1/8

Key takeaway from #AVCT Interims presentation and a point I have been focusing in on for a while.

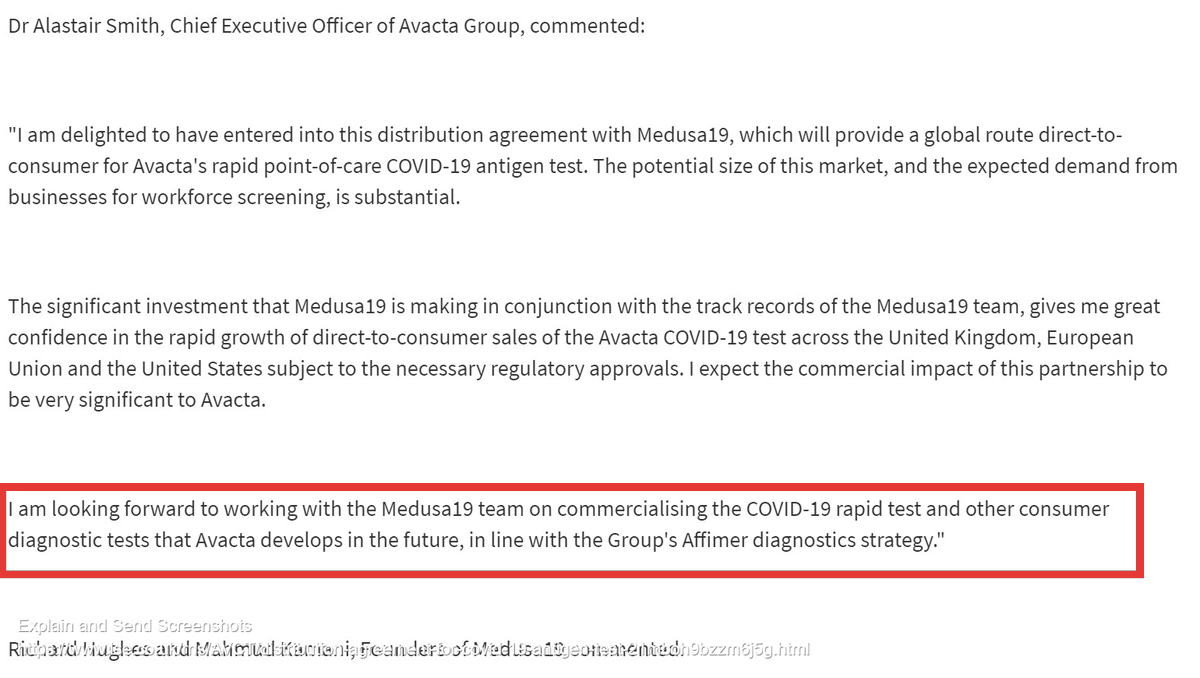

The enclosed slide delves more into "Avacta's Product Strategy."

Whilst home testing is of course an ultimate goal,

Key takeaway from #AVCT Interims presentation and a point I have been focusing in on for a while.

https://twitter.com/BigBiteNow/status/1294661796448665600?s=20

The enclosed slide delves more into "Avacta's Product Strategy."

Whilst home testing is of course an ultimate goal,

2/8

it is for me a complete bonus to the investment case. A free shot if you will and not necessary for the success of this test, to be truly enormous.

When discussing this slide Dr Smith says about professional use being ;

it is for me a complete bonus to the investment case. A free shot if you will and not necessary for the success of this test, to be truly enormous.

When discussing this slide Dr Smith says about professional use being ;

3/8

"far more likely to be professional use around workplace testing and that involves having a trained technician or healthcare worker on site, which many companies are planning to do."

Now ask yourself, how does AVCTs CEO know so many companies are planning to have...

"far more likely to be professional use around workplace testing and that involves having a trained technician or healthcare worker on site, which many companies are planning to do."

Now ask yourself, how does AVCTs CEO know so many companies are planning to have...

3/8

...healthcare personnel on site to conduct these tests?

Furthermore, what does that say about the necessity of focusing in on CONDOR and UK Gov orders?

Clinical validation for professional use, sits fully under the control of AVCT and their manufacturing partners

...healthcare personnel on site to conduct these tests?

Furthermore, what does that say about the necessity of focusing in on CONDOR and UK Gov orders?

Clinical validation for professional use, sits fully under the control of AVCT and their manufacturing partners

4/8

and is coming in Q4.

Remember, back on 20th May, Medusa agreed exclusive world roll out for the consumer test but only ;

"non-exclusive rights to supply the tests to businesses for workforce testing."

What that slide demonstrates is that the workforce testing market...

and is coming in Q4.

Remember, back on 20th May, Medusa agreed exclusive world roll out for the consumer test but only ;

"non-exclusive rights to supply the tests to businesses for workforce testing."

What that slide demonstrates is that the workforce testing market...

5/8

...is up first and AVCT have clearly known that for some time.

So much so that the BBI Solutions app is in play, so completely stand alone in terms of what Medusa are putting together.

However, simply writing off Medusa is for me a mistake. They can push further sales...

...is up first and AVCT have clearly known that for some time.

So much so that the BBI Solutions app is in play, so completely stand alone in terms of what Medusa are putting together.

However, simply writing off Medusa is for me a mistake. They can push further sales...

6/8

...to businesses and so it is another pipeline and entity, working to sell AVCT tests, which can never be a bad thing. In addition, they are clearly blooding their teeth with Covid tests and being set up for the next phase, post Covid.

See below.

...to businesses and so it is another pipeline and entity, working to sell AVCT tests, which can never be a bad thing. In addition, they are clearly blooding their teeth with Covid tests and being set up for the next phase, post Covid.

See below.

7/8

One question remains on where AVCT wants to go with this now?

Will they sell direct or will it be other parties?

But its not what's key right now.

Whats key is that a very large market is about to be opened up in Q4 and it won't be affected by UK Gov.

Unless of course,

One question remains on where AVCT wants to go with this now?

Will they sell direct or will it be other parties?

But its not what's key right now.

Whats key is that a very large market is about to be opened up in Q4 and it won't be affected by UK Gov.

Unless of course,

8/8

UK Gov has its very own FOMO and pushes the buy button earlier than it should.

They've form after all with tests that cannot do what AVCT is advertising they will.

All of which creates a wonderful arena of competition for AVCT and why more partners are clearly on the way.

UK Gov has its very own FOMO and pushes the buy button earlier than it should.

They've form after all with tests that cannot do what AVCT is advertising they will.

All of which creates a wonderful arena of competition for AVCT and why more partners are clearly on the way.

• • •

Missing some Tweet in this thread? You can try to

force a refresh