The pandemic is distorting euro area inflation data, but today's final HICP report provides another brutal reality check for the ECB - a thread with charts.

https://twitter.com/nghrbi/status/1317046632672788481

To add insult to injury, core inflation was revised even lower in September, from 0.24% to 0.22% YoY, its lowest level ever.

The main exogeneous drivers of the decline in core inflation are well-known (German VAT; summer sales in FR/IT) but excluding these, the trend continued to deteriorate. Every single metrics of underlying consumer prices declined in September, with no exception.

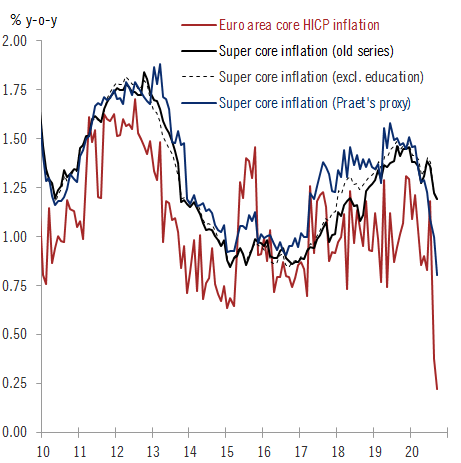

Super core inflation rates are falling, after having recovered for more than three years.

Momentum and trimmed inflation measures are collapsing.

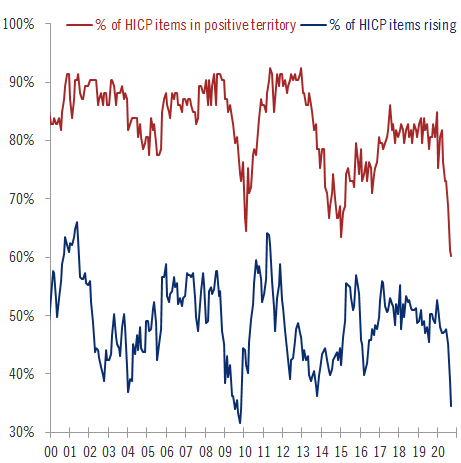

The share of HICP goods and services in positive territory has collapsed to an all-time low of 60%.

In the end, the deterioration in the inflation outlook requires further stimulus. And that was the case before the resurgence in Covid-19 cases.

ECB's Panetta: "the risks of a policy overreaction are much smaller than the risks of policy being too slow or too shy".

ECB's Panetta: "the risks of a policy overreaction are much smaller than the risks of policy being too slow or too shy".

• • •

Missing some Tweet in this thread? You can try to

force a refresh