So Asana is the latest SaaS leader to grow even >faster< as it scales

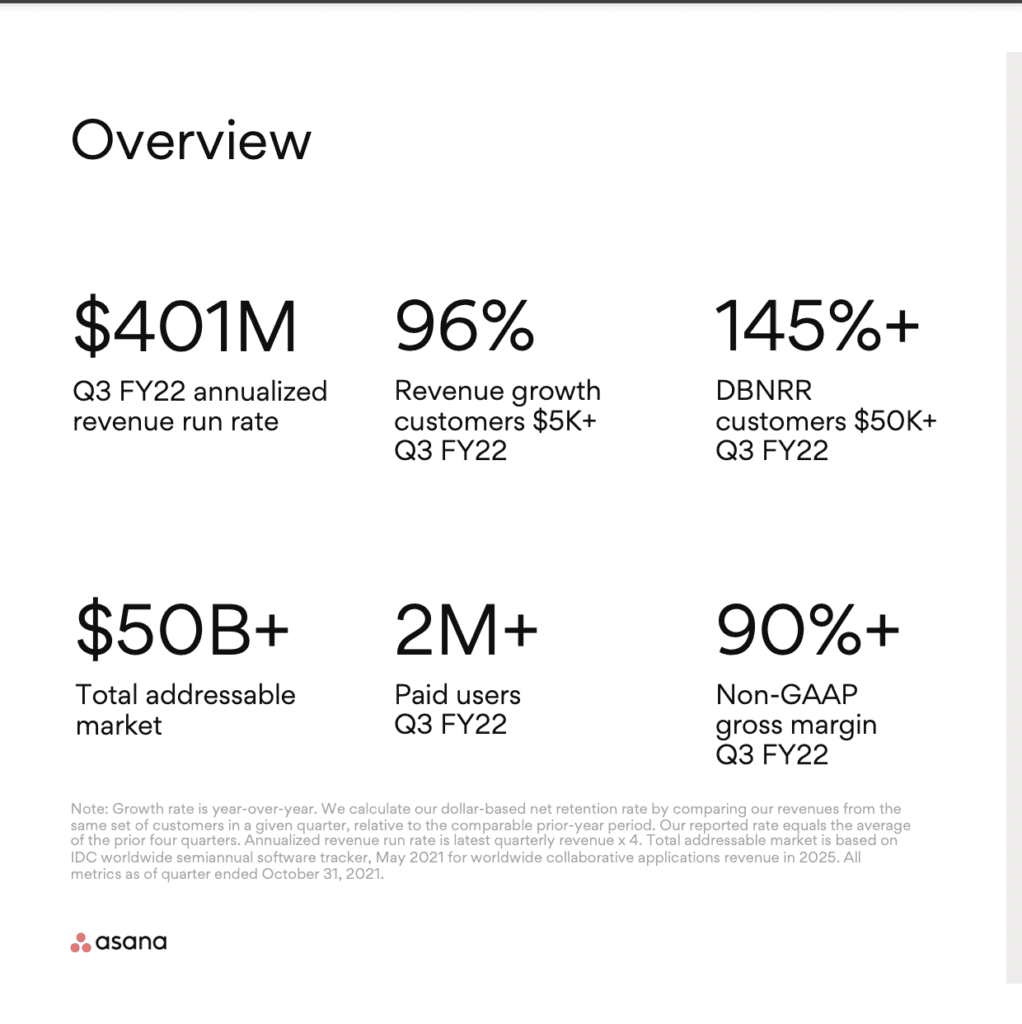

At $400m+ ARR, it's growing a stunning 70%

And that's up from 55% at $200m+ in ARR

5 Interesting Learnings: 🔽🔽🔽🔽🔽

At $400m+ ARR, it's growing a stunning 70%

And that's up from 55% at $200m+ in ARR

5 Interesting Learnings: 🔽🔽🔽🔽🔽

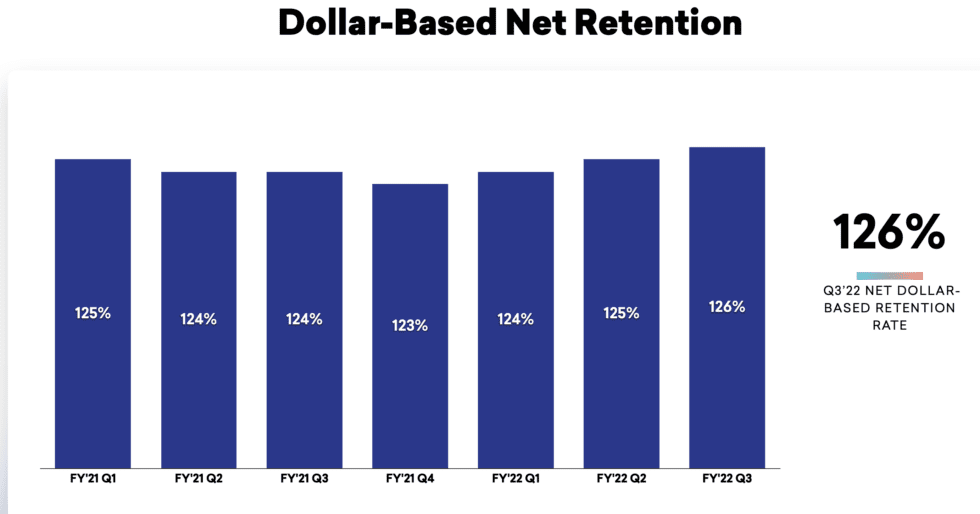

1. NRR up, from 115% to 120%. And 145% for $50k+ ACV deals.

