Prices send signals to both supply and demand like a ringing phone. One of the two typically pick up. For many reasons, supply is not available, but the phone is still ringing, sooner or later demand has to answer. #OOTT

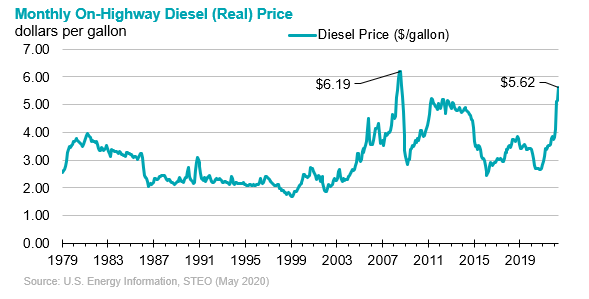

U.S. on-highway diesel prices are crazy high on a nominal basis, but we've still got a ways to go before we match the highest real prices from 2008.

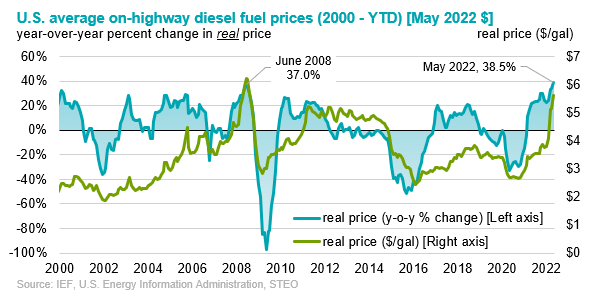

This is key, the year-over-year change in real diesel prices this time around is higher than it was back in 2008... But that's comparing peak 2008 to now, we still don't know when diesel prices will come down.

• • •

Missing some Tweet in this thread? You can try to

force a refresh