Detailed Analysis on the business of #SRF Ltd 🧪🧪 - A journey of aggressive capital allocation

CMP - ₹2267

Like and retweet for maximum reach!!

CMP - ₹2267

Like and retweet for maximum reach!!

1. COMPANY OVERVIEW

The company was first incorporated in 1970 by the name Shri Ram Fibres Limited by DCM limited as a wholly owned subsidiary. They set up their first manufacturing facility in Manali, near Chennai in 1973 with initial focus on the manufacturing of tyre cord

The company was first incorporated in 1970 by the name Shri Ram Fibres Limited by DCM limited as a wholly owned subsidiary. They set up their first manufacturing facility in Manali, near Chennai in 1973 with initial focus on the manufacturing of tyre cord

fabrics(TCF). The company entered the chemicals business in 1989 by beginning the production of refrigerant gases and renamed itself as SRF ltd in 1990.The company’s product portfolio now consists of specialty fluorochemicals, refrigerant gases, nylon and polyester tyre cord

fibres, laminated and coated fabrics, packaging films like BOPP and BOPET and has 11 manufacturing facilities spread across India, Thailand, Hungary and South Africa

2. BUSINESS VERTICALS

The image below summarizes the business segments of SRF:

2. BUSINESS VERTICALS

The image below summarizes the business segments of SRF:

SRF is the largest manufacturer of technical textiles in India. The products under this business consists of nylon and polyester tyre cord fabrics, belting fabrics and industrial yarn. The Chemicals business portfolio consists of Specialty Chemicals, Refrigerant gases and

Chloromethanes and the upcoming fluoropolymers. The specialty chemicals made by the company have major end-use in the agrochemical industry. The company makes a wide variety of refrigerant gases and has the widest portfolio of refrigerant gases in India. In Packaging films, the

company has products like biaxially oriented polypropylene(BOPP) and biaxially oriented polyethylene terephthalate(BOPET) and it has recently entered into aluminium foil packaging. The Other business has products like laminated and coated fabrics which earlier used to be

classified under the technical textiles business

The image below summarizes the business segment wise revenue split for SRF:

The image below summarizes the business segment wise revenue split for SRF:

As technical textiles is a business which is characterised by a flat growth profile, the company decided to focus more on its chemicals and packaging business. The results of this focus can be seen from the chart in the image above where the company right now is earning major

revenues from the chemicals and packaging business and the contribution of technical textiles business has decreased over time from 24% in FY19 to 17% in FY22

3. VALUE CHAIN

As you can see from the value chain of SRF in the image below, the company produces a wide variety of

3. VALUE CHAIN

As you can see from the value chain of SRF in the image below, the company produces a wide variety of

chloromethanes such as Chloroform, Methylene Dichloride, Perchloroethylene and Trichloroethylene which go into manufacturing of a wide variety of refrigerant gases and HFC blends. The company recently commissioned it’s chloromethane capacity on 7 November 2022 in Dahej which has

taken the total chloromethanes capacity of the company to 1,90,000 MTPA which is the largest in India

Trichloroethylene acts as a backward integration to the HFC-134a production facility and is used primarily as a feedstock. Perchloroethylene is used as a solvent in the laundry,

Trichloroethylene acts as a backward integration to the HFC-134a production facility and is used primarily as a feedstock. Perchloroethylene is used as a solvent in the laundry,

metal degreasing and vapour degreasing industries. It is also a feedstock for HFC-125 and HFC-134a for some producers. There is no domestic producer of perchloroethylene with the major demand being met through imports

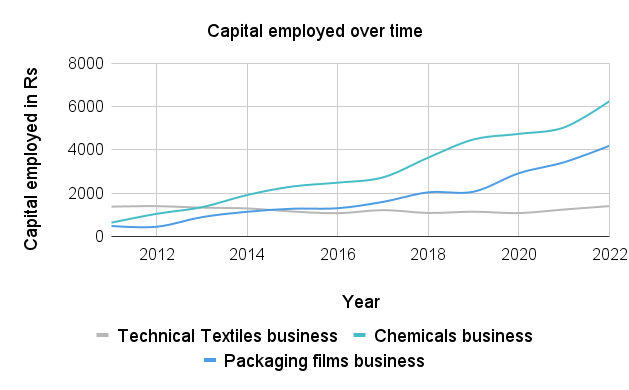

4. CAPITAL ALLOCATION STRATEGY

The company management in 2011-12 decided to shift its focus towards the chemicals & packaging business from the technical textiles business as they witnessed a stagnant growth in technical textiles business. Technical textiles business was a cash

