Tradfi markets may not have realised it yet, but we're living through a generational change in credit markets.

Let's look at what's happening and how Mars protocol will radically accelerate the change...

👇

Let's look at what's happening and how Mars protocol will radically accelerate the change...

👇

In the old world financial system, interest rates on loans and deposits are determined by two 🔑 factors:

1. The term (or duration) of a loan.

2. The rates set by central banks (which lend money at those rates to commercial banks).

1. The term (or duration) of a loan.

2. The rates set by central banks (which lend money at those rates to commercial banks).

Rates on credit protocols like $AAVE and soon $MARS are driven by different rules.

The way most prominent DeFi protocols work is automated and transparent.

They're rarely subject to terms or fixed durations, and that makes them more flexible.

The way most prominent DeFi protocols work is automated and transparent.

They're rarely subject to terms or fixed durations, and that makes them more flexible.

You can borrow $10 (or $10 million) without committing to a hard date for repayment.

Central banks have little impact on credit protocol rates.

Instead, interest rates on crypto loans are driven by liquidity and market demand.

Central banks have little impact on credit protocol rates.

Instead, interest rates on crypto loans are driven by liquidity and market demand.

If there's a lot of borrowing demand for a given token, rates rise. The opposite is also true (low demand = low rates).

So how do credit protocols set their rates?

