#ncyt #alnov #novacyt

SP Angel published a New note on #ncyt

You Can Access the full document here :

novacyt.com/wp-content/upl…

The target Price is 1433p, but there are many interesting things in this document.

Thread ⤵️

1/15

SP Angel published a New note on #ncyt

You Can Access the full document here :

novacyt.com/wp-content/upl…

The target Price is 1433p, but there are many interesting things in this document.

Thread ⤵️

1/15

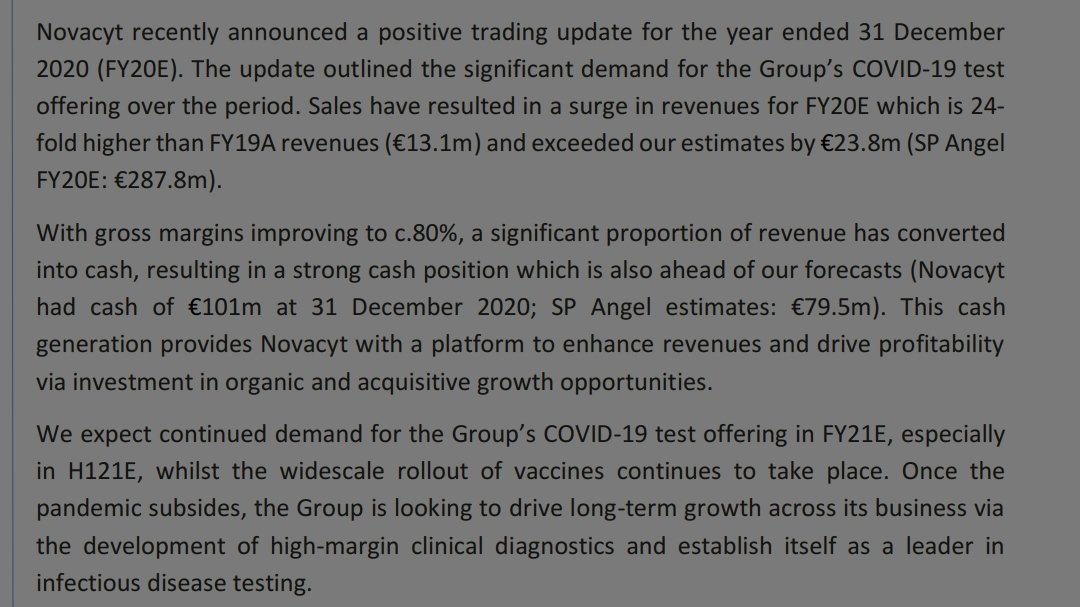

First, the FY2020 results are better than in the last forecast.

Actual vs previous forecast

Revenue 311m vs 287m

Cash 101m vs 79m

The cash accumulated will allow them to develop themselves into a "high margin clinical diagnostics" sector.

2/n

Actual vs previous forecast

Revenue 311m vs 287m

Cash 101m vs 79m

The cash accumulated will allow them to develop themselves into a "high margin clinical diagnostics" sector.

