Does #Paytm have a good business model? - A thread

Watch the video :

Investors Resources : valueeducator.com/investor-resou…

Like and Retweet for Max Reach !

Read the thread below 👇

Watch the video :

Investors Resources : valueeducator.com/investor-resou…

Like and Retweet for Max Reach !

Read the thread below 👇

There is a lot of talk about how Paytm’s business is bad. Let us take a look to see if that is true.

1. Company Overview

Paytm is a payments led super app which allows its customers to access financial and other commercial services through its app. It was founded by

1. Company Overview

Paytm is a payments led super app which allows its customers to access financial and other commercial services through its app. It was founded by

Vijay Shekhar Sharma in 2009 as a prepaid mobile and DTH recharge platform. The company has since evolved to provide multiple fintech services and is one of the largest players in the payments space

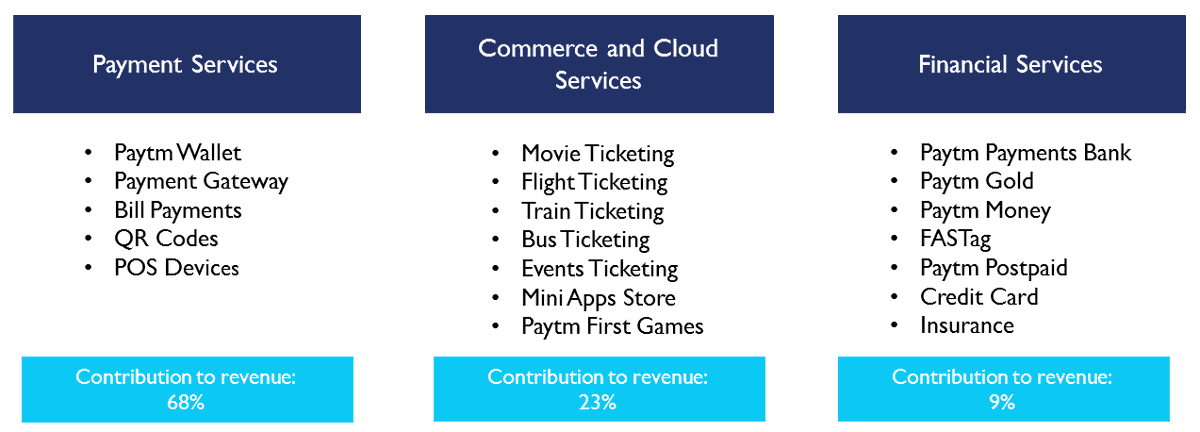

2. Business Segments

Paytm’s services are segregated into 3 main categories: Payment Services, Commerce and Cloud Services and Financial Services.

Payment Services: This is the company’s largest vertical and contributes to about 68% of their revenues.

Paytm’s services are segregated into 3 main categories: Payment Services, Commerce and Cloud Services and Financial Services.

Payment Services: This is the company’s largest vertical and contributes to about 68% of their revenues.

Paytm offers customers a platform to transfer money to other people and also pay for various services. Some of the payments that customers can make on their platform are mobile and DTH recharge, pay for utilities like gas, electricity and water, pay for their credit cards, etc.

They offer services to merchants like QR codes to accept offline payments, payment gateways to accept online payments and the soundbox that you may have seen in the stores. They charge consumers a convenience fee in certain cases and charge merchants payment processing fees.

They also receive rentals for the Soundbox device.

Commerce and Cloud Services: This vertical contributes about 23% of their revenues. Under commerce services, the company offers services like ticket booking for travel like flights, trains & buses and also entertainment like

Commerce and Cloud Services: This vertical contributes about 23% of their revenues. Under commerce services, the company offers services like ticket booking for travel like flights, trains & buses and also entertainment like

movies and events. Under cloud services, the company has Paytm First Games - which is their real money gaming platform where you can play games like poker, rummy and fantasy cricket. The company also has mini apps on its platforms.

These are basically smaller versions of ecommerce apps that you can order directly from the paytm app. They also sell ads on their platform which comes under their cloud services. For the ticket booking, Paytm charges the customers a convenience fee.

They also charge them a platform fee or a subscription for their first games platform. Paytm charges merchants a payment processing fee and for commerce and a hosting fee for mini games. They charge merchants marketing and advertising fee for the ads on their platform.

Financial Services: This vertical currently contributes only 9% of the company’s income but the company’s plan is to grow this vertical to make it their biggest revenue generator. Under this vertical, the company has a payments bank called Paytm Payments Bank

through which they offer customers some limited banking services. They also have a platform where they offer loans through other banks or NBFCs. Paytm money where they offer customers trading and demat accounts and mutual funds also falls under this segment.

They also offer insurance and digital gold on their platform. Paytm is also one of the leading issuers of Fastag where they facilitate electronic toll collection through RFID technology. Under this vertical, they earn brokerage and fees from customers and merchants.