The company management in 2011-12 decided to shift its focus towards the chemicals & packaging business from the technical textiles business as they witnessed a stagnant growth in technical textiles business. Technical textiles business was a cash

cow for the company and the cash generated from this business was used towards the development of the chemicals and packaging business. The capital allocation done by the company is summarized in the image below:

As seen from the image below, the capital employed in the technical textiles business has mostly remained flat while the capital allocation for the chemicals and packaging business has increased over the years

SRF has done capacity expansions in Dahej for the manufacturing of both agrochemical intermediates and active ingredients in the last decade. The images below show the presence of SRF in the Agro CRAMS Value Chain and how SRF has done investments towards the agro side over time

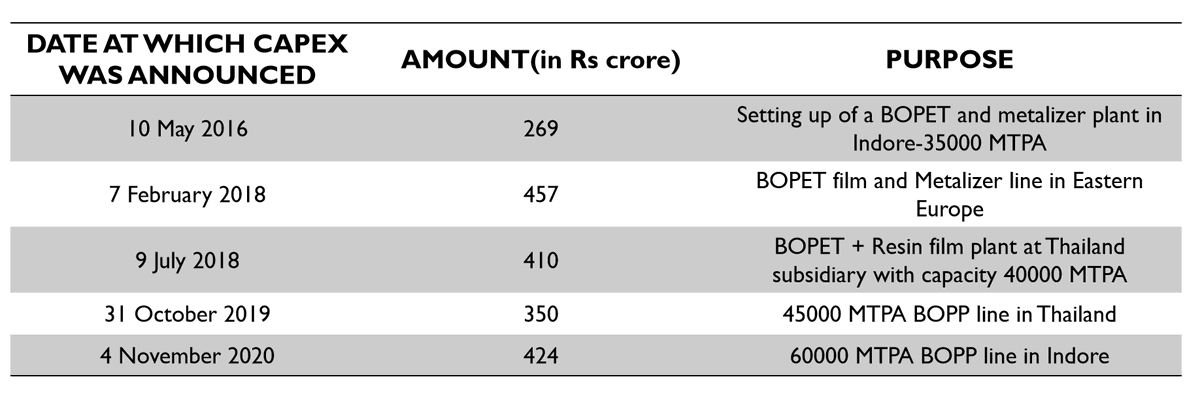

SRF has done capacity expansion on both the BOPP and BOPET side for developing their Packaging films business and has recently entered into aluminium foil packaging. The image below shows the capacity expansions done by the company on this side:

5. FUTURE OUTLOOK

i. CRAMS AND SPECIALTY FLUOROCHEMICALS

The company announced a capex for an MPP4 plant at Dahej at a cost of Rs 375 crores.The company is planning to make 5 to 6 products out of this plant

The company made an investment of Rs 190 crores in 2021 for a Pharma

i. CRAMS AND SPECIALTY FLUOROCHEMICALS

The company announced a capex for an MPP4 plant at Dahej at a cost of Rs 375 crores.The company is planning to make 5 to 6 products out of this plant

The company made an investment of Rs 190 crores in 2021 for a Pharma

Intermediates plant (PIP) which will help strengthen the pharma capabilities of the company along with a Rs 61 crore investment for a dedicated facility which will be used for the manufacturing of a key agrochemical product. The company expects the PIP plant to come online in