A good reminder that NRR doesn’t need to come down as you scale. Somehow, we find a way not to saturate our markets, our customers, and our total potential deal sizes.

A good reminder that NRR doesn’t need to come down as you scale. Somehow, we find a way not to saturate our markets, our customers, and our total potential deal sizes.

And Asana’s ARR has gone up in >all< categories, from 140% to 145% for its $50k+ customers, 130% for $5k+ customers, and from 115% to 120% overall.

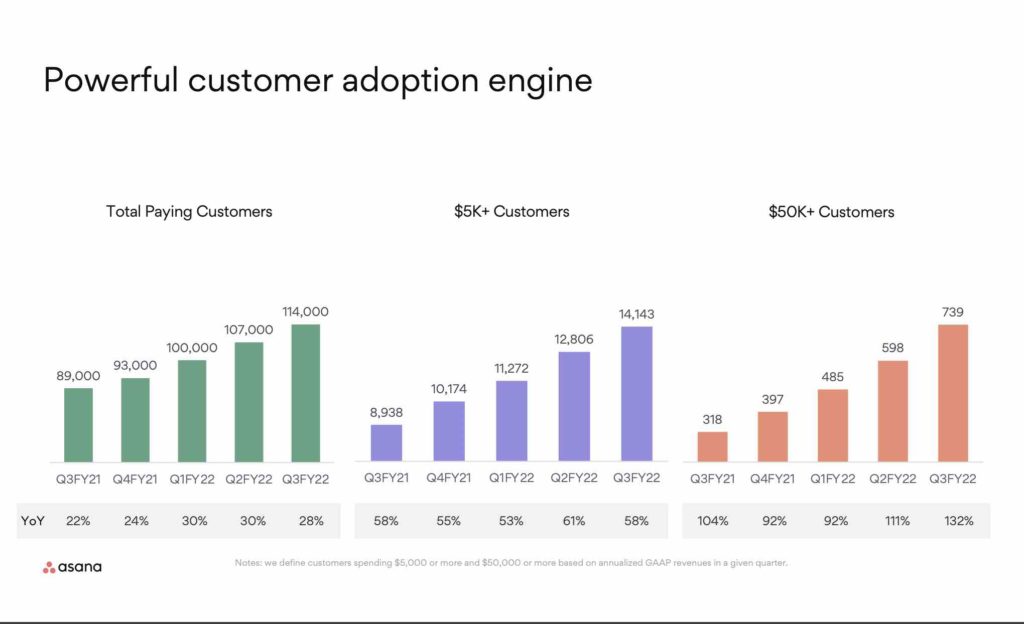

2. 114,000 total customers or about $3,500 per customer on average.

