1/ Releasing a redacted Lux quarterly letter to LPs.

Some strong views of

-a catalog of an excess of excesses

-what catalysts cause the current market frenzy to end

(preview: LP indigestion)

-what we are advising our Lux family companies

-much more…

Some strong views of

-a catalog of an excess of excesses

-what catalysts cause the current market frenzy to end

(preview: LP indigestion)

-what we are advising our Lux family companies

-much more…

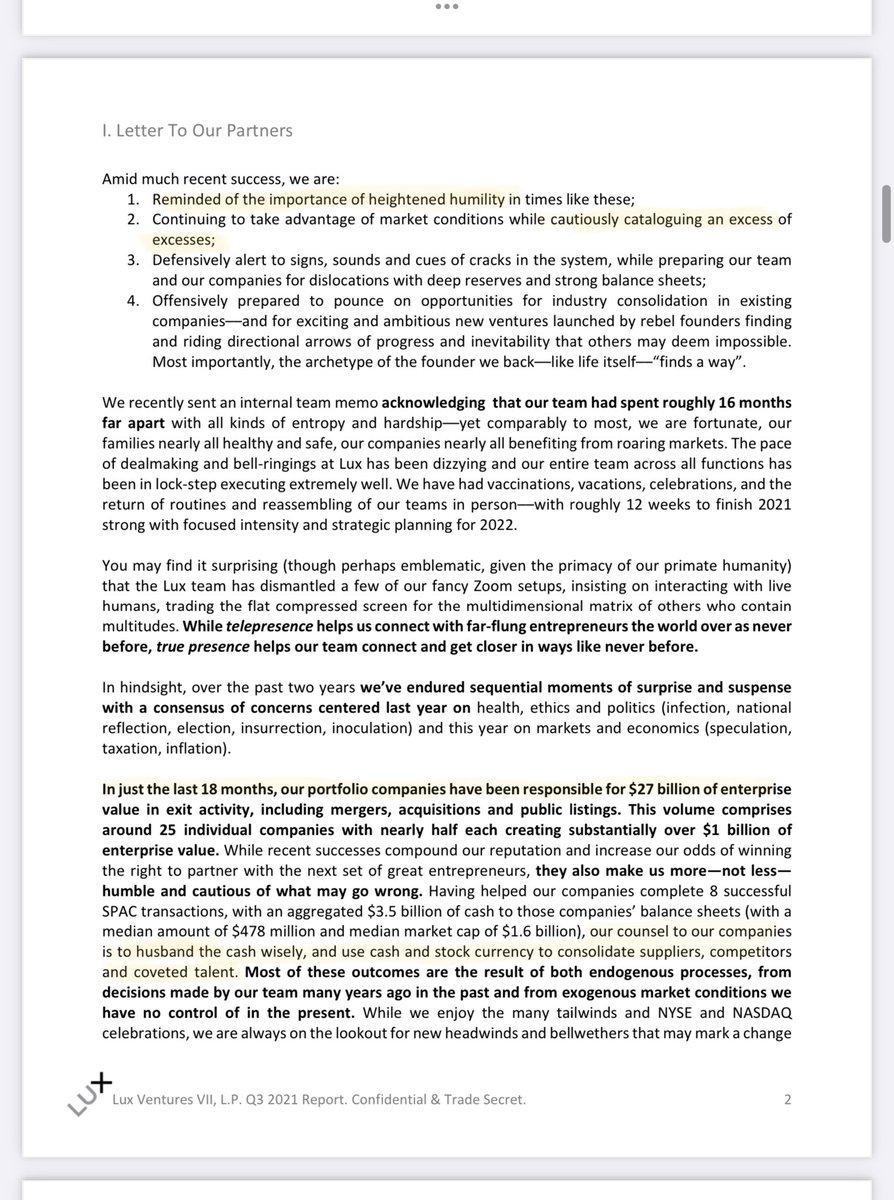

2/-The importance of HEIGHTENED HUMILITY in times like these (where source of ‘success’ can be easily mistaken)

