on #SRB after yesterday's brief post.

"MANAGEMENT’S DISCUSSION AND ANALYSIS

For the 3 and 6 month periods

ended 30 June 2020" page 14 ;

Dated 4th August.

2B

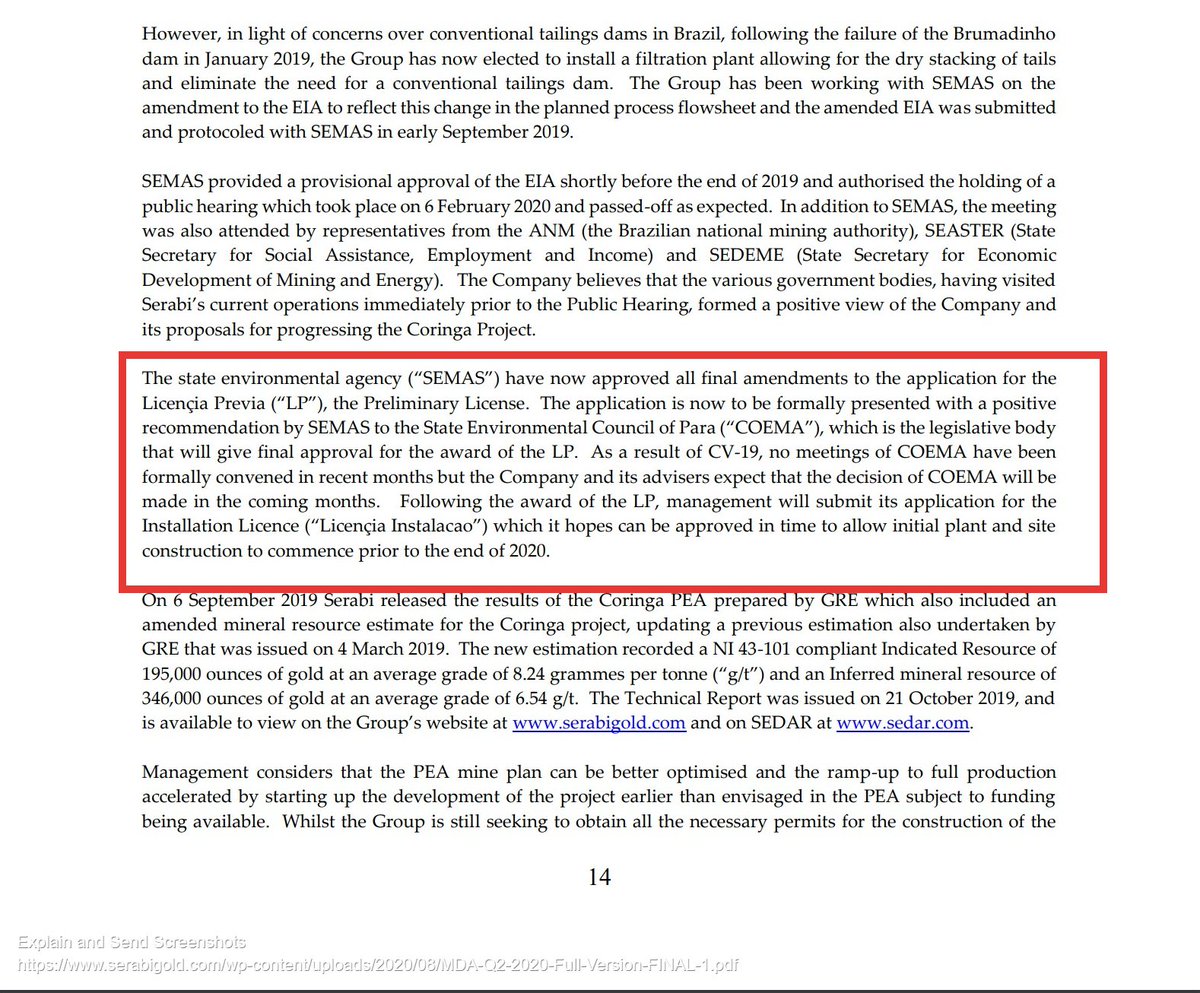

"expect that the decision of COEMA will be made in the coming months" Received c. 2 months later.