Q4FY23 as mentioned in their Q1FY23 concall

The board has approved a capex of Rs 400 crores for a number of projects at Dahej as mentioned in their Q1FY23 concall. The breakup of this capex is as follows:

a. Rs 250 crore will be used to set up a dedicated facility for production of an advanced agrochemical intermediate to

a. Rs 250 crore will be used to set up a dedicated facility for production of an advanced agrochemical intermediate to

meet the growing demand in the future.The capacity of this product is 1000 MTPA.The capacity is expected to come online in the next eight to ten months

b. Rs 72 crores will be used for capacity expansion of an intermediate product.This product is a key building block which finds

b. Rs 72 crores will be used for capacity expansion of an intermediate product.This product is a key building block which finds

applications in both pharmaceuticals and agrochemicals

c. The remaining capex is for the development of various agrochemical products which help the company to cater to the increasing demand in the future

The MPP4 plant at Dahej has been commissioned and the company is planning

c. The remaining capex is for the development of various agrochemical products which help the company to cater to the increasing demand in the future

The MPP4 plant at Dahej has been commissioned and the company is planning

to ramp-up the facility. The board has approved a capex of Rs 604 crore for 4 new agrochemical plants. This capacity expansion will happen at Dahej.The products in these plants are precursors to some of the existing AIs of the company. The company manufactures precursors for some

of their AIs, so this project plans to expand the margins of the company. The company plans to add an additional capacity of around 4000 MTPA as a part of this Rs 604 crore capex and this capacity is estimated to come online in the next 10-12 months. The company plans to fund

this capex with a mix of debt and internal accruals

The board has also approved a project for the development of a Kilo-lab facility in Bhiwadi, Rajasthan which has an estimated outlay of Rs 9.8 crore. This lab will cater to the needs of the pharma market

The company has incurred a capex of Rs 1250 crore in H1FY23. The company plans to incur a total capex of Rs 3000 crore for this year which is the part of the company’ s long-term capex plan of Rs 15000 crore for the next 3-5 years

ii. FLUOROPOLYMERS

SRF announced a capex of Rs 424 crore to set up a manufacturing facility for PTFE along with R-22 which acts as the backward integration for PTFE. The company plans to be cost competitive to GFL by doing this backward integration. The company plans to

SRF announced a capex of Rs 424 crore to set up a manufacturing facility for PTFE along with R-22 which acts as the backward integration for PTFE. The company plans to be cost competitive to GFL by doing this backward integration. The company plans to

manufacture 4 grades initially out of which 2 will be commodity grade and the remaining will be specialty grade.

The company plans to commercialize their new PTFE plant in Q3FY23 and once they have approvals for their products, they plan to begin supplying from Q4FY23

The company plans to commercialize their new PTFE plant in Q3FY23 and once they have approvals for their products, they plan to begin supplying from Q4FY23

The company also has plans to enter other fluoropolymers like PVDF and FKM which find applications in Lithium ion batteries and semiconductors. It will face tough competition from GFL in Indian market and other fluoropolymer players in the foreign market who already have a wide

portfolio of fluoropolymers. The fluoropolymer business is a high entry barrier business as it takes time to develop the technology and the level of forward and backward integration required to get a low cost structure required in fluoropolymer production

iii. PACKAGING BUSINESS

The industry margins for BOPET declined due to new capacities which came online globally. The company took a hit on their margins due to the rising power cost in Hungary and the correction in commodity prices. There was a partial offset from a sustained

The industry margins for BOPET declined due to new capacities which came online globally. The company took a hit on their margins due to the rising power cost in Hungary and the correction in commodity prices. There was a partial offset from a sustained

demand on the BOPP side however. The company commissioned a new BOPP line in Indore in this Q2FY23

The Hungary plant made an EBITDA €8 to €9 million in FY22 and the company was planning to ramp-up the plant but due to the rising power cost in Hungary, they delayed their plans and are now the production in this plant is taking place only to the extent to the probability of

getting orders at good prices

BOPP as a product is 3x the size of BOPET. It has a large value added product portfolio as compared to BOPET and there has been a discussion for use of mono family structure polymers which will increase the demand for BOPP as compared to BOPET going forward

The aluminium foil project which is part of the Packaging Films Business of the company is on track and is expected to come online in September 2023

Check out the New Year Offer on the Micro Cap Club membership:

bit.ly/3zYY8OS

bit.ly/3zYY8OS

• • •

Missing some Tweet in this thread? You can try to

force a refresh