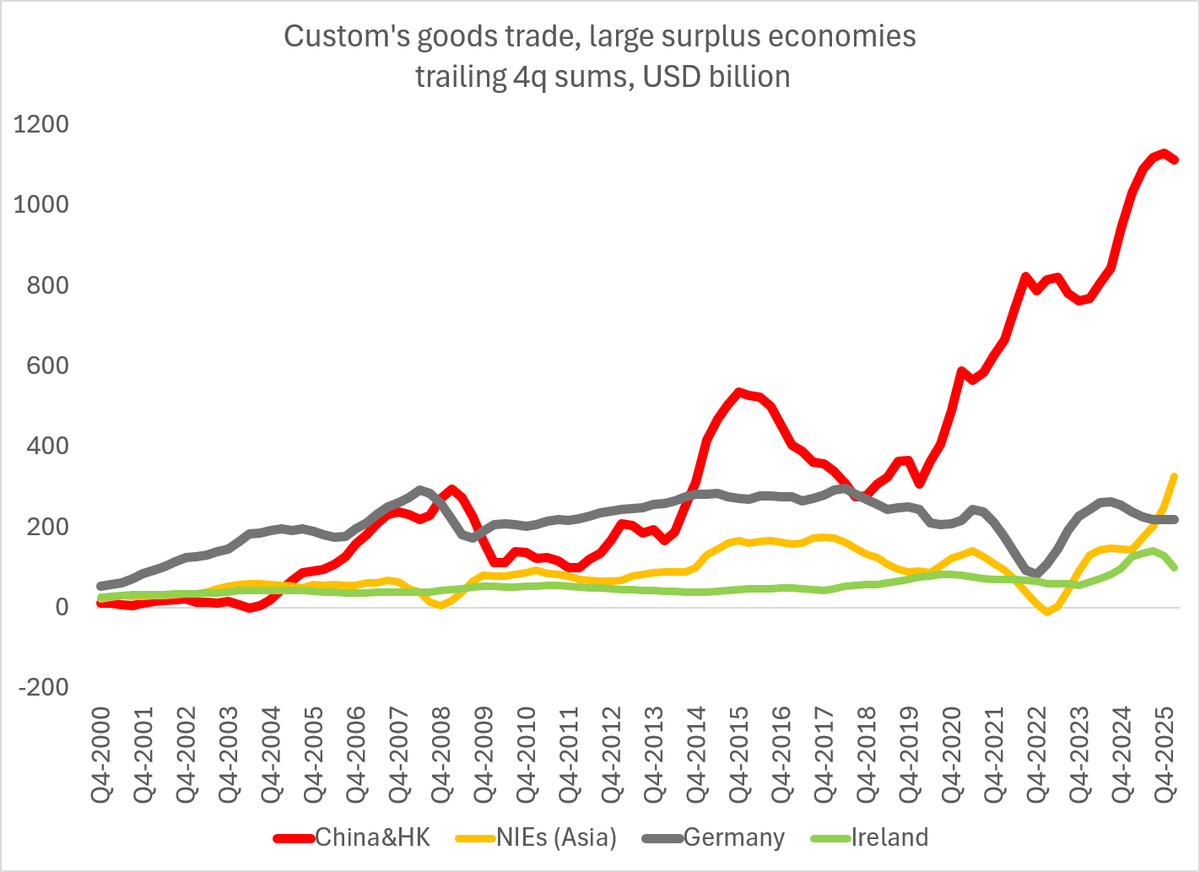

Excellent essay. No doubt one of the defining features of the China shock has been how it has reallocated the global surplus.

The old exportweltmeister has been dethroned -- and China has world scale in advanced manufacturing, which is new and disruptive

1/

The old exportweltmeister has been dethroned -- and China has world scale in advanced manufacturing, which is new and disruptive

1/

https://twitter.com/adam_tooze/status/2071204022070255802

The jump in China's surplus since the start of 2024 is actually understated in dollar terms -- as Chinese export prices have fallen/ volume metrics show a bigger rise. But there has been a huge shift since 2018