"Following the award of the LP, management will submit its application for the Installation Licence....hopes can be approved in time..."

"expect that the decision of COEMA will be made in the coming months" Received c. 2 months later.

"Following the award of the LP, management will submit its application for the Installation Licence....hopes can be approved in time..."

2C

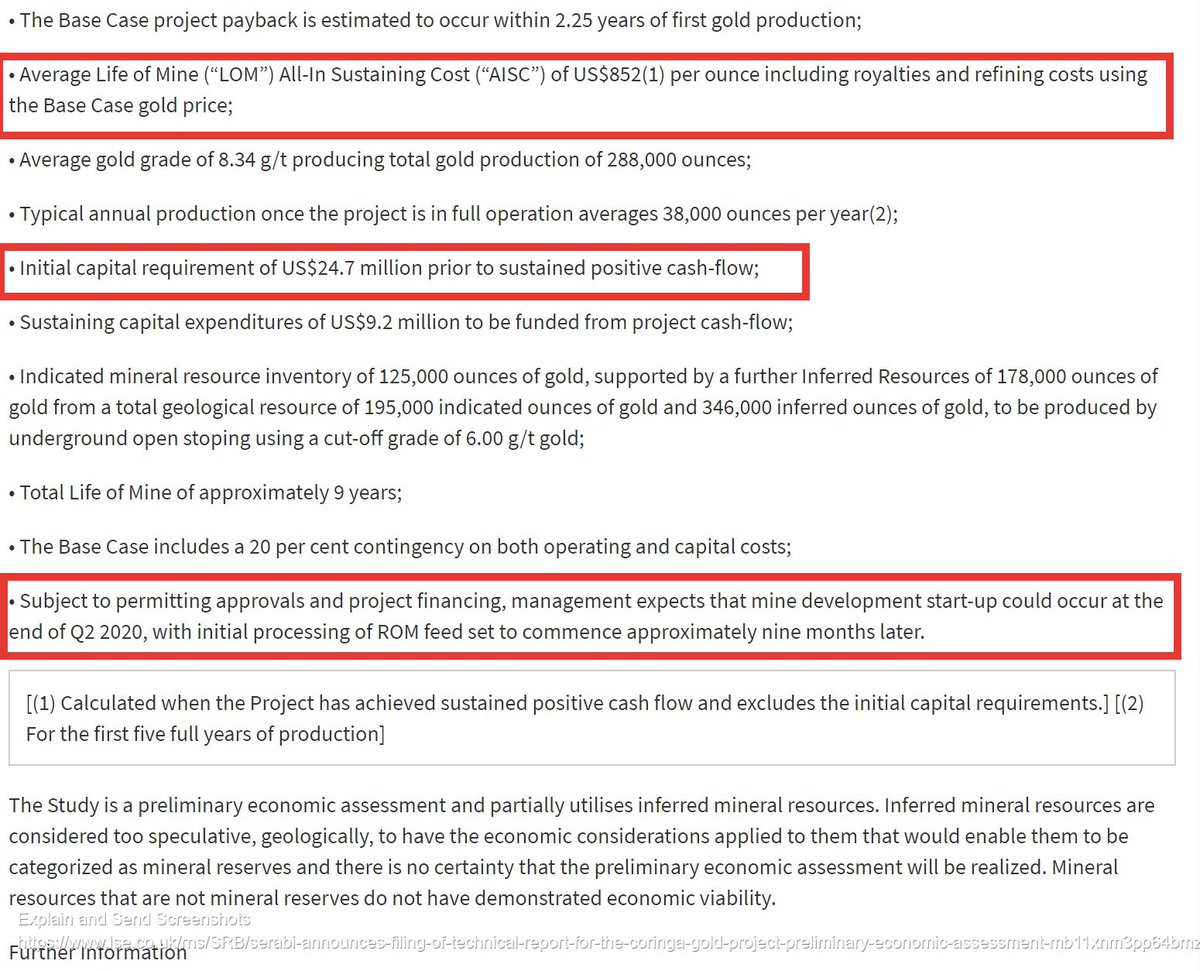

"to allow initial plant and site construction to commence prior to the end of 2020."

