Why it’s hard to understand blockchain and its momentum unless you see it as a new type of computer?

(Thread heavily inspired by @cdixon’s lecture: “Crypto networks and why they matter.”)

🧵🧵🧵

(Thread heavily inspired by @cdixon’s lecture: “Crypto networks and why they matter.”)

🧵🧵🧵

“What problem does blockchain solve?”

It’s a common question among crypto skeptics. And it’s a fair one - typically, products that can’t solve problems are flops.

But is blockchain a product? Or is it a design space?

It’s a common question among crypto skeptics. And it’s a fair one - typically, products that can’t solve problems are flops.

But is blockchain a product? Or is it a design space?

What is a design space? It’s a platform that lets you build new things on top of it.

PCs were a design space for MS Office and video games.

Internet was a design space for social media and SaaS businesses.

iPhone was a design space for Uber, Tinder, and Google Maps.

PCs were a design space for MS Office and video games.

Internet was a design space for social media and SaaS businesses.

iPhone was a design space for Uber, Tinder, and Google Maps.

Thanks to their unique characteristics, these computing platforms let developers build a new types of apps.

And the more useful apps, the more attractive these computers became.

But it’s a double-edged sword.

The less useful apps, the less attractive the computers.

And the more useful apps, the more attractive these computers became.

But it’s a double-edged sword.

The less useful apps, the less attractive the computers.

Imagine:

PC without software,

Internet without e-mail and browser,

iPhone without apps.

They would remain just toys for a handful of geeks.

PC without software,

Internet without e-mail and browser,

iPhone without apps.

They would remain just toys for a handful of geeks.

So the goals for the computing platforms are:

1) create a design space that lets developers build a new type of apps,

2) then bring developers and entrepreneurs on board to build apps,

3) then, bring users to buy your computer so they can use the new cool apps.

1) create a design space that lets developers build a new type of apps,

2) then bring developers and entrepreneurs on board to build apps,

3) then, bring users to buy your computer so they can use the new cool apps.

When the number of good apps reaches the critical mass, it builds strong positive feedback loops. That’s what happened in PCs, the Internet, and iPhones.

But how to convince developers to produce apps for a computing platform that has almost no users?

In the PC & Internet case, the tech was interesting, so hackers built apps for other hackers. That’s why the UX of the first PCs and Internet was hard.

In the PC & Internet case, the tech was interesting, so hackers built apps for other hackers. That’s why the UX of the first PCs and Internet was hard.

https://twitter.com/benedictevans/status/1447907561831870468?t=s-FMXERWbPy58jt-Q1839g&s=19

The iPhone case was a little bit different.

Jobs made sure that the first iPhones had iTunes, Google Maps, e-mail, and the browser, to make the device useful for non-hacker users.

Jobs made sure that the first iPhones had iTunes, Google Maps, e-mail, and the browser, to make the device useful for non-hacker users.

But even despite his efforts, iPhone was pretty hard to get in the early days. So were early PCs and the early Internet.

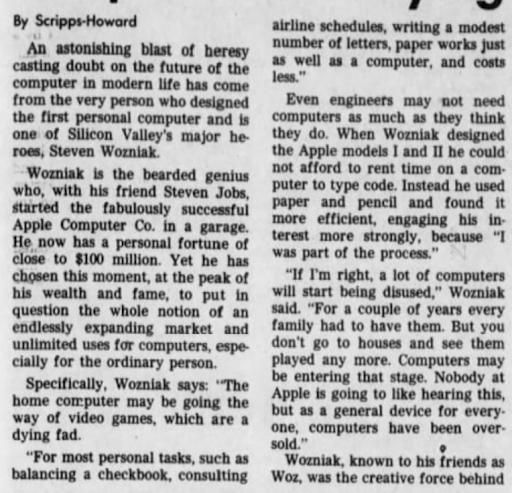

In 1985 (9 years after the foundation of Apple), Steve Wozniak, Apple Co-Founder, thought that PCs were oversold.