2/

2/

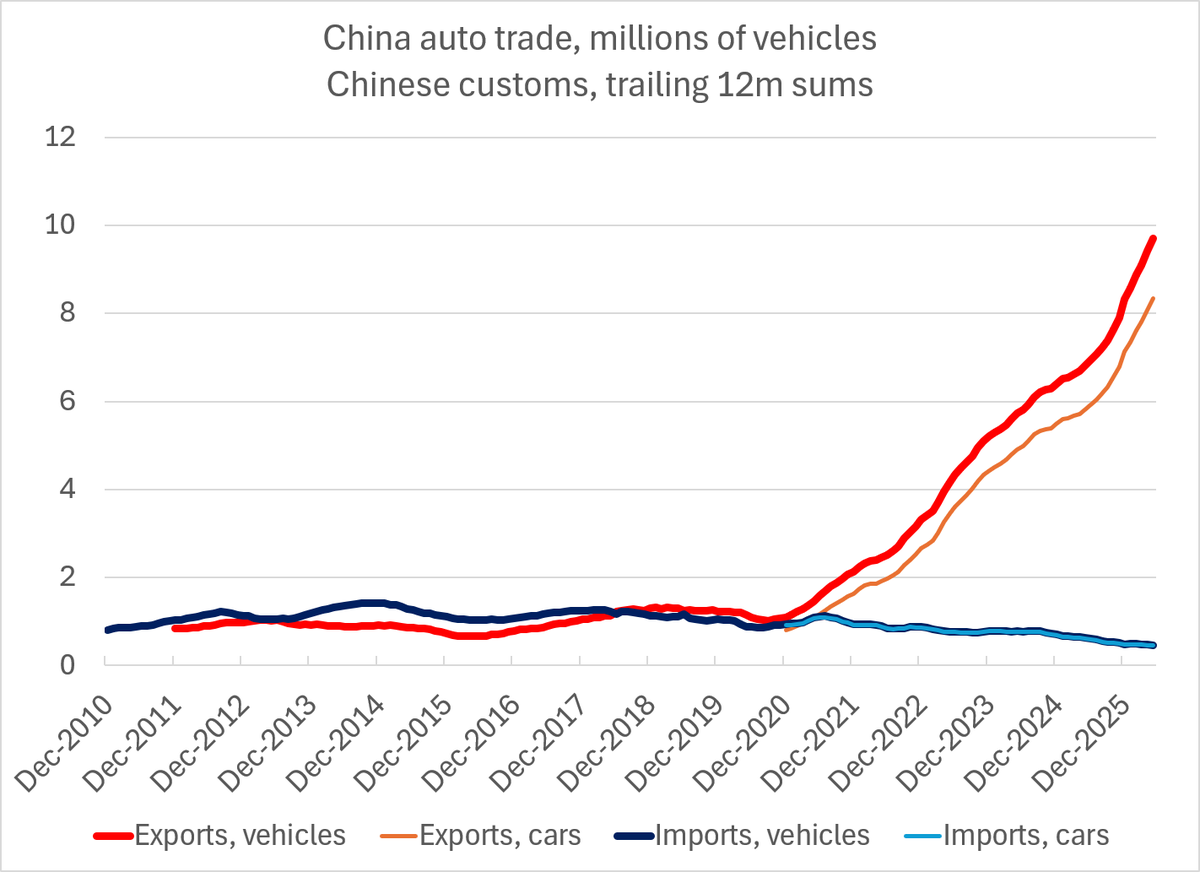

I do think I was among the first to talk of a second China shock -- I was among the first to notice the acceleration in China's auto exports, and I also observed that the rise in China's surplus in manufacturing after 19 was as big as the rise after WTO accession

3/

3/

Everything always looks different when scaled to Chinese GDP -- but it is worth recalling that China's surplus in manufactures was 3-4% of its GDP before WTO accession (and RMB real depreciation). It is back at its pre GFC highs (with much lower levels of imports)

4/

4/

These are profound shits in the global economy (And the distribution of global manufacturing production/ engineering & technical skill). East Asia's surplus is two times its 1980s peak, mostly b/c of China (Korea will have a bigger impact on the 26 numbers)

5/

5/

I do have a few additional technical points in response to Adam's sweeping story telling --

I would put a bit more emphasis on the fall in Chinese export prices after 22 (and after 23, which is tied to the currency move/ recent rise is all chips)

6/

I would put a bit more emphasis on the fall in Chinese export prices after 22 (and after 23, which is tied to the currency move/ recent rise is all chips)