-Telepresence helps us connect with far-flung founders but true presence (in person) helps our team connect like never before

-Where a CONSENSUS of CONCERNS is CENTERED

-Telepresence helps us connect with far-flung founders but true presence (in person) helps our team connect like never before

-Where a CONSENSUS of CONCERNS is CENTERED

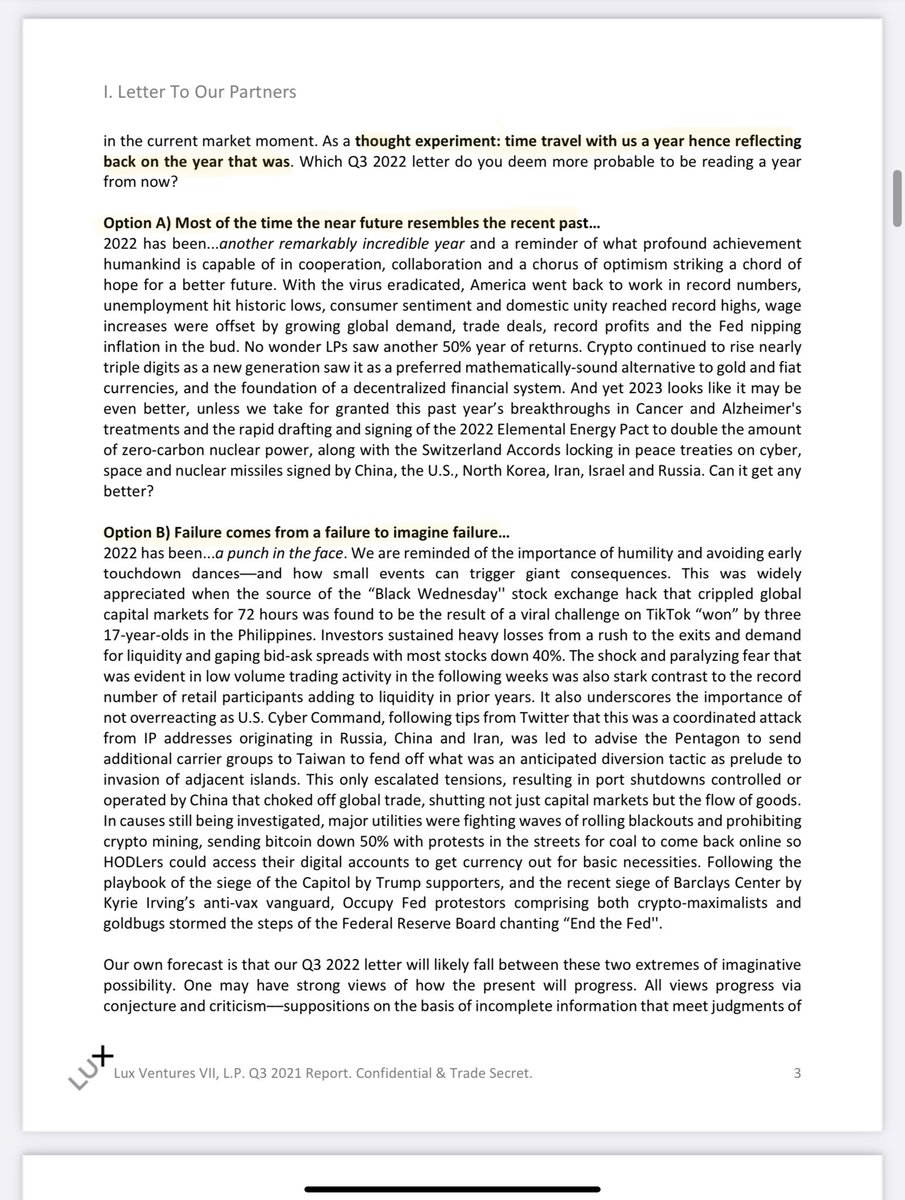

3/ Time travel with us a year hence—

reflecting back on the year that was.