David Letterman was making fun of the Internet in 1995 (4 years after the first web browser) because it had almost zero truly innovative apps that were mainstream.

iPhone hasn’t been understood by journalists from TechCrunch, AdAge, Bloomberg, Guardian. And, of course, Steve Ballmer, who famously said: “There’s no chance that the iPhone is going to get any significant market share.”

bgr.com/tech/iphone-re…

bgr.com/tech/iphone-re…

This pattern repeats itself with every new computing platform. That’s because it sometimes takes years until one of the 1000s apps becomes a ‘killer app’ that makes the computer worth buying.

(For me in the 90s, the killer apps for PC were video games like Diablo)

(For me in the 90s, the killer apps for PC were video games like Diablo)

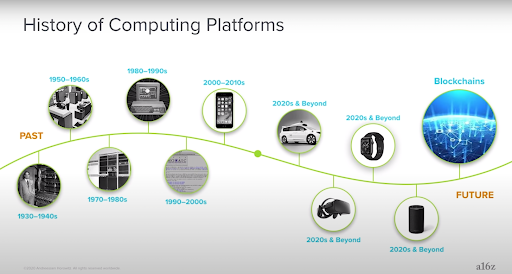

Why it’s important? Because, according to Dixon, blockchain is a new type of computer.

It’s a computer that can make commitments, which means it can hard-limit itself. And because of that, blockchain can take different shapes.

It’s a computer that can make commitments, which means it can hard-limit itself. And because of that, blockchain can take different shapes.

Bitcoin is an application-specific computer like an Xbox or calculator.

Which means it has many hard limitations. And thanks to these limitations, Bitcoin can perform its main task - storing and exchanging money - better.

Which means it has many hard limitations. And thanks to these limitations, Bitcoin can perform its main task - storing and exchanging money - better.

Ethereum, on the other hand, is a general-purpose computer like a PC or iPhone.

Thanks to fewer limitations, developers can create more apps.

That’s why there are 1000s of apps on Ethereum from art and music, through lending & borrowing, exchanges, games, and more.

Thanks to fewer limitations, developers can create more apps.

That’s why there are 1000s of apps on Ethereum from art and music, through lending & borrowing, exchanges, games, and more.

There are other types of specialized blockchain computers.

Solana is optimized for fast transactions. Arweave for file storage. And DeSo for social media.

Solana is optimized for fast transactions. Arweave for file storage. And DeSo for social media.

Because blockchain is a new type of computer, it lets you create new kinds of apps. And because ‘software eats up the world,’ it’s big news.

That’s why a16z built a giant 2.2B crypto fund.

That’s why a16z built a giant 2.2B crypto fund.

What kind of apps can now be created? Mostly apps that let you own, exchange, and distribute digital things - cryptocurrencies and tokens.

The most popular apps take the forms of Wallets, Smart Contracts, NFT marketplaces, Decentralized Exchanges, and DAOs.

The most popular apps take the forms of Wallets, Smart Contracts, NFT marketplaces, Decentralized Exchanges, and DAOs.

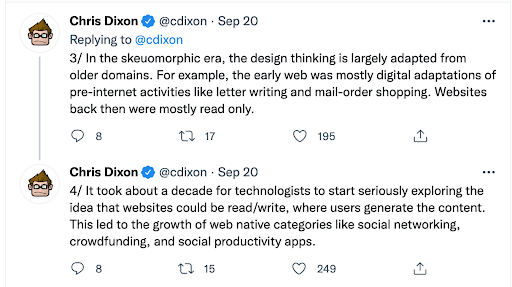

At this point, most apps are skeuomorphic.

That’s why many people go into 1995 Letterman mode and say:

“Money transfers? Does a bank ring a bell?”,

"Owning company's tokens? Do stocks ring a bell?"

“Logging in with Wallet? Does ‘Log in with Google ring a bell?”

That’s why many people go into 1995 Letterman mode and say:

“Money transfers? Does a bank ring a bell?”,

"Owning company's tokens? Do stocks ring a bell?"

“Logging in with Wallet? Does ‘Log in with Google ring a bell?”

But blockchain has already experienced real innovation.

Like play-to-earn games such as Axie Infinity that haven’t been seen before.

