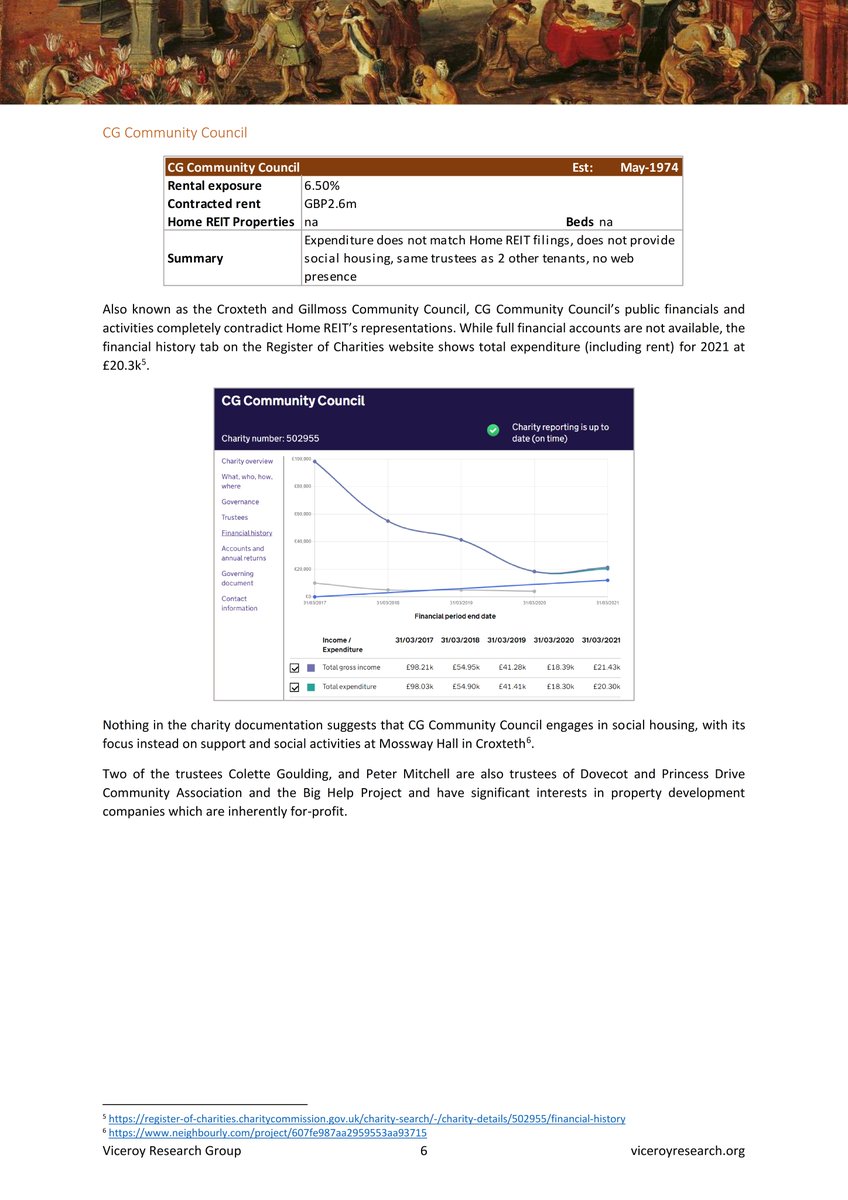

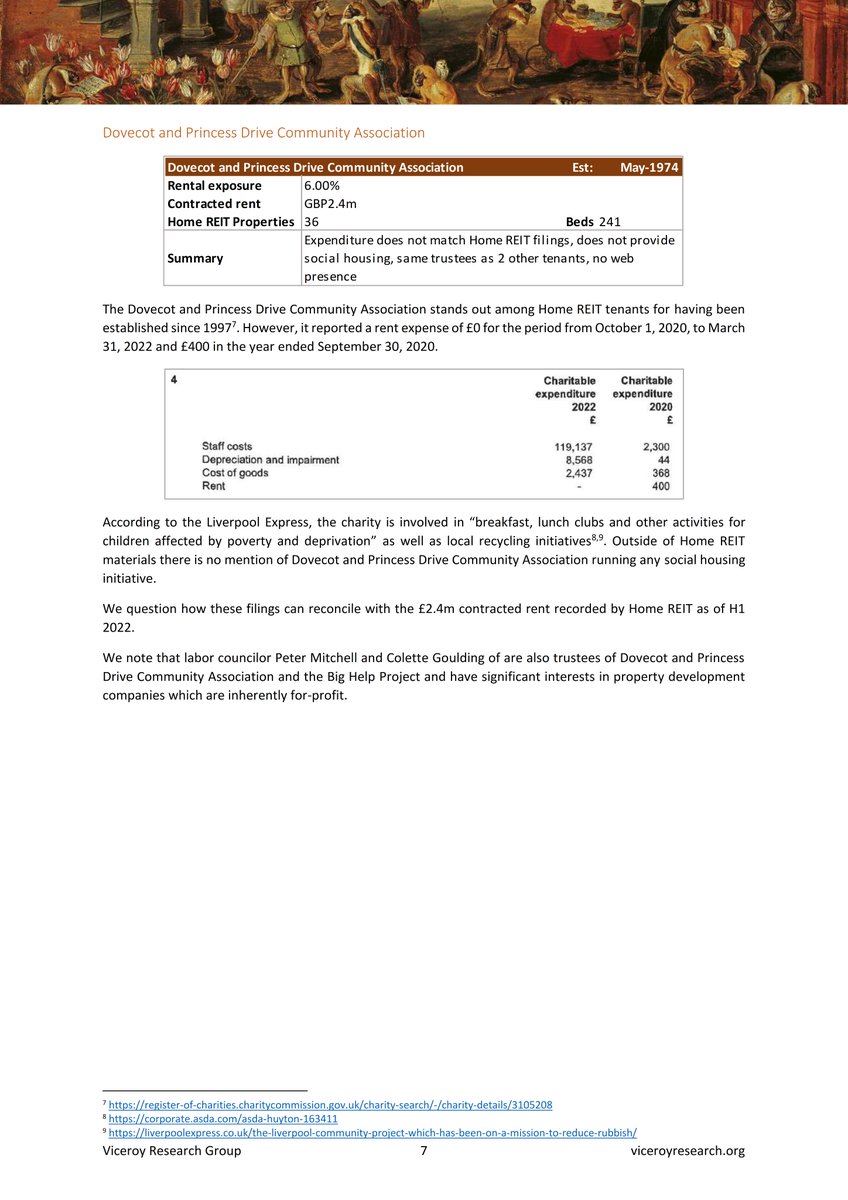

SALT LAKE CITY PORTFOLIO

$MPW plainly overpaid an estimated $700m for a portfolio of properties from Steward. It financed Stewards entire purchase of a larger portfolio, and extinguished the entire loan in return for a fraction of the properties. 1/

$MPW plainly overpaid an estimated $700m for a portfolio of properties from Steward. It financed Stewards entire purchase of a larger portfolio, and extinguished the entire loan in return for a fraction of the properties. 1/

In 2017, $MPW loaned Steward $1.4b to purchase a Salt Lake City Hospital operator IASIS and their portfolio of 19 hospitals. It also made a further $100m minority interest equity contribution in the transaction. IASIS owned and operated 17 hospitals. 2/

A $700m portion of this loan was immediately extinguished in exchange for 9 properties.

The remaining $700m was a mortgage loan against 2 unnamed properties: Jordan Valley Medical Center and Davis Hospital & Medical Center. $MPW 3/

The remaining $700m was a mortgage loan against 2 unnamed properties: Jordan Valley Medical Center and Davis Hospital & Medical Center. $MPW 3/

On July 8, 2020, $MPW acquired the Jordan Valley Medical Center and Davis Hospital & Medical Center in exchange for a total extinguishment of the loan and an additional $200m cash payment it labelled a fair value increase. 4/

The first $700m loan was exchanged for 9 properties, and the second $700m loan was secured against a further 2, but Iasis owned and operated 18 facilities in total at the time of acqusition. Steward basically received 7 of them for free. $MPW 5/

Steward ultimately tried offloading this operations portfolio to HCA Healthcare, but was blocked by the FTC. It is now holding the bag. $MPW 6/6

• • •

Missing some Tweet in this thread? You can try to

force a refresh