1/ This Howard Marks memo describes why I am a "Charlie Munger investor" and why the term "value investor" is dead for me. oaktreecapital.com/insights/howar…

"There is no such thing as value and growth investing.” Buffett

"Dividing it up into 'value' and 'growth' is twaddle." Munger

"There is no such thing as value and growth investing.” Buffett

"Dividing it up into 'value' and 'growth' is twaddle." Munger

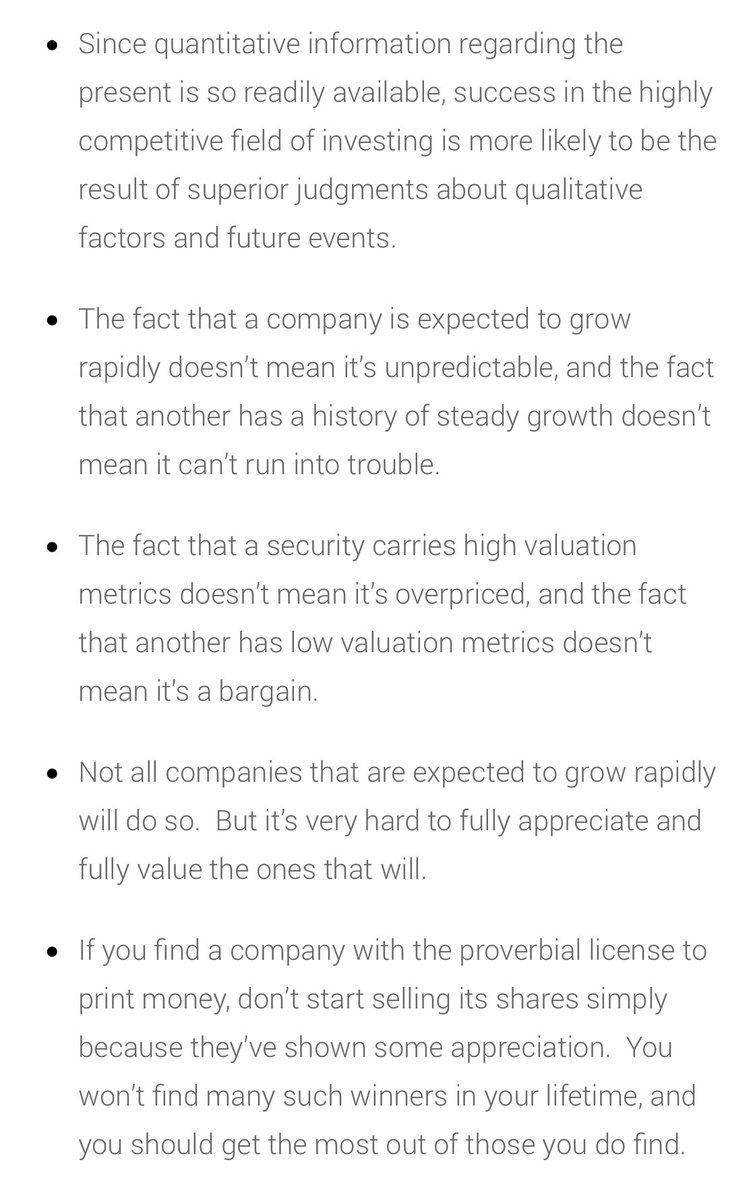

2/ "Value can be found in many forms. The fact that a company grows rapidly, relies on intangibles such as technology for its success and/or has a high p/e ratio shouldn’t mean it can’t be invested in on the basis of intrinsic value." Howard Marks

3/ If a genie asked me what meeting I would have liked to attended as a fly on the table, very high on the list would be one of the breakfasts where Charlie Munger and Howard Marks exchanged ideas. Here's some of the memo I cited in the first tweet:

4/ "Discounted cash proceeds is the appropriate way to value any business." Warren Buffett

See:

“Our main finding is direct cash flow measures are generally better stock return predictors than...various income statement profitability measures." economics.uwo.ca/50_anniversary…

See:

“Our main finding is direct cash flow measures are generally better stock return predictors than...various income statement profitability measures." economics.uwo.ca/50_anniversary…

5. "As John Malone famously said, if your long-term growth rate exceeds your cost of capital, your present value is infinite. However, this is only true for truly special companies, which are few and far between...." Howard Marks in his most recent memo cited above.

• • •

Missing some Tweet in this thread? You can try to

force a refresh