I recommend reading the full “deal” to reopen Nickel trade at LME on Wednesday, 16 March.

I mean are u kidding me: $3.5bn trades canceled! The guy still short 150,000 tonnes! Refused to “be closed out”!? JPM agreeing not to increase margins etc…!

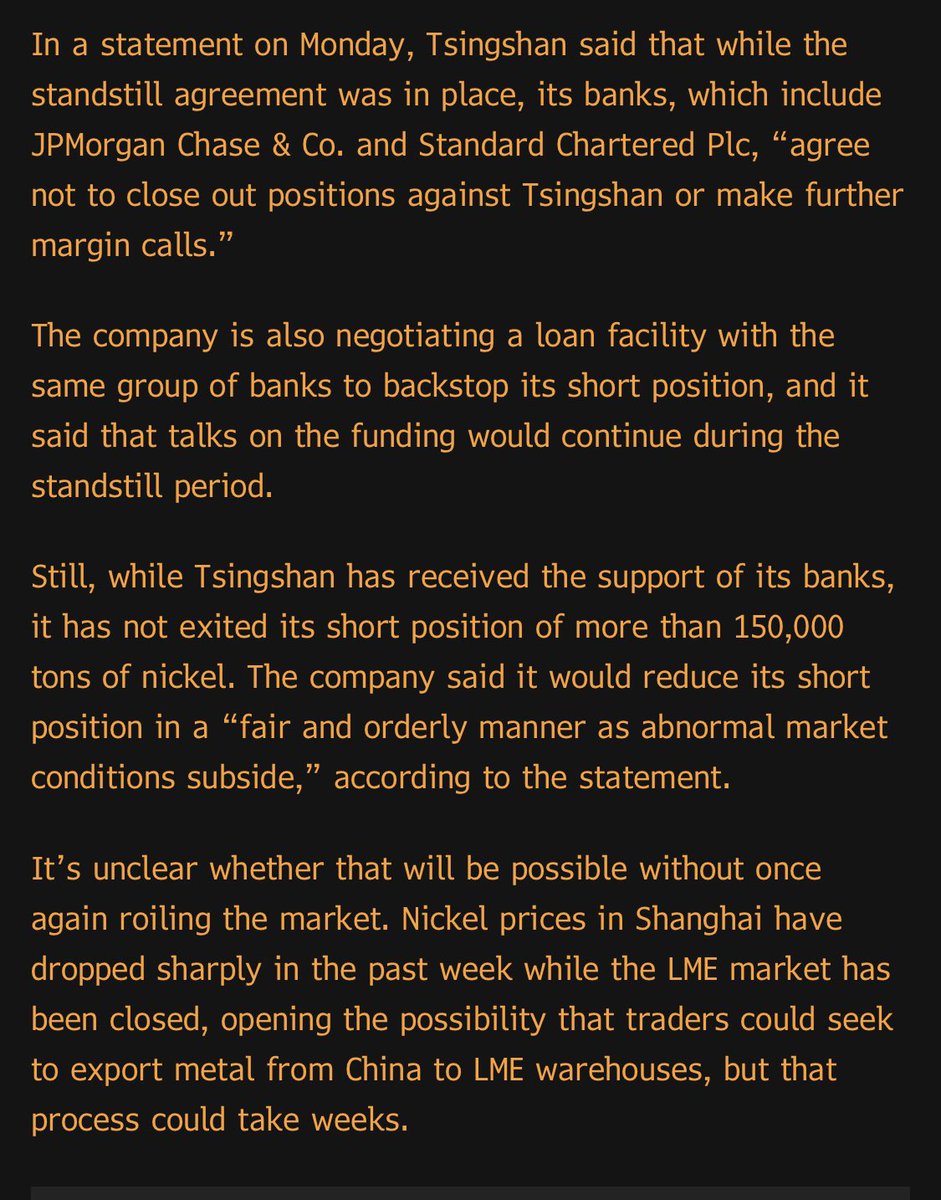

1/5 #Nickel

I mean are u kidding me: $3.5bn trades canceled! The guy still short 150,000 tonnes! Refused to “be closed out”!? JPM agreeing not to increase margins etc…!