2/n

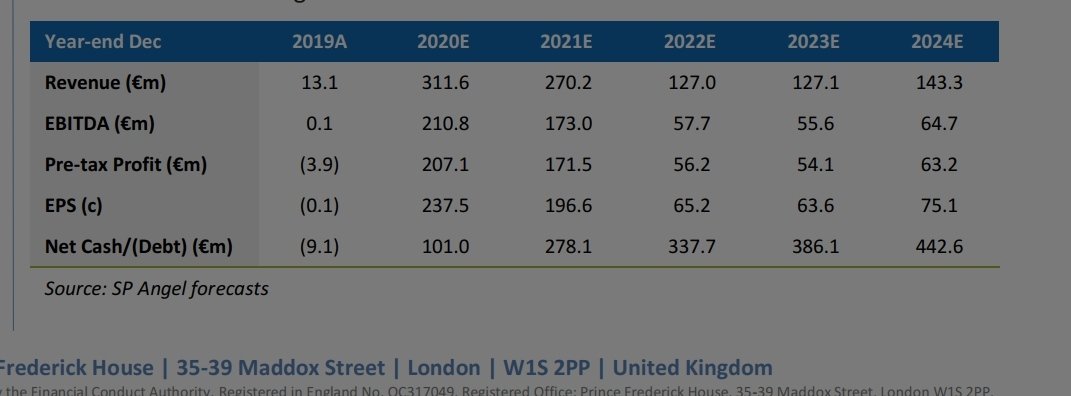

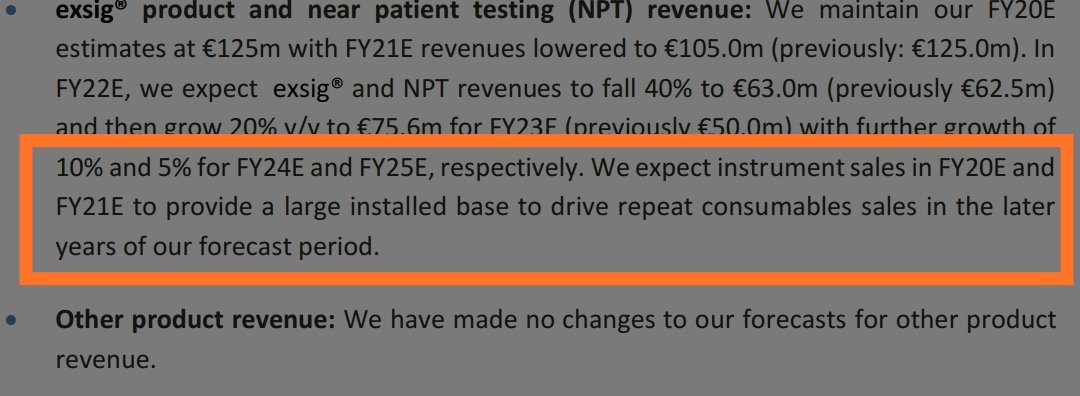

Revenues and forecast.

Things are really important here.

We Can see the revenues decrease until 2023 on this forecast.

But look at the cash accumulation. This will not sit in the bank and wait !

So, when they use this cash for aquisitions for ex.,

3/n

Things are really important here.

We Can see the revenues decrease until 2023 on this forecast.

But look at the cash accumulation. This will not sit in the bank and wait !

So, when they use this cash for aquisitions for ex.,

3/n

This note will be updated again, and the revenues will be modified.

This forecast is based on "now", so each new contract, like phase 2 for ex., Will change this forecast dramaticly too !

So, when aquisition or new contracts come, the revenue forecast will increase.

4/n

This forecast is based on "now", so each new contract, like phase 2 for ex., Will change this forecast dramaticly too !

So, when aquisition or new contracts come, the revenue forecast will increase.

4/n

They also suppose in this note that covid revenue will decrease once the pandemic subsides.

But when ? Imo, noone knows for sure.

New variants are appearing, and there might be immunity problems with vaccines. To Guess when the covid revenue will decrease is hard to tell...

5/n

But when ? Imo, noone knows for sure.

New variants are appearing, and there might be immunity problems with vaccines. To Guess when the covid revenue will decrease is hard to tell...

