This thread reports ongoing India vaccination data, explains 2nd dose crowding effect and May open eligibility projections.

First: Ongoing rate of vaccinations , with both first and second doses considered:

1/

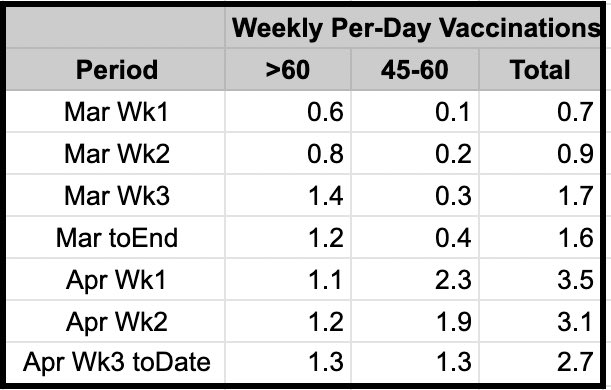

First: Ongoing rate of vaccinations , with both first and second doses considered:

1/

Observations:

1. >60 group consistently ~1.1 to 1.3m per day since mid March

2. 45-60 group did 2.3/day in wk 1 of April, but dropped to 1.3m by wk 3

Unclear why 45-60 group less enthusiastic despite >60 group consistent wk to wk .

2/

1. >60 group consistently ~1.1 to 1.3m per day since mid March

2. 45-60 group did 2.3/day in wk 1 of April, but dropped to 1.3m by wk 3

Unclear why 45-60 group less enthusiastic despite >60 group consistent wk to wk .

2/

Observations 2

1. Navratri since Apr 13

2. 2nd wave may be lowering turnout.

Since >60 is highest risk group, consistency in that group has highest impact on keeping mortality risk down.

3/

1. Navratri since Apr 13

2. 2nd wave may be lowering turnout.

Since >60 is highest risk group, consistency in that group has highest impact on keeping mortality risk down.

3/

Fig 2

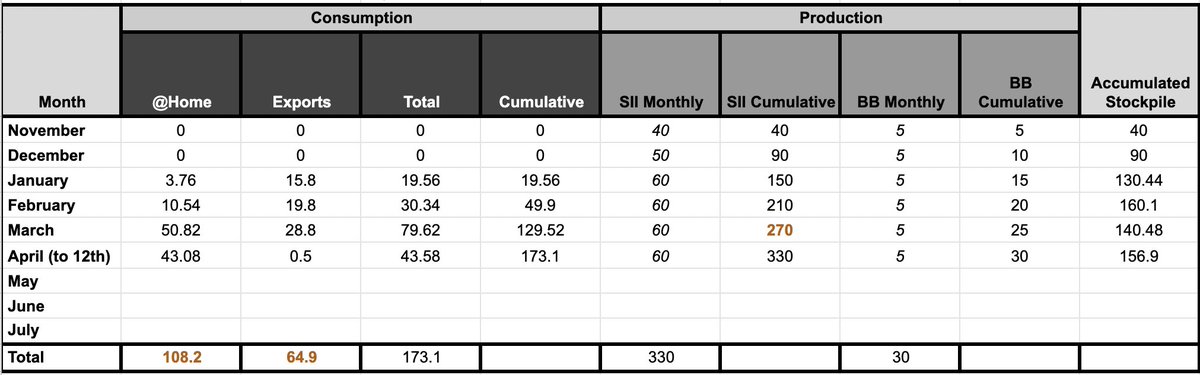

This data shows the impact of 2nd dose demand , which results in a ‘crowding out’ behavior using up daily doses and preventing people from getting first doses. People think this is ‘shortage’ but it is really a 1st dose crowding out:

4/

This data shows the impact of 2nd dose demand , which results in a ‘crowding out’ behavior using up daily doses and preventing people from getting first doses. People think this is ‘shortage’ but it is really a 1st dose crowding out:

4/

Fig 2 Explained:

1. Assume 5m dose/month Covaxin spread over 4 weeks.

2. Compute Covishield 2nd dose demand from 6wk prior first dose, and taking out Covaxin 2nd doses from 4 weeks after 1st dose.

Caveat: imprecise/simplified but just for modeling purposes.