Like NFTs.

Or DAOs.

There are also numerous intriguing B2B applications on Hyperledger.

Like play-to-earn games such as Axie Infinity that haven’t been seen before.

Like NFTs.

Or DAOs.

There are also numerous intriguing B2B applications on Hyperledger.

Here are some ideas from the 2020 @balajis lecture about potential killer apps on Blockchain.

The slides are around 2 years old, so some of the examples might be outdated (like OpenBazaar and CryptoKitties), but it gives a glimpse into what’s happening in the space.

The slides are around 2 years old, so some of the examples might be outdated (like OpenBazaar and CryptoKitties), but it gives a glimpse into what’s happening in the space.

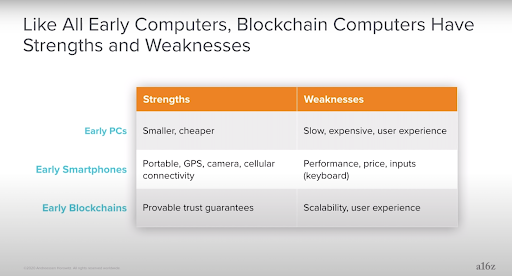

Okay, but if Blockchain is a computer, is it powerful? To build powerful apps, you need a powerful computer.

You wouldn’t create:

MS Office for 70s PC,

Fortnite for the iPhone 1,

Or Salesforce for 56kbps Internet.

And Blockchain - like all early computers - is far from perfect.

You wouldn’t create:

MS Office for 70s PC,

Fortnite for the iPhone 1,

Or Salesforce for 56kbps Internet.

And Blockchain - like all early computers - is far from perfect.

It means that some apps are now impossible to build because the infrastructure isn't good enough.

If you wanted to use blockchain, e.g., for playing Counter-Strike, it would be a disaster. You would experience big lags, and one day of playing a game would cost a fortune.

If you wanted to use blockchain, e.g., for playing Counter-Strike, it would be a disaster. You would experience big lags, and one day of playing a game would cost a fortune.

But it doesn’t need to be perfect from the start. iPhone 1 was good enough for Google Maps and Apple I was good enough for coding.

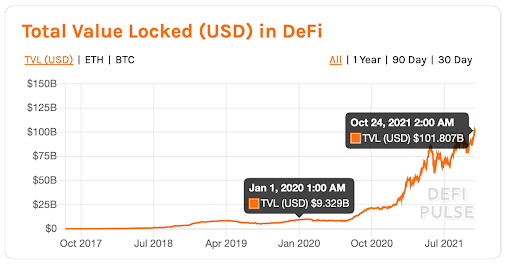

Blockchain’s present infrastructure is good enough for NFTs and DeFi.

That’s why the De-Fi market has grown over 10X since the start of 2020:

Blockchain’s present infrastructure is good enough for NFTs and DeFi.

That’s why the De-Fi market has grown over 10X since the start of 2020:

And infrastructure matters.

Moving from 3G to LTE:

1. Created space for data-heavy apps (YouTube, Snapchat, Instagram),

2. Made smartphones more useful,

3. And convinced more people to buy and use smartphones.

We might see the same effect when new blockchains get more powerful

Moving from 3G to LTE:

1. Created space for data-heavy apps (YouTube, Snapchat, Instagram),

2. Made smartphones more useful,

3. And convinced more people to buy and use smartphones.

We might see the same effect when new blockchains get more powerful

That’s why the community is working hard to improve blockchains.

Bitcoin uses Lightning.

Ethereum moves to 2.0.

New blockchains such as Solana, Polkadot, and DeSo arise.

Bitcoin uses Lightning.

Ethereum moves to 2.0.

New blockchains such as Solana, Polkadot, and DeSo arise.

Because people earn crypto for creating a network, adding features, or operating it, they have financial incentives to make Blockchains better.

As Chris points out, it’s a Moore’s Law in its economic sense:

“If a lot of smart people who know computer science start thinking about computer science problems and have an economic incentive to do so, those computers tend to get a lot lot better.”

