A Little GameStop/Robinhood Perspective: A number of hedge funds got the $GME trade very wrong on a risk/reward basis(I know the feeling), and attracted the interest of smart retail investors. They spread the word via social media, and the stock skyrocketed.

(2) The affected hedge funds were run over, but few noticed that other big hedge funds made as much, or more, than the retail investors. Ok, some lost big, some won big. Happens all the time. Then things got weird...

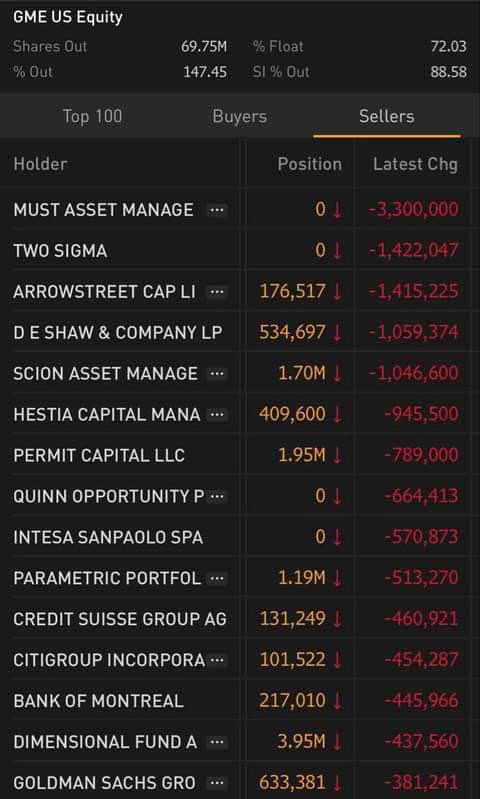

(3) As the stock went higher and higher, retail investors began to believe that the hedge funds that were short could never cover because the short interest was 140% of the shares outstanding. Yet the stock was trading more than 100% of its shares outstanding EVERY DAY.

(4) As this story circulated, $GME stock went parabolic and other stocks with high short interest also went up in sympathy. But so many retail investors began to buy these stocks on margin, that the online brokers began having regulatory/clearinghouse capital issues today.

(5) These brokerages(but not others) began to restrict trading in the volatile stocks per their customer agreements, so as to not violate their regulatory capital limits...and all hell broke loose.

(6) Retail traders were outraged that they were not allowed to buy more of a stock that was up 20X over the past three months. That somehow the Wall St “Elites” were preventing them from profiting even more, so as to protect hedge funds(many of whom were long) and short-sellers.

(7) And as a result, politicians joined the fray, decrying the regulatory system(!) that they would normally defend, so as to curry favor with the aggrieved investor class that had already made a killing in a very smart trade.

(8) A regulatory system that did exactly what it should have done, for a set of undercapitalized brokerages, so as to prevent their collapse(we’ll see what happens) in an extreme set of market circumstances.

(9) So just what is all the outrage about? The shorts/HF’s lost, retail (and HF’s!) won, and we all learned about the risks of the no cost online brokerage model. But I am hard-pressed to see why making a lot of $ in a heavily-shorted set of stocks is a national crisis.

• • •

Missing some Tweet in this thread? You can try to

force a refresh