1/5 #Nickel

2/5

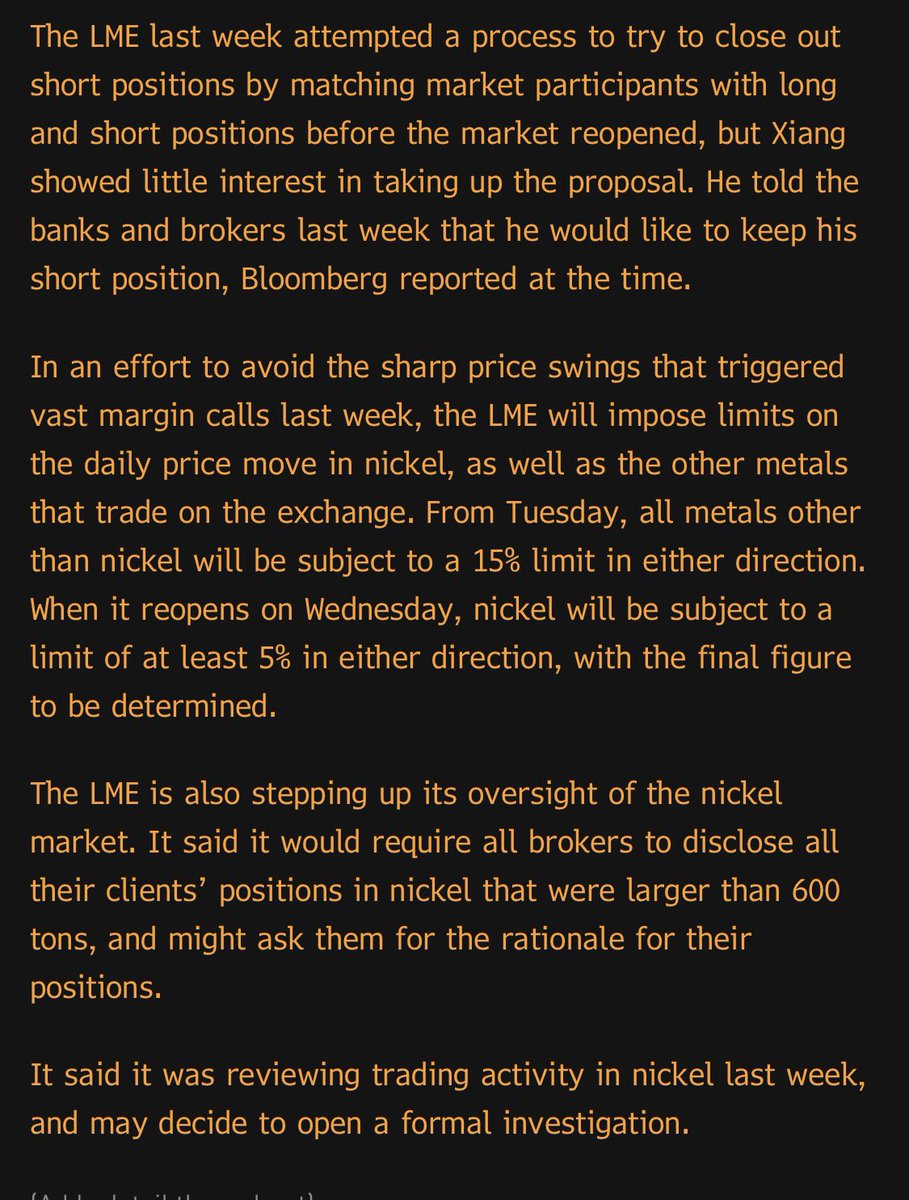

3/5

4/5

5/5

• • •

Missing some Tweet in this thread? You can try to

force a refresh