So every day there are more and more massive funding rounds

But where does all that money >come from<?

1/ From "Limited Partners", the ones that give VCs $ to invest

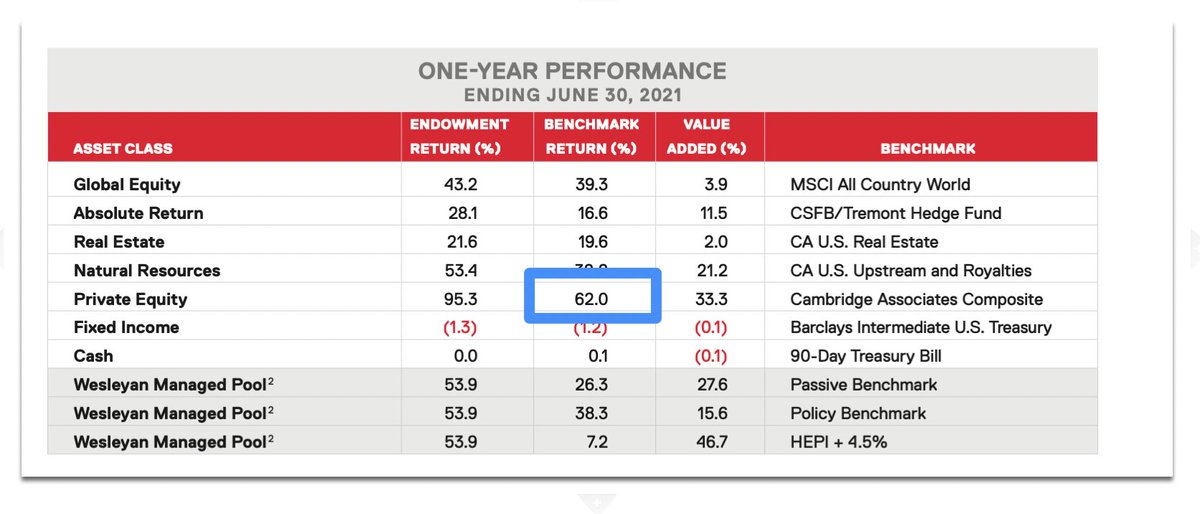

And they had an incredible year

Top endowments and LPs saw a jaw-dropping 62% (!) returns from VC + PE in 2021

But where does all that money >come from<?

1/ From "Limited Partners", the ones that give VCs $ to invest

And they had an incredible year

Top endowments and LPs saw a jaw-dropping 62% (!) returns from VC + PE in 2021

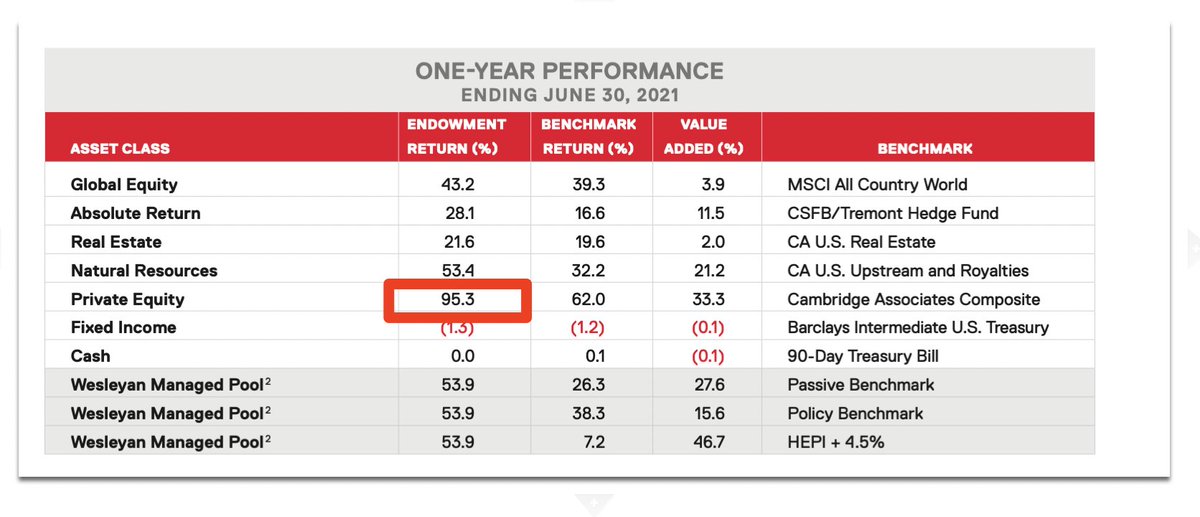

2/ Top LPs (endowments, universities, family offices, etc) did even better than that

Wesleyan's endowment for example grew 54% overall last year, and 95% from venture and private equity (!!)

Woah

And many / most are (re-)investing even more into VC + PE after those gains

Wesleyan's endowment for example grew 54% overall last year, and 95% from venture and private equity (!!)

