Quite some info here on @VirginOrbit and #launcherone to feed the never ending saga of launch costs reduction. Is it happening? is it supporting the 'smallsat revolution'? is it 'democratising' space and making it 'accessible to everyone'? 1/

https://twitter.com/pbdes/status/1524785266296242177

First we read that the January 2022 launch yielded 2.1M$. With a total mass launched of less than 30kg, for 6 cubesats deployed (according to @planet4589 here: planet4589.org/space/gcat/dat…) that is a whopping >70k$/kg to orbit. Hardly a bargain. 2/

If that weren't enough, even at that price $VORB state they can't cover their costs for the next launches “It is probable for five of these launch service agreements that the costs to provide the service will exceed the firm fixed price of each launch” @VirginOrbit says 3/

As a result @VirginOrbit announces that it will increase its price to 6-12M$/launch. At 12M$ and assuming an optimistic max fill rate of 500kg the price/would be 24k$/kg. But is this fill rate even achievable? (max fill is seldom achieved, see here

https://twitter.com/LionnetPierre/status/1433536407625035781) 4/

Now I ask myself: why was the January 2022 launch so badly filled? Why would a rocket launch at less than 10% of its capacity? Particularly considering the usual narrative of 'there is a huge demand pipeline for small satellite launch', is it that hard to find passengers? 5/

I discussed this same exact point a while ago regarding the @RocketLab launch with @BlackSky_Inc (

https://twitter.com/LionnetPierre/status/1425074169599889414) and the comments ensuing suggested a limitation due to the fairing volume. Fair enough. 6/

However it is hard to believe that fairing volume limitations prevented a better fill rate for the #launcherone launch of January last. Then I am back to my initial interrogation: where is the demand? 7/

And looking at upcoming $VORB best possible prices to orbit of 12 to 24k$/kg I don't see how they can still consider their service to be "affordable". And their price structure seems ill designed to stimulate a "rapidly growing industry". 8/

But if the new players in space launch are not more 'affordable' than the established players, what exactly is their added value to the space sector? How can we expect launch demand to grow if operators are confronted to increasing launch prices instead of decreasing ones? 9/

In this thread on launch prices (

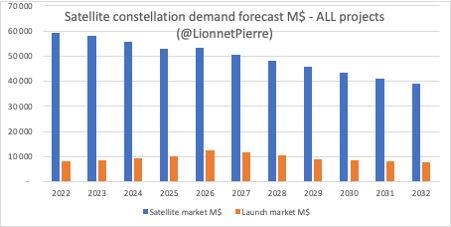

https://twitter.com/LionnetPierre/status/1430497863306465286) I have explained what I believe is the real situation of launch prices and how, despite their significant reduction in past decades, they did not translate into growing demand, but a shrinking market value instead. 10/

In this other thread on megaconstellations economics (

https://twitter.com/LionnetPierre/status/1448677218566250501) I suggest that the "right" launch price threshold to unlock a massive launch demand growth (mostly for smallsats) is probably somewhere between 1 and 2k$/kg, and definitely well below 5k$/kg. 11/

I am afraid that with @VirginOrbit we are not getting any closer to an 'affordable' space launch supply. Regretfully we can say that much of other new launch suppliers (@RocketLab or @Astra e.g.). 12/end

• • •

Missing some Tweet in this thread? You can try to

force a refresh