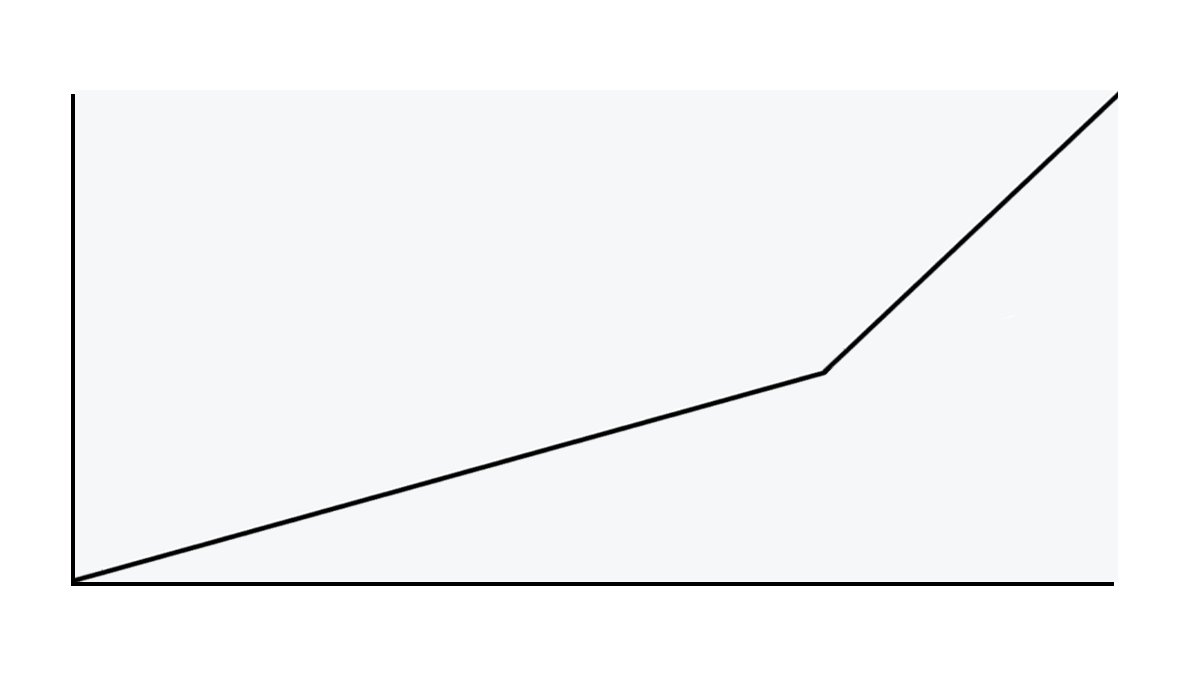

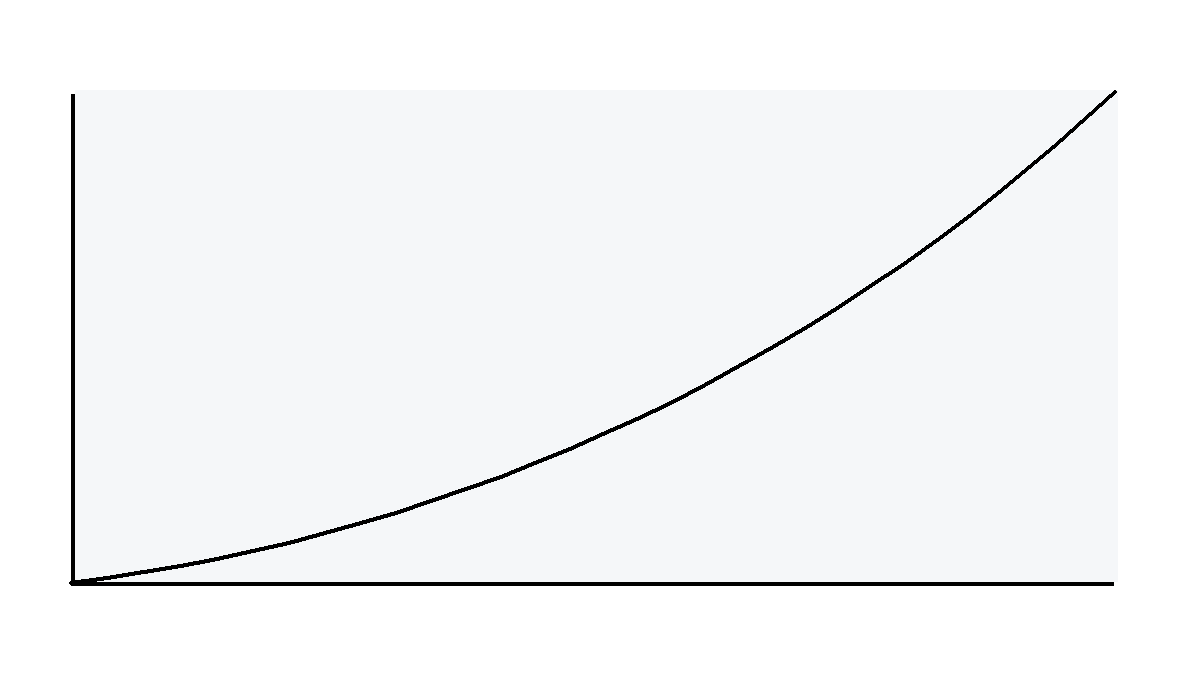

To date, most protocols have taken a very straightforward approach. They fall into three broad groups:

1. Linear rates. Rates increase based on demand.

To date, most protocols have taken a very straightforward approach. They fall into three broad groups:

1. Linear rates. Rates increase based on demand.

2. Linear with a kink. Rates follow 2 slopes: a lower slope before an optimal utilisation level and a steeper slope after that level. The kink is created by the difference between the 2 slopes.

3. Non-linear. The rate is curved into a nice-looking slope.

While these approaches have proven successful to date, there are enormous opportunities for improvement.

See, all three interest rate models share a problem: they can't adapt to real-time changes in market conditions.

See, all three interest rate models share a problem: they can't adapt to real-time changes in market conditions.

That's why some assets on today's leading credit protocols are frequently over-utilised... meaning that they've lent more than they want to.

When that happens, users who want to withdraw their deposits may be unable to do so.

When that happens, users who want to withdraw their deposits may be unable to do so.

$MARS will be different.

We will be the first credit protocol in the world to feature dynamic interest rates. Rates will not be defined by a pre-determined curve but will rather evolve in real-time based on market conditions.

We will be the first credit protocol in the world to feature dynamic interest rates. Rates will not be defined by a pre-determined curve but will rather evolve in real-time based on market conditions.

Our adaptive rates will be handled by a "PID Controller" or proportional-integral-derivative controller.

It's a terrible name (we know), but it's a common mathematical concept used in lots of places outside of finance.

It's a terrible name (we know), but it's a common mathematical concept used in lots of places outside of finance.

The classic example of a PID Controller is the cruise control on a car. Maintaining a fixed speed is simple on a flat surface. But as soon as you hit a hill, the car's computer must adapt to changes in gravity.

That means the car must apply more gas when going uphill and decelerate when going downhill. Enter the continually-running mathematical formulas of the PID Controller.

$MARS' dynamic interest rates will operate similarly. Thanks to an integrated PID Controller, we'll adjust rates based on changes in supply and demand to target an optimal utilisation level.

On a per-block basis, rates will be re-calculated using this formula.

On a per-block basis, rates will be re-calculated using this formula.

Rates will also be looked at holistically.

For example, if one market is underutilised, we will decrease interest rates to boost demand within that market and vice versa when the market is over-utilised.

For example, if one market is underutilised, we will decrease interest rates to boost demand within that market and vice versa when the market is over-utilised.

You can dive extraordinarily deep into our dynamic interest rate model here.

mars-protocol.medium.com/exploring-mars…

mars-protocol.medium.com/exploring-mars…

But right now, we're thinking big picture. What does all this mean on a macro level?

First, the success of existing credit protocols shows there's a whole new credit ecosystem that's developing in parallel to the old world financial system.

First, the success of existing credit protocols shows there's a whole new credit ecosystem that's developing in parallel to the old world financial system.

Power is quietly shifting from the old world financial system to the new. This will only accelerate as blockchains become truly cross-chain and assets like $LUNA, $BTC, $ETH, and $MARS siphon off some of the value-storing characteristics of fiat.

We envision a future where literally ALL credit-based transactions shift from centralised, old world systems to decentralised, fully-automated protocols.

Today's protocols hold billions of dollars in value. Soon they will hold trillions.

Today's protocols hold billions of dollars in value. Soon they will hold trillions.

Two years ago, such a statement might have sounded ludicrous.

Today, it feels inevitable, and we believe it will happen much faster than the old world participants realise.

Today, it feels inevitable, and we believe it will happen much faster than the old world participants realise.

When Mars launches, it will first feature the proportional (p) term... the "P" in "PID Controller" to efficiently allocate resources within the protocol.

As we gauge the impact with real-world usage, we'll launch the Integral and Derivative terms.

As we gauge the impact with real-world usage, we'll launch the Integral and Derivative terms.

All this will give Mars a fully dynamic interest rate model that's never been used before within credit protocols.

It will adjust to market conditions in real time, and in the process it will maximise rewards for lenders, borrowers and stakers (who earn a cut of protocol fees).

It will adjust to market conditions in real time, and in the process it will maximise rewards for lenders, borrowers and stakers (who earn a cut of protocol fees).

Mars will quite literally adapt to credit conditions like the cruise control on your sedan.

We're approaching finance at the speed of light.

We're approaching finance at the speed of light.

Mars' dynamic interest rate model will drive new efficiencies that will supercharge adoption.

We recognise "PID Controller" may be one of the worst-sounding names in history... but it doesn't matter. It has the potential to profoundly change the future of all credit markets.

We recognise "PID Controller" may be one of the worst-sounding names in history... but it doesn't matter. It has the potential to profoundly change the future of all credit markets.

• • •

Missing some Tweet in this thread? You can try to

force a refresh