Woah

And many / most are (re-)investing even more into VC + PE after those gains

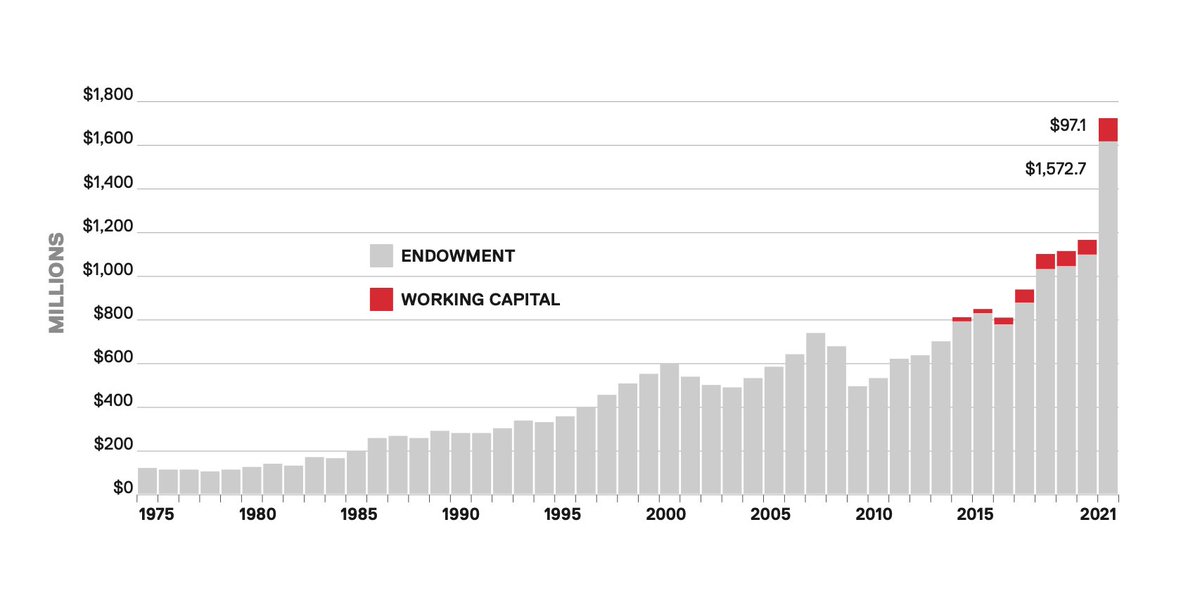

3/ As you can, these huge gains (even though many are on paper), so swell endowments that for now, even with some market tumult, there's more and more investment dollars to go into venture and PE

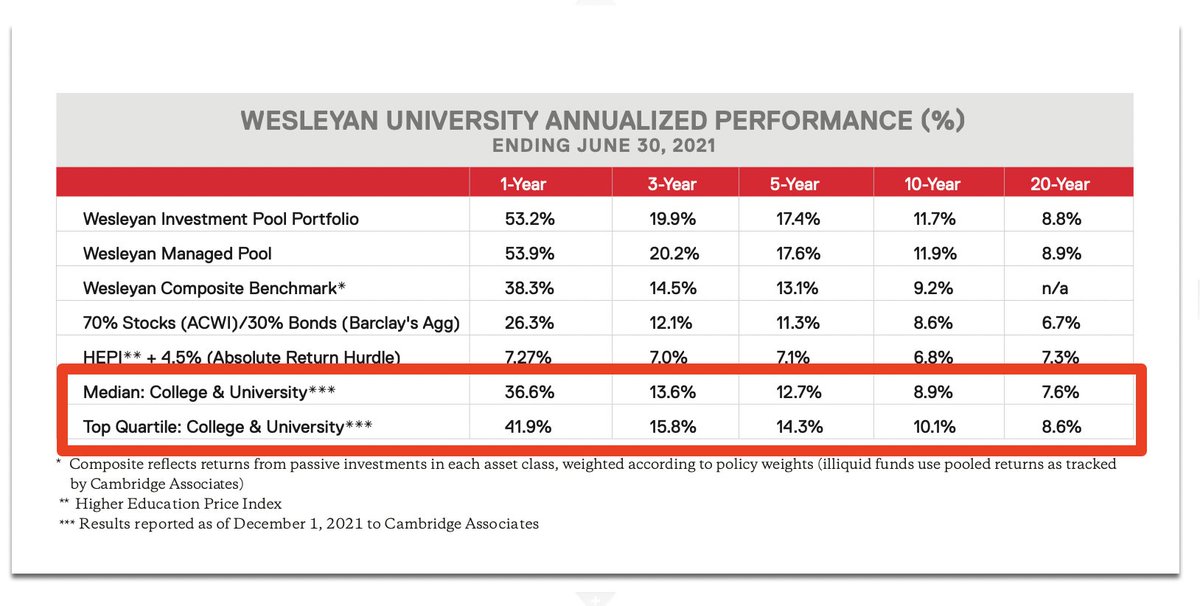

Look how much Wesleyan's endowment grew in 2021, and it's a relatively small one:

Look how much Wesleyan's endowment grew in 2021, and it's a relatively small one:

4/ With endowment growth, they themselves need to write larger checks to keep it up

This drives capital to Opportunity Funds, Growth Funds, Select Funds, etc. They can deploy a lot of capital, much more than a seed fund alone

So you are seeing LPs happy to fund these vehicles

This drives capital to Opportunity Funds, Growth Funds, Select Funds, etc. They can deploy a lot of capital, much more than a seed fund alone

So you are seeing LPs happy to fund these vehicles

5/ Even though some LPs are skeptical how long the great times will last, the results are unprecedented

You can see top Median University performance was 42% last year vs. 10% average past decade

With VC + PE the top asset class (it isn't always)

You can see top Median University performance was 42% last year vs. 10% average past decade

With VC + PE the top asset class (it isn't always)

6/ The bottom line is if your top managers (VC firms) are coming back to you with 60%, 80%, 100%+ IRR

Even if some is on paper. But there are plenty of IPOs and liquidity events.

You have to invest ever more to keep up the growth rate of your endowment

= much more $$ to VC

Even if some is on paper. But there are plenty of IPOs and liquidity events.

You have to invest ever more to keep up the growth rate of your endowment

= much more $$ to VC

• • •

Missing some Tweet in this thread? You can try to

force a refresh