📣 Breaking: @CMSGov releases January 2022 enrollment report: Medicaid/CHIP now cover ~87 million Americans, or 26% of the total U.S. population:

acasignups.net/22/04/28/cms-r…

acasignups.net/22/04/28/cms-r…

Another 64.2 million Americans are now enrolled in Medicare...45% of whom are now enrolled in privately-administered Medicare Advantage plans, for good or for bad. That's over 19% of the U.S. population.

11.9M of these are dual-eligibles (counted as part of both programs), so combined that's around 139.3 million, or ~41.6% of the total U.S. population enrolled in Medicare, Medicaid or CHIP.

Add to this ~13 million enrolled in effectuated #ACA exchange plans & ~1 million enrolled in ACA Basic Health Plans, and that's > 153 million, or ~45.7% of the total U.S. population receiving their healthcare coverage via government-run or directly government-subsidized programs.

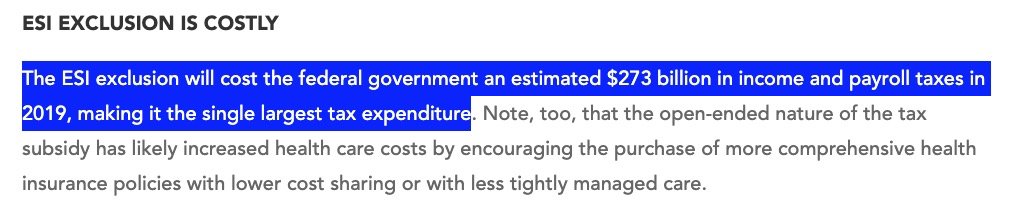

NOTE: I say "directly" subsidized because ANOTHER ~45% or so of the U.S. population is enrolled in EMPLOYER-BASED coverage, which is *indirectly* subsidized in the form of the federal income & payroll tax exclusion.

taxpolicycenter.org/briefing-book/…

taxpolicycenter.org/briefing-book/…

In other words, for those claiming that they don't want "The Gub'mint" subsidizing their healthcare coverage, I have some bad news for you: It's been doing that to some extent for the vast majority of the population for decades, even before the ACA came around.

I'm not sure how self-insured corporations play into this and there's likely plenty of other caveats/etc, but $273B / ~154M = an average "subsidy" of ~$1,770/year per employer-sponsored enrollee.

Also, if you're covered via your employer, they likely pay upwards of 60-70% of your premiums! This is technically part of your compensation, but still.

Here's how to see how much of YOUR employer-based health insurance is being paid for by your employer:

acasignups.net/22/04/28/quick…

Here's how to see how much of YOUR employer-based health insurance is being paid for by your employer:

acasignups.net/22/04/28/quick…

In other words, if you're single & earn $50K/yr + an employer health policy costing $7,200/yr, you're likely only paying ~$1,200 of it yourself, w/your employer picking up the other $6,000.

Technically, you're earning $57,200/year but only paying taxes on $50,000 of it.

Technically, you're earning $57,200/year but only paying taxes on $50,000 of it.

• • •

Missing some Tweet in this thread? You can try to

force a refresh