Which of the 2 paragraphs below do you expect to read in Q3 2022?

reflecting back on the year that was.

Which of the 2 paragraphs below do you expect to read in Q3 2022?

4/-Is now time for CAUTION or throwing CAUTION to the wind?

-Valuations have risen

diligence fallen &

EXCESS is in EXCESS

-Preparing for the turn—when it comes

is wiser than predicting—when it may

-Valuations have risen

diligence fallen &

EXCESS is in EXCESS

-Preparing for the turn—when it comes

is wiser than predicting—when it may

5/ An excess of excesses—or what things wicked may this way come…

As Fed + central banks dole out dramatic distortion of discount rates, duration and the “true” cost of capital into markets…

A scene from ‘Deadwood’ comes to mind…

As Fed + central banks dole out dramatic distortion of discount rates, duration and the “true” cost of capital into markets…

A scene from ‘Deadwood’ comes to mind…

6/

-In just the last 12 weeks, startups raised more than the entire 99-00 .com boom/bust

-Character is built thru hardship + steep slopes

Yet today’s hero’s journey has given way to flattened slopes

-Thus far all news has been good news—which to realists—portends bad news.

-In just the last 12 weeks, startups raised more than the entire 99-00 .com boom/bust

-Character is built thru hardship + steep slopes

Yet today’s hero’s journey has given way to flattened slopes

-Thus far all news has been good news—which to realists—portends bad news.

7/ Failures comes from a failure to imagine failure

Good times let guards down

making co’s vulnerable to the silent artillery of time

LP’s whiteboard of GPs coming to market

looks like A Beautiful Mind

indigenstion of LPs + pace of new commitments

cant match pace of new raises

Good times let guards down

making co’s vulnerable to the silent artillery of time

LP’s whiteboard of GPs coming to market

looks like A Beautiful Mind

indigenstion of LPs + pace of new commitments

cant match pace of new raises

9/ The “Hemingway Hinge”…

A few funds with AUM $50-100B taking page from Carlyle,Apollo, KKR + now TPG will…

turn once cultivated intimate partnerships

into calculated intentions to go public becoming institutional corporations, fully diversified supermarkets

A few funds with AUM $50-100B taking page from Carlyle,Apollo, KKR + now TPG will…

turn once cultivated intimate partnerships

into calculated intentions to go public becoming institutional corporations, fully diversified supermarkets

10/

-We have benefited from unusual demand—just as we caution against its unlikely persistence in its current form.

-we said 90% of SPACs would be CRAPs

-Some deals will prove…less kosher than a kilebasa sausage smothered in swiss cheese

-The Appointment in Samarra…

-We have benefited from unusual demand—just as we caution against its unlikely persistence in its current form.

-we said 90% of SPACs would be CRAPs

-Some deals will prove…less kosher than a kilebasa sausage smothered in swiss cheese

-The Appointment in Samarra…

11/ Indefinitely Modified Paths—the wisdom of William James & Jurassic Park.

“Life finds a way”… and so do incredible founders

in every cutting-edge industry we find + fund…

“Life finds a way”… and so do incredible founders

in every cutting-edge industry we find + fund…

12/

Space race is real—over 12 nations have astral aspirations

took humanity til 1961 to launch 1st 👨🚀 in space

last mo there were 14 in space @ same time

Do wise things when others are doing provably foolish things

And do what may appear to be foolish that’ll prove to be wise

Space race is real—over 12 nations have astral aspirations

took humanity til 1961 to launch 1st 👨🚀 in space

last mo there were 14 in space @ same time

Do wise things when others are doing provably foolish things

And do what may appear to be foolish that’ll prove to be wise

• • •

Missing some Tweet in this thread? You can try to

force a refresh