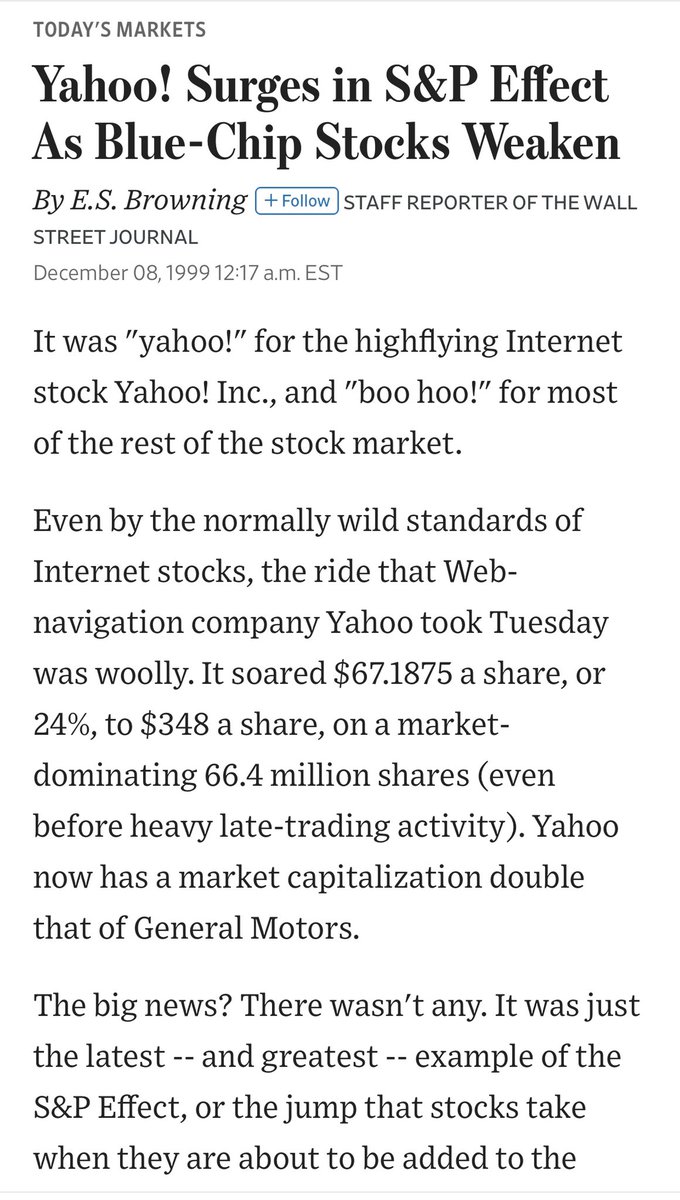

The guy I used to work with (I’ll call him “Q”) who shorted $TSLA at $600 in Dec called me today:

Q: Why is $TSLA up 6% on no news?

GB: Because it was down 8% yesterday on no news - unless you call a 10 bp rise in treasury yields and $BTC collapsing news. You still short?

Q: Why is $TSLA up 6% on no news?

GB: Because it was down 8% yesterday on no news - unless you call a 10 bp rise in treasury yields and $BTC collapsing news. You still short?

https://twitter.com/garyblack00/status/1343576316436762624

2/ Q: Of course I’m still short. It’s up another 30% since we talked two weeks ago. It’s all mo’.

GB: $TSLA MIC Y has a 4 mo wait. It’s entering India. Analysts are playing leapfrog raising PTs. Active mgrs have to own it or get fired. It’s cheap at 80x 2022 EPS vs 55% growth.

GB: $TSLA MIC Y has a 4 mo wait. It’s entering India. Analysts are playing leapfrog raising PTs. Active mgrs have to own it or get fired. It’s cheap at 80x 2022 EPS vs 55% growth.

3/ Q: Your earnings estimates are like twice consensus.

GB: The Street’s been wrong on $TSLA forever. Why do you listen to them? You really shouldn’t be short going into Biden’s inaugural speech and the FY’21 volume guide at the end of Jan. You’re going to get run over.

GB: The Street’s been wrong on $TSLA forever. Why do you listen to them? You really shouldn’t be short going into Biden’s inaugural speech and the FY’21 volume guide at the end of Jan. You’re going to get run over.

4/ Q: Whatever.

GB: Did you rent a Tesla for a week like I told you?

Q: No. You know I don’t drive.

GB: Did you build a $TSLA 5-yr volume, earnings, cash flow model?

Q: No. No one can forecast out 5 years.

GB: Did you talk to any Audi or BMW dealers? Or Tesla owners?

GB: Did you rent a Tesla for a week like I told you?

Q: No. You know I don’t drive.

GB: Did you build a $TSLA 5-yr volume, earnings, cash flow model?

Q: No. No one can forecast out 5 years.

GB: Did you talk to any Audi or BMW dealers? Or Tesla owners?

5/ Q: I don’t have time for that.

GB: Q, you haven’t done any real research. $TSLA ‘s up 40% since you shorted it. Maybe you should figure out why it keeps going up.

Q: It keeps going up because people like you are pumping it.

GB: You’re giving people like me too much credit.

GB: Q, you haven’t done any real research. $TSLA ‘s up 40% since you shorted it. Maybe you should figure out why it keeps going up.

Q: It keeps going up because people like you are pumping it.

GB: You’re giving people like me too much credit.

6/ Q: How can you even own $TSLA? It’s trading at more than all the other auto companies combined.

GB: You’re using the wrong metric. TSLA’s future competitors are $AAPL, $GOOG, $AMZN, $BIDU, plus Rivian, Lucid and new SPACs launching dedicated EVs. The legacy guys are dead.

GB: You’re using the wrong metric. TSLA’s future competitors are $AAPL, $GOOG, $AMZN, $BIDU, plus Rivian, Lucid and new SPACs launching dedicated EVs. The legacy guys are dead.

7/ Q: CNBC says $TSLA ‘a getting killed in Europe by the legacy mfrs’ new EV launches.

GB: CNBC is looking backward at 2020, when Tesla’s plant was shut for 7 weeks, and capacity was re-purposed to produce Y CUVs, which more than doubled TSLA’s TAM, but none got to Europe.

GB: CNBC is looking backward at 2020, when Tesla’s plant was shut for 7 weeks, and capacity was re-purposed to produce Y CUVs, which more than doubled TSLA’s TAM, but none got to Europe.

8/ Q: I still don’t see how you can buy a stock trading at 220x next year’s earnings. $TSLA is a friggin car company.

GB: And $AAPL was a cellphone company that destroyed Blackberry, Nokia, and Motorola. $AMZN was a online bookseller that destroyed the entire retail industry.

GB: And $AAPL was a cellphone company that destroyed Blackberry, Nokia, and Motorola. $AMZN was a online bookseller that destroyed the entire retail industry.

9/ Q: You used to be a smart guy.

GB: I’m not the one down 40% on one stock in 2 weeks.

Q: Well I’m not closing my short. A lot of smart people are short $TSLA.

GB: Like you, they’re value investors who know nothing about growth stocks. It’s a whole different world.

GB: I’m not the one down 40% on one stock in 2 weeks.

Q: Well I’m not closing my short. A lot of smart people are short $TSLA.

GB: Like you, they’re value investors who know nothing about growth stocks. It’s a whole different world.

• • •

Missing some Tweet in this thread? You can try to

force a refresh