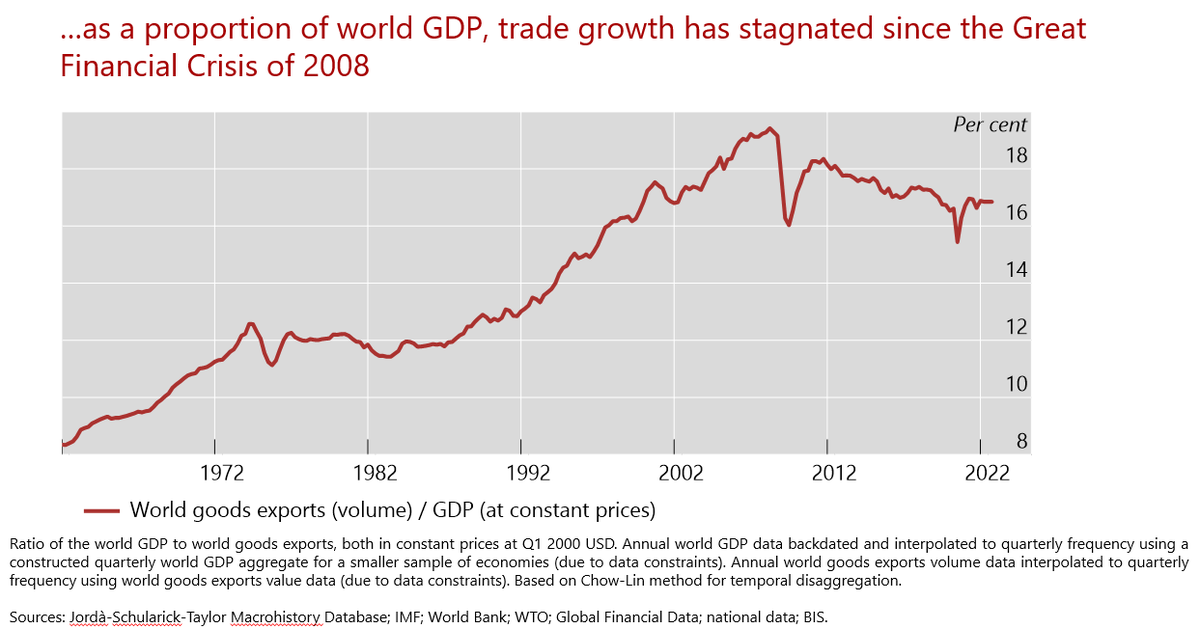

House prices boomed during the Covid recession - a big departure from past recessions

Where house prices go from here will be a key determinant of global activity

A thread from our latest #BIS_Bulletin on the topic

bis.org/publ/bisbull50…

Where house prices go from here will be a key determinant of global activity

A thread from our latest #BIS_Bulletin on the topic

bis.org/publ/bisbull50…

First, it's worth stressing how unusual the Covid recession was in terms of house prices

Typically, economic downturns are followed by a moderate fall in house prices lasting about four quarters

This time round, there was not even a temporary dip

Typically, economic downturns are followed by a moderate fall in house prices lasting about four quarters

This time round, there was not even a temporary dip

https://twitter.com/BIS_org/status/1501947247738585092

At the same time, the international co-movement of house prices has strengthened; more than 60% of house price movements can now be explained by a common global factor

Small open economies (both advanced and emerging) have been at the sharp end of this development

Small open economies (both advanced and emerging) have been at the sharp end of this development

Special Covid-related factors (demand for space, strong liquidity asset positions of households) were partly responsible

But they combined with the more timeless factors such as easy financing conditions and reaching for yield in pushing up prices

But they combined with the more timeless factors such as easy financing conditions and reaching for yield in pushing up prices

But before sounding the alarm, it's worth noting that household and bank leverage are not flashing red as they did before the GFC

More accurately, they are not flashing red everywhere; there is a great deal of diversity in country experiences

More accurately, they are not flashing red everywhere; there is a great deal of diversity in country experiences

Where do we go from here?

To get some answers, the #BIS_Bulletin undertakes two analytical exercises

First is a simulation based on past data using "random forest" machine-learning methods (don't ask - just read the piece) on what we might encounter depending on interest rates

To get some answers, the #BIS_Bulletin undertakes two analytical exercises

First is a simulation based on past data using "random forest" machine-learning methods (don't ask - just read the piece) on what we might encounter depending on interest rates

Need to step away for a second; to be continued

Short-term declines in nominal house prices usually occur when GDP growth is negative and annual credit growth is below a 5–10% threshold

Higher interest rates need not trigger immediate house price declines if there is growth and rising incomes; debt service capacity matters

In a bid to study the impact of higher interest rates, the #BIS_Bulletin also looks at how the price-to-rent ratio might depend on mortgage rates and extrapolations of capital gains

The house price trajectory depends on assumptions about the path of interest rates; with no change in interest rates, the model predicts further appreciation before reversing to levels consistent historical user cost levels

With a gradual tightening of monetary policy of 100-200 bps, house price rises would be more muted, averting a boom-bust-style adjustment

Needless to say, how house prices evolve from here could have material implications for real activity going forward

For the median economy in our sample, a 10% increase in house prices boosts consumption growth in the following year by 2.2 percentage points

The effect is quite symmetric; a 10% decline lowers consumption growth by 2.2 ppts - a big hit

The effect is quite symmetric; a 10% decline lowers consumption growth by 2.2 ppts - a big hit

But it's worth stressing how diverse the international experience has been; small open economies (both advanced and emerging) have seen the largest housing booms with the greatest increases in household debt to historical highs

No doubt, the short-term impact of rising house prices has been a tailwind for growth

But we should be attuned to the risks of a reversal; in economies with high historical valuations and household debt, demand tailwinds could turn into headwinds

But we should be attuned to the risks of a reversal; in economies with high historical valuations and household debt, demand tailwinds could turn into headwinds

The macroprudential toolkit (loan-to-value caps, debt service-to-income caps) can help;

Monetary policy cannot neglect these risks, either

Monetary policy cannot neglect these risks, either

Fixing broken thread

https://twitter.com/HyunSongShin/status/1502248599899488260?s=20&t=CxdMXXQxO8Y2gfcnxlUKPQ

• • •

Missing some Tweet in this thread? You can try to

force a refresh