“If a lot of smart people who know computer science start thinking about computer science problems and have an economic incentive to do so, those computers tend to get a lot lot better.”

Okay, so we have new apps, and the computer will get better. But what about developers that are key to the computing platform’s success?

Look at @DarenMatusoka’s numbers of Ethereum developers joining the network. Similar trends are observed in other major blockchains.

https://twitter.com/DarenMatsuoka/status/1446495671863762949

So blockchain, like a proper computer platform:

1) delivered a design space that lets developers build a new type of apps,

2) brought developers and entrepreneurs on board to build apps,

3) and now finally brings users to the computer so they can use the cool apps.

1) delivered a design space that lets developers build a new type of apps,

2) brought developers and entrepreneurs on board to build apps,

3) and now finally brings users to the computer so they can use the cool apps.

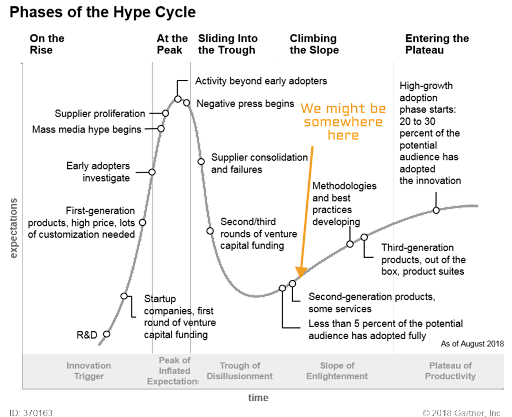

It’s not hard to notice that blockchain experienced all the hype and doubts just like the older computing platforms.

But as blockchain computers get better and developers create new apps, some products such as MetaMask reach over 10 million active users.

But as blockchain computers get better and developers create new apps, some products such as MetaMask reach over 10 million active users.

It took 12 years, but it’s not that long for such a complex technology.

Blockchain obviously won’t take over everything. Just like you don’t do spreadsheets on your iPhone, you won’t do everything on the blockchain.

But it is already a thing. And can play a vital role in the history of tech, serving as a backbone of Web3.

But it is already a thing. And can play a vital role in the history of tech, serving as a backbone of Web3.

https://twitter.com/cdixon/status/1442201621266534402

Personally, I think that most people won’t even know that they use blockchain-based apps in the future.

Like most people don’t know, they use TCP/IP protocol when they surf the web or SMTP protocol when they send their e-mails.

Like most people don’t know, they use TCP/IP protocol when they surf the web or SMTP protocol when they send their e-mails.

As blockchain computers get more users, the developers will follow, and new apps will emerge. In the same way, as it happened with PCs, the Internet, and iPhones.

That’s why the blockchain/crypto/Web3 community is so exciting to participate in. So if you’re interested in the future of the Internet, I highly recommend following this subject.

If you want to follow some crypto/blockchain/web3 OGs I recommend:

@cdixon on Web3,

@6529 on NFTs,

@packym for deep dives,

@balajis for all things blockchain/society/economy,

@FEhrsam for one-liners,

@neerajKA for current affairs commentary.

@cdixon on Web3,

@6529 on NFTs,

@packym for deep dives,

@balajis for all things blockchain/society/economy,

@FEhrsam for one-liners,

@neerajKA for current affairs commentary.

It’s the end of the thread, but II will prepare new ones where I describe:

- 5 blockchain’s killer features,

- How do they translate into Web3 opportunities,

- And the potential road forward.

So if you don’t want to miss them, follow me @macbudkowski :)

- 5 blockchain’s killer features,

- How do they translate into Web3 opportunities,

- And the potential road forward.

So if you don’t want to miss them, follow me @macbudkowski :)

PS: I’m starting a podcast where I’ll talk with Web3 builders and investors.

The goal is to share high-level inspirational ideas and low-level practical solutions necessary to make the Web3 project succeed.

It'll start in November and you can sub here:

web3talks.substack.com

The goal is to share high-level inspirational ideas and low-level practical solutions necessary to make the Web3 project succeed.