5/n

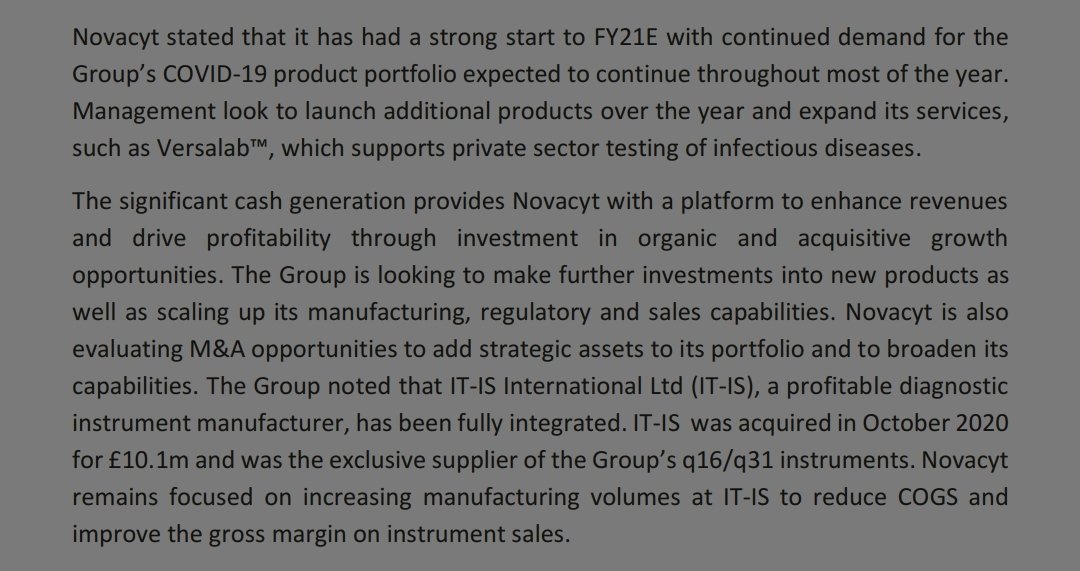

But, 2021 has started with a strong demand, and this should last most of the year. (Conservative thought imo)

-New products to be launched

-Versalab expanding, note they use infectious diseases in general.

6/n

-New products to be launched

-Versalab expanding, note they use infectious diseases in general.

6/n

Investments :

- New products

- scaling up manufacturing (also it-is)

- "..." Regulatory and sales capabilities

- M&A

All this Can change this evaluation, especially M&A, which could allow a better view in future revenues, post-covid.

7/n

- New products

- scaling up manufacturing (also it-is)

- "..." Regulatory and sales capabilities

- M&A

All this Can change this evaluation, especially M&A, which could allow a better view in future revenues, post-covid.

7/n

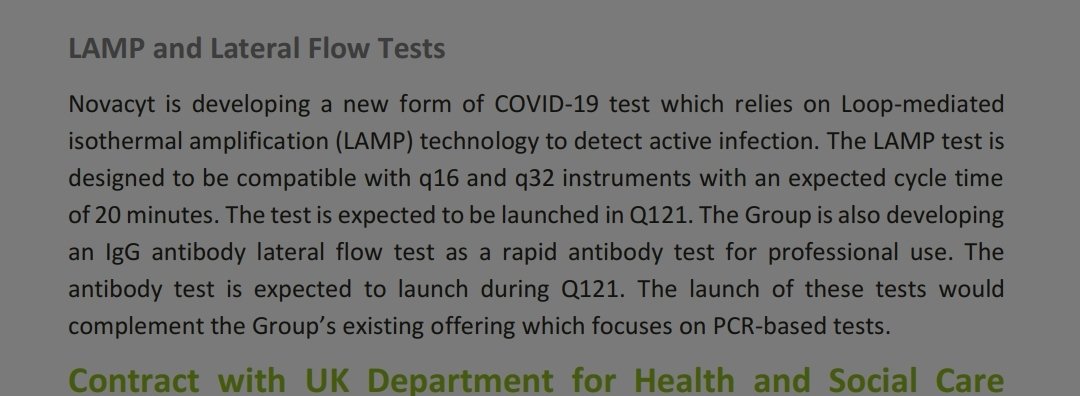

Dont forget the New products to be launched during Q1, soon !

- LFT antibody test

- rt-lamp

Remember Jacks shooting about an LFT ?

If like PROmate, when the product is launched, it will certainly have been through all the UK validations, and be ready for sales and tenders.

8/n

- LFT antibody test

- rt-lamp

Remember Jacks shooting about an LFT ?