6/

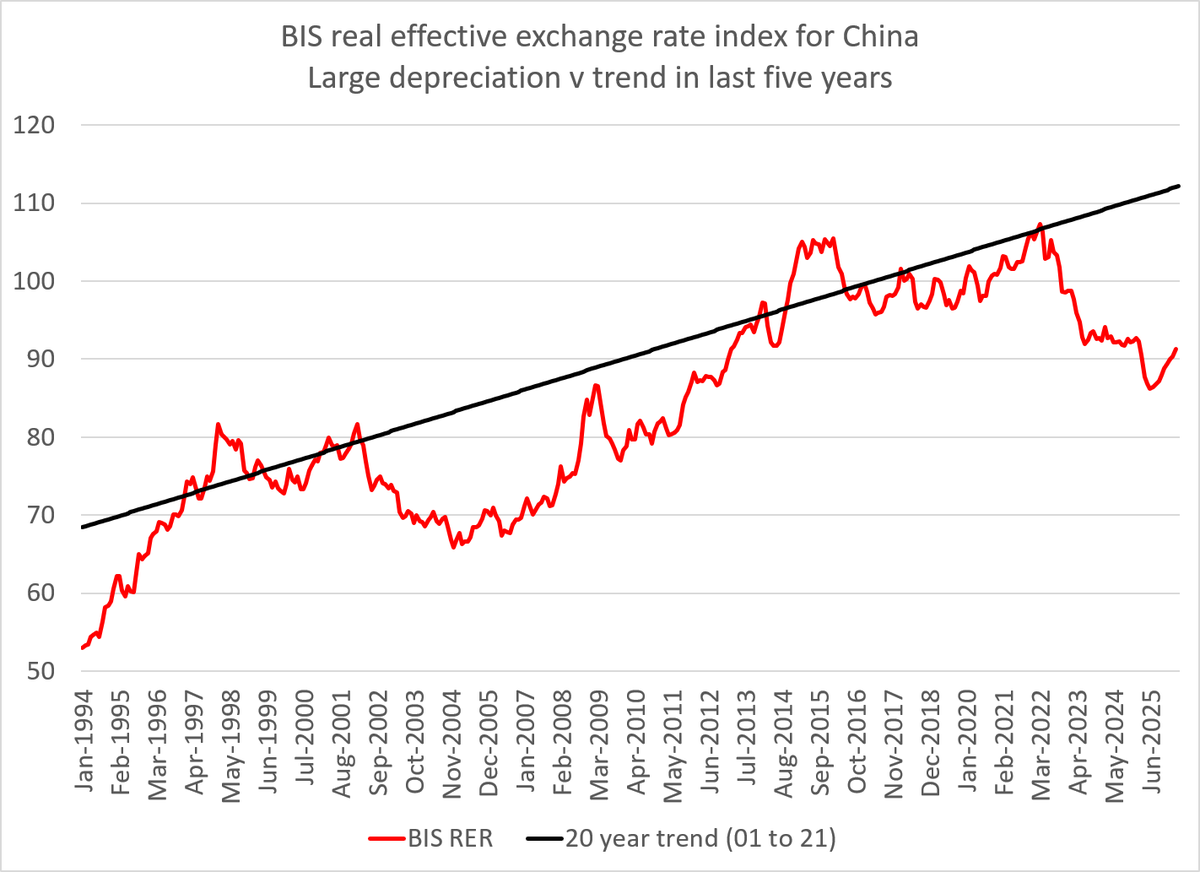

when assessing the balance between industrial policies & currency policy in explaining China's 24/25 export success (net exports added 3 pp to growth, export volumes were 2x global trade) I would put a bit more emphasis on the exchange rate (the 15% move = 2 pp on NX)

