Today’s GDP release, and in particular how the economy has adapted, a thread.👇

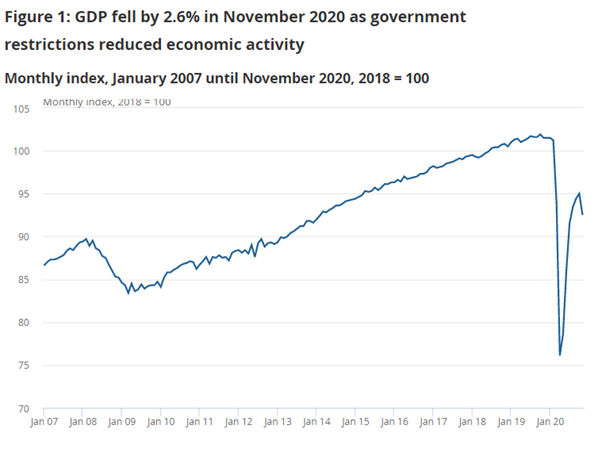

After 6 months of growth, the economy started shrinking again in November as tighter restrictions were in place. (Though there were variations across Wales, England, Scotland and Northern Ireland.) (1/n)

The economy shrank by 2.6% in November. In normal times this would be a significant downturn, but it is much smaller than the falls seen with the first restrictions in the spring: April GDP fell by around 20%. In that sense it is good news. But why the smaller fall? (2/n)

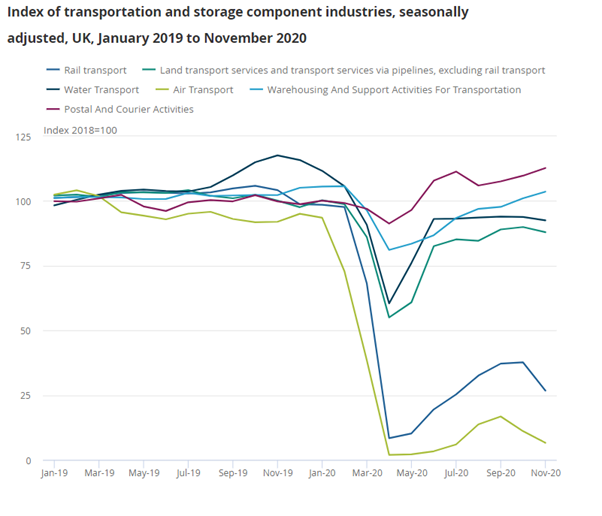

Firstly, some industries remain very depressed. Airlines (air transport in the chart) for example, were operating at very low levels in October so there wasn’t much further for their output to fall. This is different from the picture in Mar/Apr. (3/n)

The same is true, though perhaps less pronounced, for bars/restaurants and other parts of the service sector. (4/n)

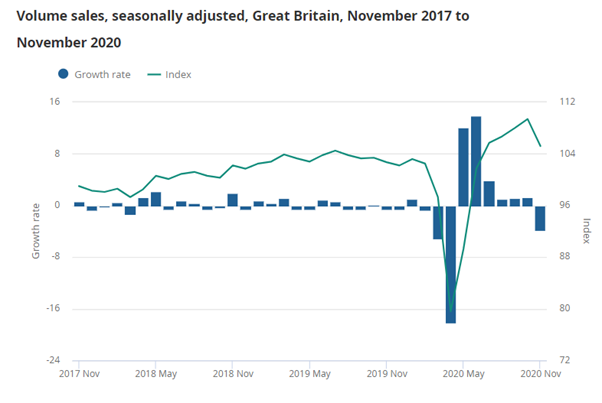

Secondly, some sections of the economy have undergone a structural shift that has allowed them to continue to meet demand/produce output. Perhaps the best example is in retail. Overall sales in November were higher than pre-pandemic despite the restrictions. (5/n)

This is due, in part, to the shift online, which allowed sales to continue when shops were shut. These structural shifts create winners (on-line retailers) and losers (high-street), so a positive overall story can hide some significant distress for some businesses. (6/n)

There are also knock-on effects of this move on-line, with courier/postal services seeing growth through the pandemic. (7/n)

And there have been wider changes: food retailers have gained at the expenses of restaurants, and home improvement shops have benefited as consumers appeared to shift expenditure from other activities such as holidays and travel. (8/n)

Whether these changes are permanent or temporary, we will have to wait to see. (9/n)

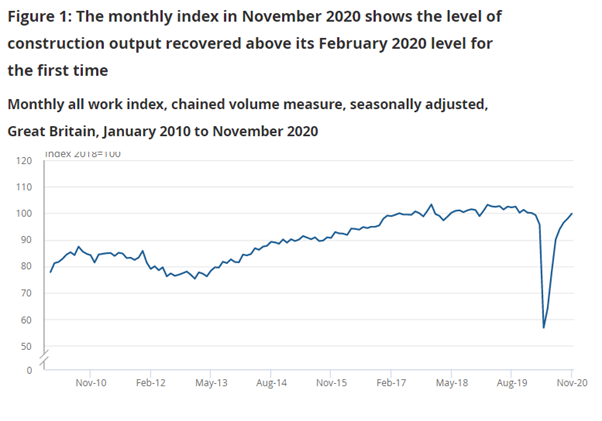

Thirdly, individual industries (and businesses) have become more resilient to the restrictions. We saw big falls in construction during the first set of national restrictions, but continued growth during the November restrictions. (10/n)

This is likely due to social distancing in workplaces, etc. that have allowed operations to continue. (11/n)

Overall, the economic impacts are smaller this time. But we should not lose sight of the fact that the economy has still taken a large hit from the pandemic, and beneath the surface there are hugely different experiences for different sectors, businesses and people. (ENDS)

• • •

Missing some Tweet in this thread? You can try to

force a refresh