If like PROmate, when the product is launched, it will certainly have been through all the UK validations, and be ready for sales and tenders.

8/n

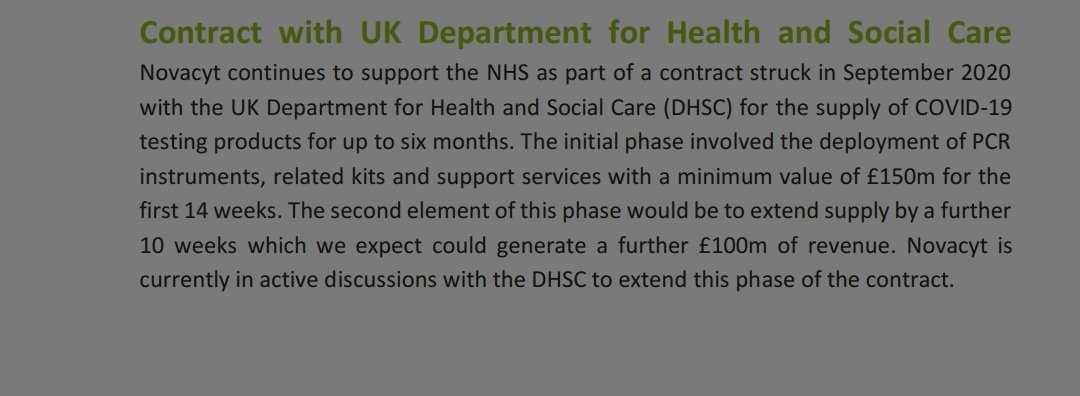

About PROmate.

We know the "marshmallow" is now used with PROmate in the NHS.

And Ncyt is in "active discussions" with DHSC.

An update about this contract could land anytime now imo....

(And could therefore change the revenue forecast 😉)

9/n

We know the "marshmallow" is now used with PROmate in the NHS.

And Ncyt is in "active discussions" with DHSC.

An update about this contract could land anytime now imo....

(And could therefore change the revenue forecast 😉)

9/n

We know GM is developping the company - done very well for now - on results, products and growth. Not on hype.

The goal here is to create during covid a Real and strong basis for the company, with New customers around the world (many of prestige, like WHO, CDC,etc)

10/n

The goal here is to create during covid a Real and strong basis for the company, with New customers around the world (many of prestige, like WHO, CDC,etc)

10/n

With the aquisition of it-is, he created a fully integrated company.

Having all covid products working efficiently with the it-is instruments allow them to create a "large installed base".

Very important to help them sell their non covid products.

11/n

Having all covid products working efficiently with the it-is instruments allow them to create a "large installed base".

Very important to help them sell their non covid products.

11/n

Imo, in a world Where the diagnostic of diseases will have a a big place, as some general forecast on diagnostic growth are showing.

Versalab is the beginning of something big. Partnerships around the world, using the Qs and ncyts pcr portfolio...

12/n

Versalab is the beginning of something big. Partnerships around the world, using the Qs and ncyts pcr portfolio...

12/n

This is not just for covid, it is for the Years to Come.

For PROmate, same. The first PROmate assay is for covid.

But they Can and will develop this for all kind of infectious diseases. AIDS, Ebola, even flu...

13/n

For PROmate, same. The first PROmate assay is for covid.

But they Can and will develop this for all kind of infectious diseases. AIDS, Ebola, even flu...

13/n

This is really a game changer in the pcr market of infectious diseases. Desactivate the virus for testing will facilitate many things.

14/n

14/n

So, important from this note is that SP Angel will have to update it with New contracts, M&A...

It is a good basis to see that revenues will continue even when covid ends

GM has a plan for Ncyt and its future

If you had confidence during 2020, imo no reason to doubt now !

15/15

It is a good basis to see that revenues will continue even when covid ends

GM has a plan for Ncyt and its future

If you had confidence during 2020, imo no reason to doubt now !

15/15

• • •

Missing some Tweet in this thread? You can try to

force a refresh