They also charge merchants payment gateway charges, sourcing and collection fees.

3. Is the business model good?

So, now that we know how the company makes money, do we think that the business is all bad? The answer to that is no. Paytm is involved in a lot of businesses and not all of them are great or scalable.

So, now that we know how the company makes money, do we think that the business is all bad? The answer to that is no. Paytm is involved in a lot of businesses and not all of them are great or scalable.

But there are parts of the company’s business model where they are absolute leaders and the opportunity size is large. So let us divide Paytm’s various businesses into 3 buckets - the good businesses, the bad businesses and the undecided.

The Good Businesses: Payments, Lending, Payments Bank and Fastag fall under this category.

The Bad Businesses: The company’s ticketing business and most of their financial services like stocks, mutual funds, insurance, gold, etc fall under this category.

The Bad Businesses: The company’s ticketing business and most of their financial services like stocks, mutual funds, insurance, gold, etc fall under this category.

Both of these businesses operate in a hypercompetitive environment and it is unlikely that the company will be a leader in either of these businesses.

The Undecided: Paytm's cloud business falls under this category. Paytm First Games, Mini Apps and Advertising have the potentia

The Undecided: Paytm's cloud business falls under this category. Paytm First Games, Mini Apps and Advertising have the potentia

l to be huge revenue generators in the future. But it is too soon to tell if they will be very important to the company going forward.

4. Payments

Paytm is the largest player in the payments space in India. In the financial year 2020, they held about 50% market share of the Person to Merchant (P2M) payments. While PhonePe and Google Pay have higher market share in UPI, UPI makes up only 41% of the payments i

Paytm is the largest player in the payments space in India. In the financial year 2020, they held about 50% market share of the Person to Merchant (P2M) payments. While PhonePe and Google Pay have higher market share in UPI, UPI makes up only 41% of the payments i

n value terms. The rest is made up of other payment modes like credit cards, debit cards, etc. UPI is not monetizable but credit and debit cards are monetizable. Paytm is essentially a payment gateway that lets you pay through any payment instrument like cards, netbanking,

wallet and not just UPI. They also provide online merchants with a payment gateway to accept online payments which is fully monetizable. They compete with other players like Billdesk, Razorpay and PayU in this space.

They also provide merchants with the soundbox and POS (card swipe machine) under payment services. So they can provide customers with omni channel payments solutions i.e instruments to accept payments through online and offline means.

5. Fastag

Fastag uses RFID technology to enable electronic toll collection in India. ICICI bank and Paytm Payments Bank are the 2 leaders in issuing Fastag. Over the past 6 months, ICICI Bank issued 26% of Fastags in India and Paytm issued 23%. This is important because the

Fastag uses RFID technology to enable electronic toll collection in India. ICICI bank and Paytm Payments Bank are the 2 leaders in issuing Fastag. Over the past 6 months, ICICI Bank issued 26% of Fastags in India and Paytm issued 23%. This is important because the

issuing bank gets a 1.5% fee for processing the toll payment. There is a ₹100 issuing fee which has to be paid every 5 years. So by issuing more fastags, the company gets annuity revenues every 5 years and the cost for issuing the tag is very low. (Continued)

The company collects fees every time a toll is paid too, for which they have no costs.

