Latest global payment trends by McKinsey and what does it means for $MA $V $SQ $AFRM $ADYEY $STNE $SE $MELI $FB:

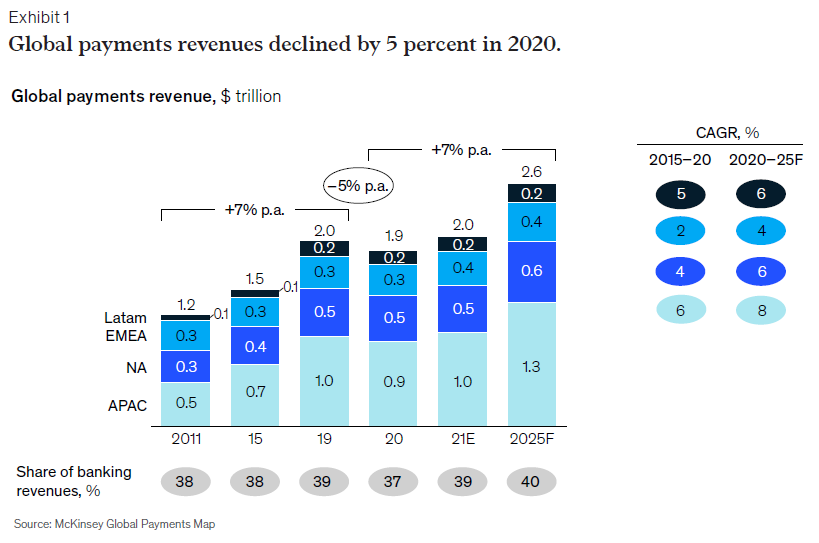

The pandemic resulted in the first decline in global payments revenues in 11 years.

But that is about to change.

Indicators point to an uneven rebound in 2021, bringing revenue back to 2019's record high.

But that is about to change.

Indicators point to an uneven rebound in 2021, bringing revenue back to 2019's record high.

McKinsey expects growth rates to return to the 6 to 7% range, generating approximately $2.5 trillion by 2025.

As 2020 payment numbers were flat, it hid an important trend—accelerated decline in cash usage and adoption of e-payments and e-commerce transactions.

This trend will outlast the pandemic.

Revenue gains in these areas were offset by tightening of net interest margins earned.

This trend will outlast the pandemic.

Revenue gains in these areas were offset by tightening of net interest margins earned.

Cash payments declined by 16% globally in 2020!

Due to:

•Lockdown of commercial venues

•Countries increasing ATM fees e.g. Argentina, Thailand, etc

•Downsizing of ATM in Europe

McKinsey estimates that 2/3 of the decrease will be permanent.

Due to:

•Lockdown of commercial venues

•Countries increasing ATM fees e.g. Argentina, Thailand, etc

•Downsizing of ATM in Europe

McKinsey estimates that 2/3 of the decrease will be permanent.

With the dramatic reduction in cash usage, there's an urgent need for regulators to promote access of e-payments for all—especially the underbanked.

E.g. In Indonesia, e-money transactions surged by nearly 39%. led by $SE and OVO.

E.g. In Indonesia, e-money transactions surged by nearly 39%. led by $SE and OVO.

Increasingly, SMEs are also equipped with tools to accept cashless payments:

•QR Code "tap to pay" and link-based payments

•$MA in India launched Soft POS to enable smartphones to function as a POS

•Social-media platforms embedded payment features e.g. $FB's Instagram

•QR Code "tap to pay" and link-based payments

•$MA in India launched Soft POS to enable smartphones to function as a POS

•Social-media platforms embedded payment features e.g. $FB's Instagram

Changing payment landscape

Past: payments providers' revenue was mostly from processing payments.

Future: most of the revenue will come from svcs that improve consumer purchase-to-pay journey.

E.g. Only 1/3 of $SQ's revenue are payments, the rest are from value-added services.

Past: payments providers' revenue was mostly from processing payments.

Future: most of the revenue will come from svcs that improve consumer purchase-to-pay journey.

E.g. Only 1/3 of $SQ's revenue are payments, the rest are from value-added services.

Follow me @SteadyCompound for more threads on:

• Investing.

• Business breakdowns.

• Company updates.

• Investing.

• Business breakdowns.

• Company updates.

If you loved this, check out my newsletter:

3 ideas on investing and growth philosophies.

Every week.

steadycompounding.com

3 ideas on investing and growth philosophies.

Every week.

steadycompounding.com

You can find the full McKinsey report here: mckinsey.com/industries/fin…

• • •

Missing some Tweet in this thread? You can try to

force a refresh