SRB Economic Assessment RNS dated 21st Oct 2019 ;

"initial processing of ROM feed set to commence approximately nine months" after "mine development start-up."

"to allow initial plant and site construction to commence prior to the end of 2020."

SRB Economic Assessment RNS dated 21st Oct 2019 ;

"initial processing of ROM feed set to commence approximately nine months" after "mine development start-up."

2D

So Coringa could deliver first gold by early Q4 2021.

Back to the Management discussion page 10 ;

Full production is c. 12k oz. In this price environment, anything over 10k oz is high impact, given Coringa is just $24.7m full at full buil costs.

So Coringa could deliver first gold by early Q4 2021.

Back to the Management discussion page 10 ;

Full production is c. 12k oz. In this price environment, anything over 10k oz is high impact, given Coringa is just $24.7m full at full buil costs.

2E

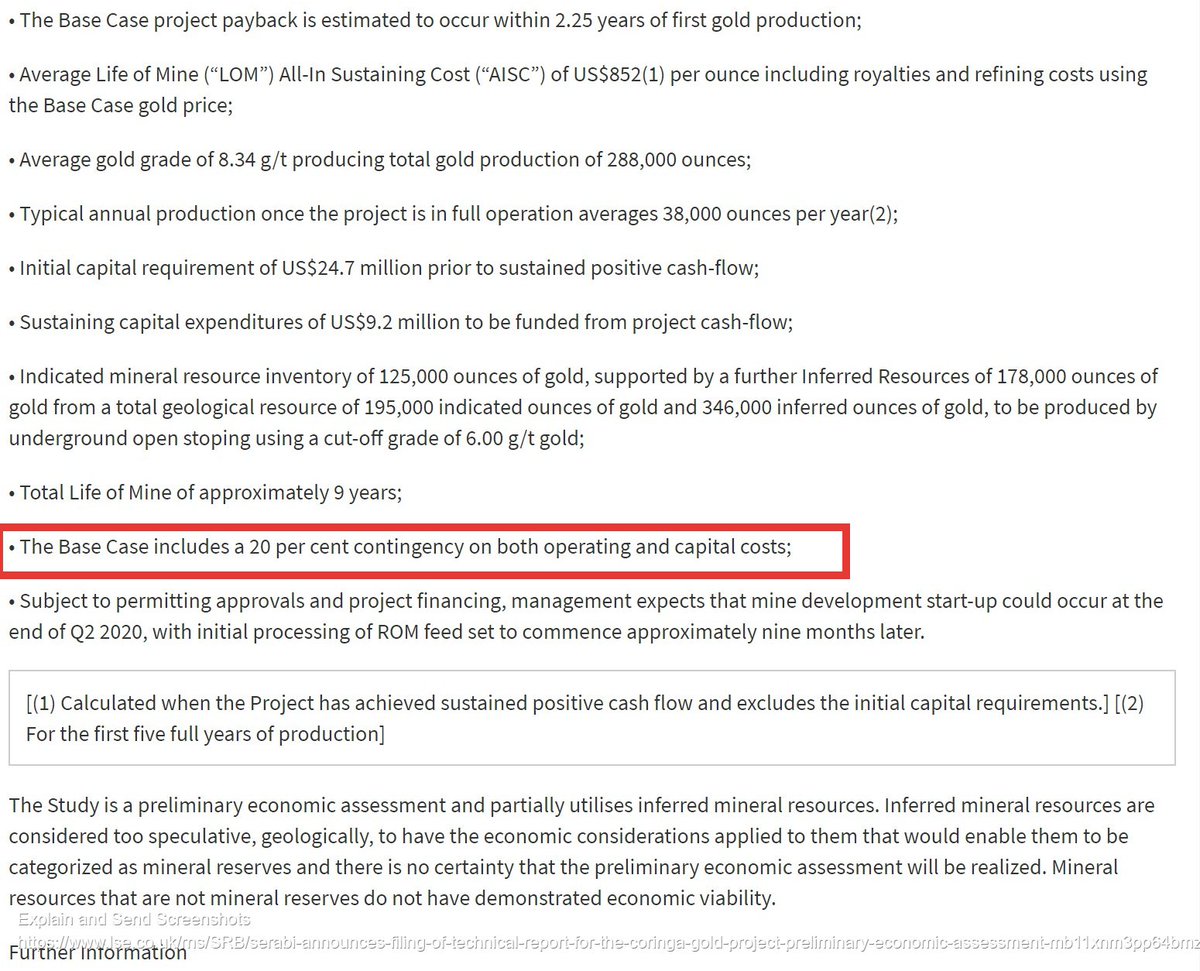

However, SRB are clear that they have already built a similar mine at Palito, so the "20 per cent contingency on both operating and capital costs" in the Oct PEA, is not to be sniffed at or easily dismissed.

At $20m build costs and debt options for at least half of it,

However, SRB are clear that they have already built a similar mine at Palito, so the "20 per cent contingency on both operating and capital costs" in the Oct PEA, is not to be sniffed at or easily dismissed.

At $20m build costs and debt options for at least half of it,

2F

if not more, SRB at c. $10m (my view) in the bank close of Q3 and only $8.5m of Coringa purchase price left to pay, have good options.

Even 10k oz at c. $1,850 gold, delivers (my view) over $5m to the SRB coffers per quarter.

SRB also still have $10m of a $12m convertable..

if not more, SRB at c. $10m (my view) in the bank close of Q3 and only $8.5m of Coringa purchase price left to pay, have good options.

Even 10k oz at c. $1,850 gold, delivers (my view) over $5m to the SRB coffers per quarter.

SRB also still have $10m of a $12m convertable..

2G