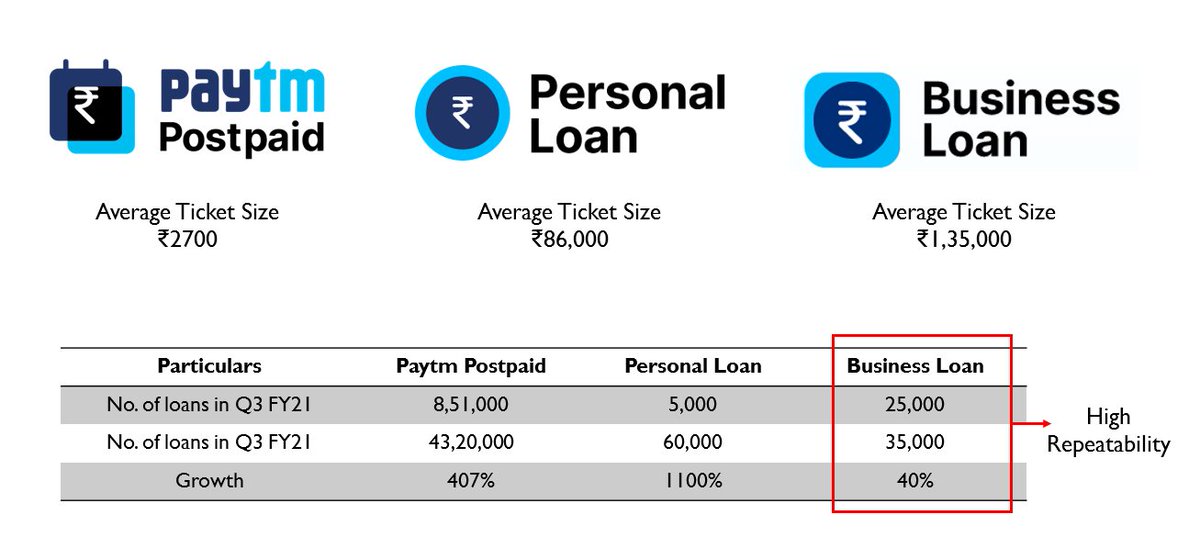

6. Lending Business

The company is not directly involved in lending but provides a platform to banks and NBFCs to lend on their platform. The company has 3 main products in this vertical - Paytm Postpaid, which is their buy now pay later product,

The company is not directly involved in lending but provides a platform to banks and NBFCs to lend on their platform. The company has 3 main products in this vertical - Paytm Postpaid, which is their buy now pay later product,

Personal loans and Merchant loans. The company has expanded this business a lot in the past year with a 407% increase in loans disbursed under postpaid, 1100% increase in the number of personal loans and 40% increase in the number of business loans.

The management says that the people who opt for Postpaid and have a positive experience are the ones who go on to take personal loans. The business loans are given to small merchants who accept payments through Paytm.

They were affected by Covid in the past year and that is why the growth number does not look very impressive. But these loans have a high repeatability and stickiness.

The company received about 79-88 Cr from their lending platform during Q3 FY22. As of Q3, the company has 2.5 Cr merchants on their platform, and they disbursed about 35,000 loans during the quarter. So their current penetration for

merchant loans is 0.14% But if we assume that the penetration goes up to 0.5%, that is 0.5% of the merchants on their platform take a merchant loan, the revenues could be 76-88 Cr from merchant loans alone.

Take a look at the table to see how much revenue the company can earn as the penetration for merchant loans increases on their platform.

7. Payments Bank

The company has a payments bank which is one of their only profitable businesses. The Payments Bank is not consolidated in their books. Vijay Shekhar Sharma owns 51% of the payments bank and the company owns the other 49%.

The company has a payments bank which is one of their only profitable businesses. The Payments Bank is not consolidated in their books. Vijay Shekhar Sharma owns 51% of the payments bank and the company owns the other 49%.

Paytm payments bank provides services such as current account, savings account, salary account, fixed deposit and debit card. 56% of the merchants on their platform have a Payments bank account which is a huge captive consumer base.

In March 2022, Paytm Payments bank received an order from the RBI to stop onboarding new customers. This is not the first time the bank has had regulatory issues. Management has said that they would apply for a small finance bank license in May 2022

when the Payments bank completes 5 years. It is unlikely that the RBI will grant the license as more than 30% of the equity of the parent company is owned by Chinese entities.

8. Major Issues

The company also has a lot of issues in terms of how the business is run. First off, they have a very complicated corporate structure. They have a total of 15 subsidiaries - 15 domestic and 17 foreign. The way they account for them are also different.

The company also has a lot of issues in terms of how the business is run. First off, they have a very complicated corporate structure. They have a total of 15 subsidiaries - 15 domestic and 17 foreign. The way they account for them are also different.

They consolidate some of the entities and they do not consolidate some others. So it becomes very difficult to understand if the company is hiding any liabilities off the balance sheet. The other issue with the company is that it is one of the largest issuers of ESOPs.

They currently have 65 crores of shares outstanding but they also have an ESOP pool of 4.5 Cr. So with full dilution, it would take the number of shares to 69.5 Cr which results in significant dilution to the shareholders.

In 2021, the company issued 2.75 crore ESOPs, of which 77% went to Vijay Shekhar Sharma. The exercise price of these ESOPs were 9 rupees per share whereas the IPO price was 2150 per share.

Management has also indicated that a quarterly ESOP cost of 380 Cr will continue for the next 4-5 years. Although this is a non-cash expense, it seems like the company will not be profitable at a PAT level till then.

9. Risks

One of the biggest risks is that the company still has the start-up mentality where they are burning huge amounts of cash with no clear path to profitability. The management has indicated that they will be profitable at a Pre-ESOP EBITDA level in 6 quarters, but there

One of the biggest risks is that the company still has the start-up mentality where they are burning huge amounts of cash with no clear path to profitability. The management has indicated that they will be profitable at a Pre-ESOP EBITDA level in 6 quarters, but there

is no indication as to when it will be profitable at a PAT level. We also don't understand how to value the company currently. Clearly the business has a potential for huge operating leverage, but such tech companies are entering into the markets for the first time.

In the absence of earnings or EBITDA, what metric could be used to value the company. The stock seems to be overvalued by all metrics for a company that has no plans to show positive earnings for the next 5-6 years.

• • •

Missing some Tweet in this thread? You can try to

force a refresh