It'll start in November and you can sub here:

web3talks.substack.com

The handle of 6529 is ofc @punk6529

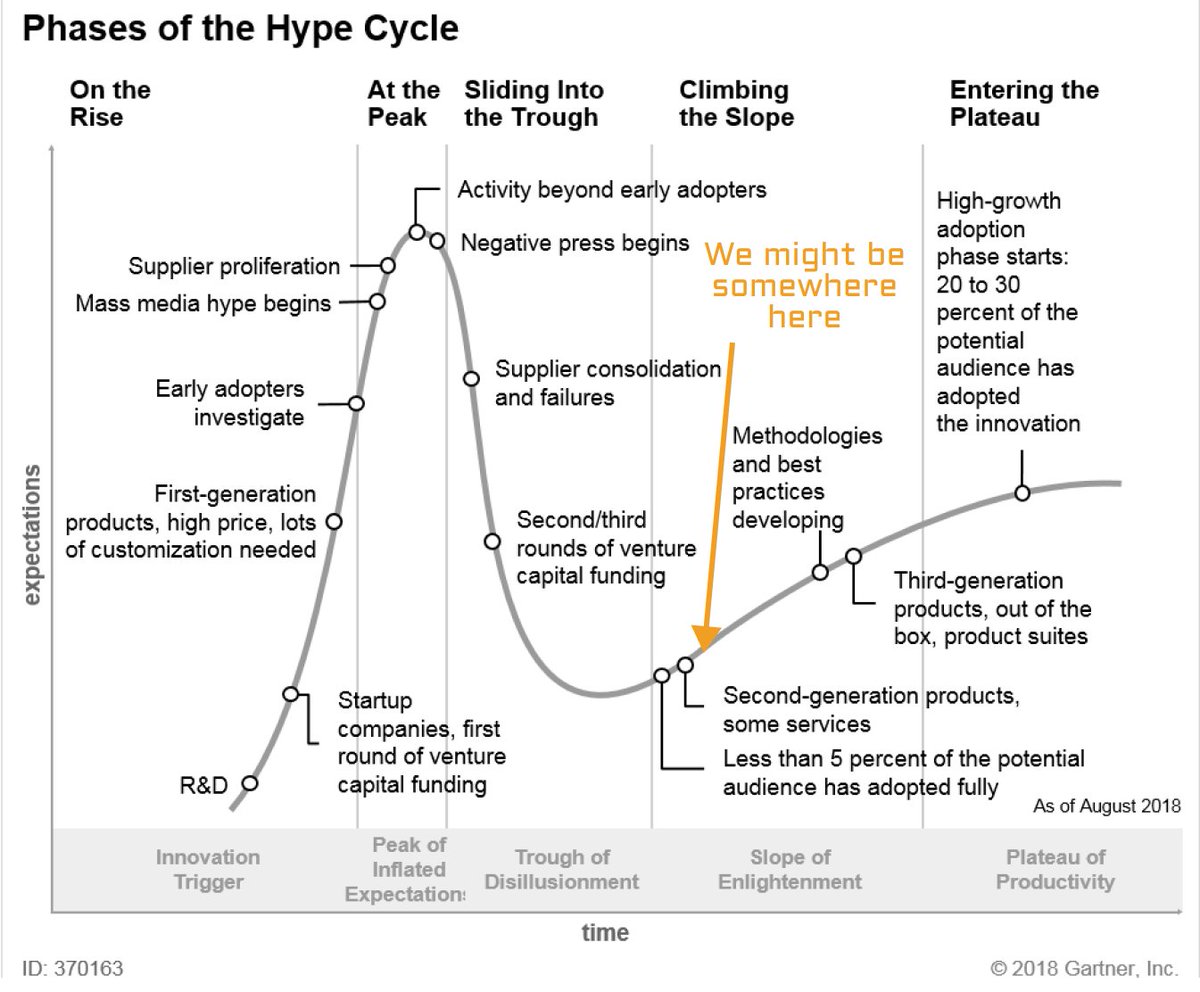

The hype cycle chart breaks on mobile, here's the correct pic

• • •

Missing some Tweet in this thread? You can try to

force a refresh