...loan from Greenstone, at 76p conversion.

So worst case scenario we are talking 71m shares in issue and Coringa on its was to being built.

But I don't see the need to employ all of it, especially when conversion is well below today's SP, be it appreciation may be in play.

...loan from Greenstone, at 76p conversion.

So worst case scenario we are talking 71m shares in issue and Coringa on its was to being built.

But I don't see the need to employ all of it, especially when conversion is well below today's SP, be it appreciation may be in play.

2H

Of course if SRB better that 10k oz or gold pushes above $1,850, then all of the above becomes much easier to solve.

Whatever the case, SRB has clear line of sight to min. 85k oz.

With additional cash resources, I would expect an ore sorter expansion at Coringa, just as...

Of course if SRB better that 10k oz or gold pushes above $1,850, then all of the above becomes much easier to solve.

Whatever the case, SRB has clear line of sight to min. 85k oz.

With additional cash resources, I would expect an ore sorter expansion at Coringa, just as...

2I

we saw play out at Palito, which added 8,000 oz to the mine, pushing us to c. 93k oz.

The play with SRB right now is getting the Palito mine back to full production and managing any Covid restrictions.

Achieve that and there's good run to much higher revenues,

we saw play out at Palito, which added 8,000 oz to the mine, pushing us to c. 93k oz.

The play with SRB right now is getting the Palito mine back to full production and managing any Covid restrictions.

Achieve that and there's good run to much higher revenues,

2J

at valuation levels, that haven't even taken into account Palito at full production yet because it is yet to be achieved/confirmed but it will come and I am more than happy to wait.

at valuation levels, that haven't even taken into account Palito at full production yet because it is yet to be achieved/confirmed but it will come and I am more than happy to wait.

• • •

Missing some Tweet in this thread? You can try to

force a refresh