In our latest video, @JasonMutiny and I explore the reflation trade.

- What is it?

- Where does the evidence stand?

- What trades might you consider in your portfolio?

Stuffed with graphs from JPM, GS, Nomura, and SocGen.

- What is it?

- Where does the evidence stand?

- What trades might you consider in your portfolio?

Stuffed with graphs from JPM, GS, Nomura, and SocGen.

https://twitter.com/FinancePirates/status/1370515626100469761

@JasonMutiny A few graphs and charts you’ll see:

Consumers have a lot of savings and are feeling pretty wealthy right now...

Consumers have a lot of savings and are feeling pretty wealthy right now...

@JasonMutiny Real goods spending has recovered, but services not so much.

So is the consumer WILLING to spend, they’re just not being allowed to?

So is the consumer WILLING to spend, they’re just not being allowed to?

@JasonMutiny We’re seeing equities pricing in reopening, but mostly in the US.

@JasonMutiny There’s lots of calls for further steepening, but in the short-term, futures suggest that lots of institutions are already priced for it.

(Did CTAs exaccerbate recent sell-offs?)

(Did CTAs exaccerbate recent sell-offs?)

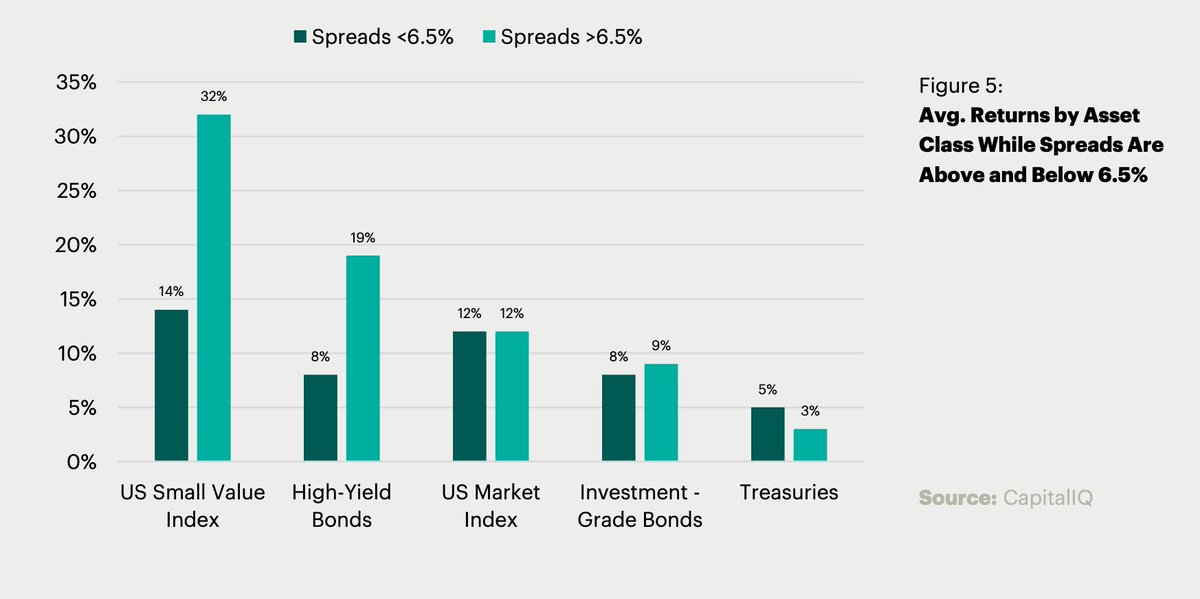

@JasonMutiny Historically speaking, certain sectors tend to do well during a steepening cycle, and we’re already seeing flow disparity in ETFs (top = XLE + XLF + XLY, bottom = XLK + XLV + XLP)

@JasonMutiny Re-opening baskets correlate highly with small-cap and value tilts right now.

Interestingly, we’d expect momentum to start tilting into these names in the next few months as well.

Interestingly, we’d expect momentum to start tilting into these names in the next few months as well.

@JasonMutiny Finally, JPM and SocGen are both calling for a commodity SUPERCYCLE.

Spot commodities, equity sectors (e.g. Energy, which is massively under-allocated), or CTAs may be different ways to play this thesis.

Spot commodities, equity sectors (e.g. Energy, which is massively under-allocated), or CTAs may be different ways to play this thesis.

@JasonMutiny For more, please watch the video!

And give us your feedback!

And, if you like what you see, hit that “like” button and subscribe.

And give us your feedback!

And, if you like what you see, hit that “like” button and subscribe.

• • •

Missing some Tweet in this thread? You can try to

force a refresh