5/

1. Assume 5m dose/month Covaxin spread over 4 weeks.

2. Compute Covishield 2nd dose demand from 6wk prior first dose, and taking out Covaxin 2nd doses from 4 weeks after 1st dose.

Caveat: imprecise/simplified but just for modeling purposes.

5/

Observations:

1. Very interesting accordion behavior: only first doses early on = many 2nd doses reqd in mid May

2. This peak 2nd dose falls later in May because by mid April more and more daily doses are second doses.

6/

1. Very interesting accordion behavior: only first doses early on = many 2nd doses reqd in mid May

2. This peak 2nd dose falls later in May because by mid April more and more daily doses are second doses.

6/

Observations Contd

1. This means fewer 1st doses now and fewer 2nd doses needed in 6 weeks…

2. This is very likely why Sputnik is being imported in May - there’s a period where March/April ramp up turns to 2nd dose demand in May.

7/

1. This means fewer 1st doses now and fewer 2nd doses needed in 6 weeks…

2. This is very likely why Sputnik is being imported in May - there’s a period where March/April ramp up turns to 2nd dose demand in May.

7/

Fig 3

Let us look at weekly 2nd dose requirement and impact

This figure takes the previously computed 2nd dose reqd in May, then tries to figure out how many first doses can be done in May.

8/

Let us look at weekly 2nd dose requirement and impact

This figure takes the previously computed 2nd dose reqd in May, then tries to figure out how many first doses can be done in May.

8/

For simplicity I assume weekly availability of 26m doses (approx current).

In second week of May, ~80% of daily doses are 2nd doses. By 3rd week it drops to 51% and then 37%, due to previously described accordion effect.

9/

In second week of May, ~80% of daily doses are 2nd doses. By 3rd week it drops to 51% and then 37%, due to previously described accordion effect.

9/

Currently approx 2m doses/day are being consumed as 1st doses, split between >60 and 45-60 groups. In May the 18+ group becomes eligible. This places a demand for first doses.

Govt has already acted to fix the mid May 2nd dose peak demand by ordering Sputnik import.

10/

Govt has already acted to fix the mid May 2nd dose peak demand by ordering Sputnik import.

10/

However, in order to support ~2m/day first doses of high risk group and adequate numbers of 18+ group, the government will quickly need at least 4-4.5m doses/day in May, translating to ~120m doses that month.

11/

11/

Given that the turnout of the >45 high risk group has been stable (ignoring the variability of the 45-60 group) a potential option to make vaccines fairly available to 18+ group is to use a lottery system for them.

12/

12/

Late May is when first and second dose consumption reaches a degree of equilibrium . In order to satisfy the high 2nd dose requirement to mid May and avoid crowding out first doses of high risk group, govt needs more supply AND rate control.

13/

13/

Rate control is only for the 18-44 group to keep them from reducing the ongoing stable first dose rate of the >45 group, who currently consume 2m first doses/day, probably falling to 1.5m/day in May since >50% of them will have at least one dose then.

14/

14/

Rate control can be implemented by setting aside the known stable consumption by >45 group and setting up a lottery registration on CoWin site for 18-44 group. Winners each day go get vaccinated next day, perhaps.

15/

15/

Summary

1. The high ramp up in end March/early April will cause a high 2nd dose demand in mid May

2. Govt urgently importing Sputnik end April is most likely to handle this crunch period.

3. By 2nd half of may 1st/2nd dose equilibrium enables better planning of doses.

16/

1. The high ramp up in end March/early April will cause a high 2nd dose demand in mid May

2. Govt urgently importing Sputnik end April is most likely to handle this crunch period.

3. By 2nd half of may 1st/2nd dose equilibrium enables better planning of doses.

16/

Overall govts actions here are predictable by looking closely at data. Sputnik import aligned to high May 2nd dose need indicates they are also doing projections. This is a good sign that there is a planned data-driven approach being used.

17/

17/

States will have to make a choice whether to keep vaccinating >45 or let 18-44 group have more share.

Former group are more at risk of death, but latter group are a higher transmission risk. States will have to sensibly split doses between the two.

18/18

Former group are more at risk of death, but latter group are a higher transmission risk. States will have to sensibly split doses between the two.

18/18

• • •

Missing some Tweet in this thread? You can try to

force a refresh