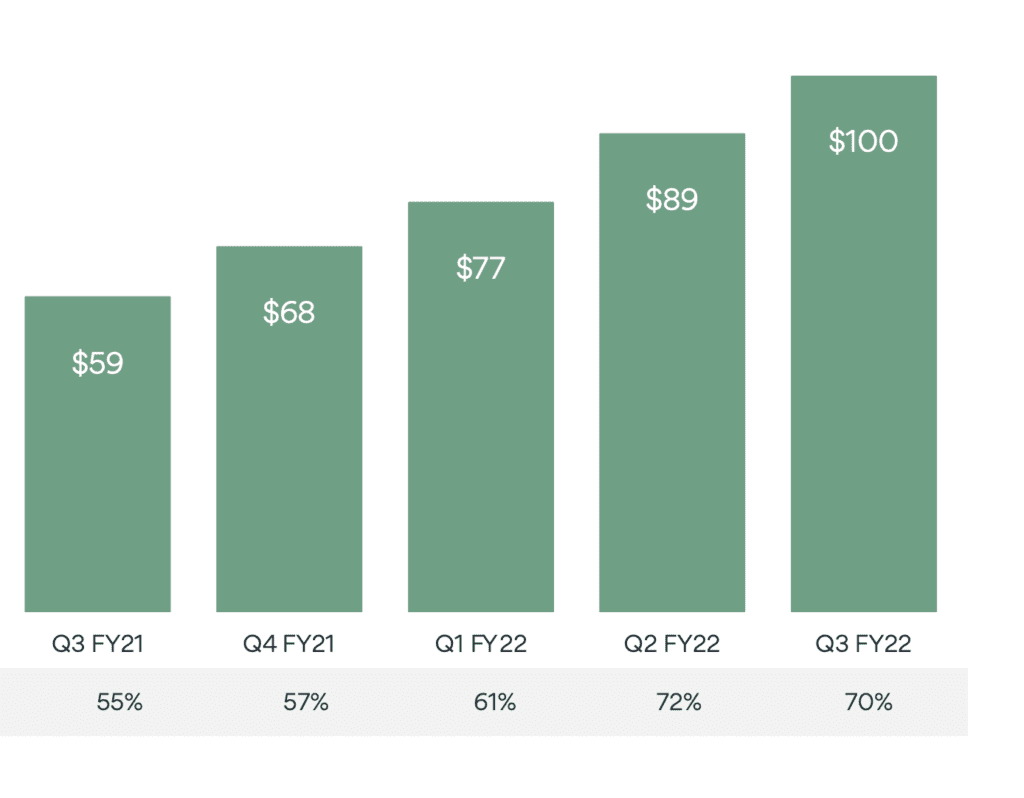

The average deal size is up about 25% since $240m ARR, when the average deal was $2,800 a year, meaning a decent piece of Asana’s growth has been from growing the ACVs +25%

The average deal size is up about 25% since $240m ARR, when the average deal was $2,800 a year, meaning a decent piece of Asana’s growth has been from growing the ACVs +25%

3. 96% Growth from $5k+ ACV customers. And 132% growth in $50k+ customers.

That’s the pull at Asana, the bigger customers. Not necessarily huge customers. But bigger. And it’s the $50k+ segment that’s growing by far the fastest.

That’s the pull at Asana, the bigger customers. Not necessarily huge customers. But bigger. And it’s the $50k+ segment that’s growing by far the fastest.

4. 42% of customers from outside the U.S.

What we see with best-of-breed apps that can be used anywhere. Aim for 35%-40% at your SaaS company, if users anywhere can get full value from your product. And localize early!

What we see with best-of-breed apps that can be used anywhere. Aim for 35%-40% at your SaaS company, if users anywhere can get full value from your product. And localize early!

5. Asana has accelerated >each< quarter since $200m ARR.

Each and every quarter it has grown faster than the quarter before. Wow.

It's never easy, but it shows there are few limits to the leaders in SaaS

You can accept slowing growth. Or you can be challenged by Asana

Each and every quarter it has grown faster than the quarter before. Wow.

It's never easy, but it shows there are few limits to the leaders in SaaS

You can accept slowing growth. Or you can be challenged by Asana

• • •

Missing some Tweet in this thread? You can try to

force a refresh