7/

7/

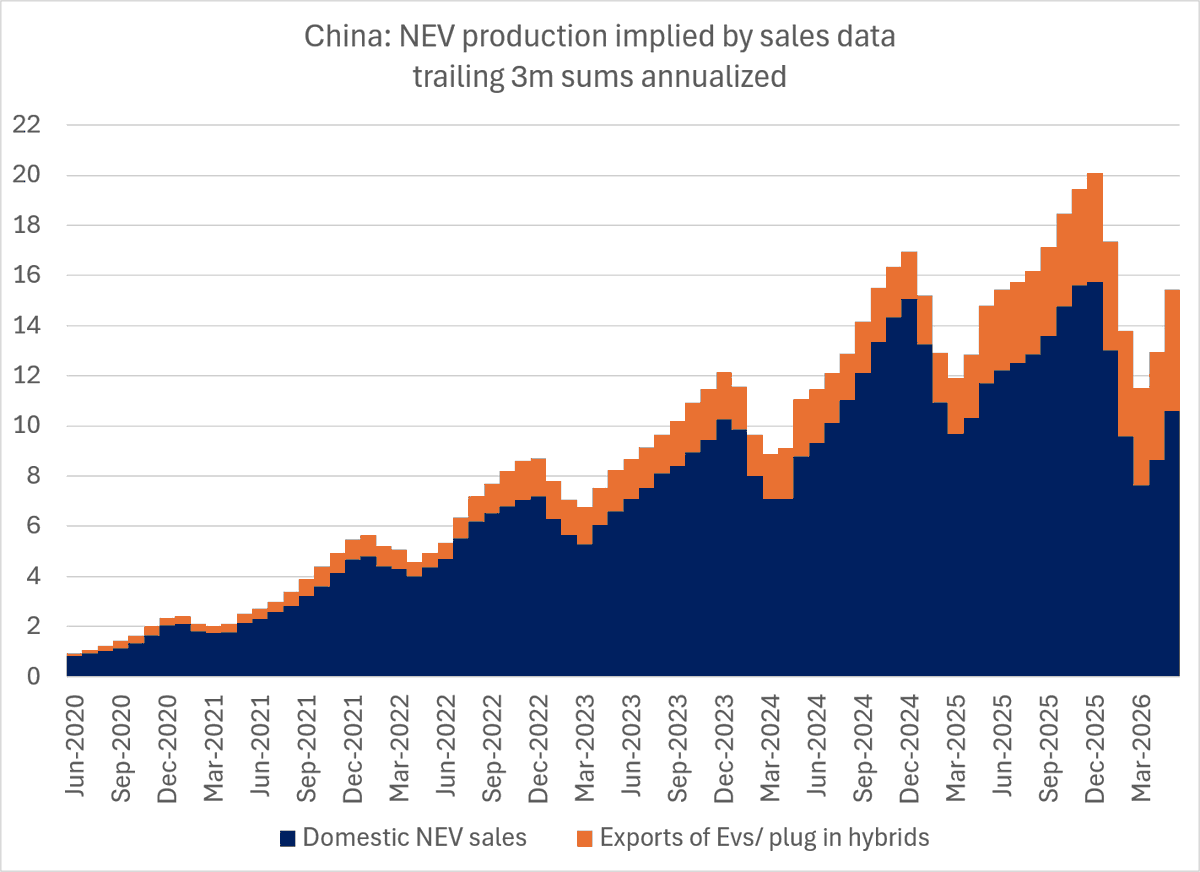

and I would put a bit more emphasis on the fall in auto demand inside China as a driver of China's current export wave -- domestic EV sales were down y/y in 3ms through May and way below the peaks of last fall

8/

8/

And domestic auto sales have peaked it seems and are now trending down.

That includes EV sales over the last 12ms (may change going forward)

9/

That includes EV sales over the last 12ms (may change going forward)

9/

But it is hard not to share Tooze's sense of wonder at the pace of China's industrial transformation. Going from producing 1-2m EVs a year to producing 20m EVs a year in 5 years is an achievement

10/

adamtooze.substack.com/p/chartbook-45…

10/

adamtooze.substack.com/p/chartbook-45…

At the same time China's industrial scale poses a profound challenge to the entire global economy -- most obviously the old mercantilist powers, but ultimately to every manufacturing economy

11/

11/

Consider the following:

China can now make 25m EVs (probably more) + is still investing in new capacity, and can produce ~ 50m total cars of all kinds. Its domestic market is falling back to 20m. It is now exporting 10m a year -- but has the capacity to export a lot more

12/

China can now make 25m EVs (probably more) + is still investing in new capacity, and can produce ~ 50m total cars of all kinds. Its domestic market is falling back to 20m. It is now exporting 10m a year -- but has the capacity to export a lot more

12/

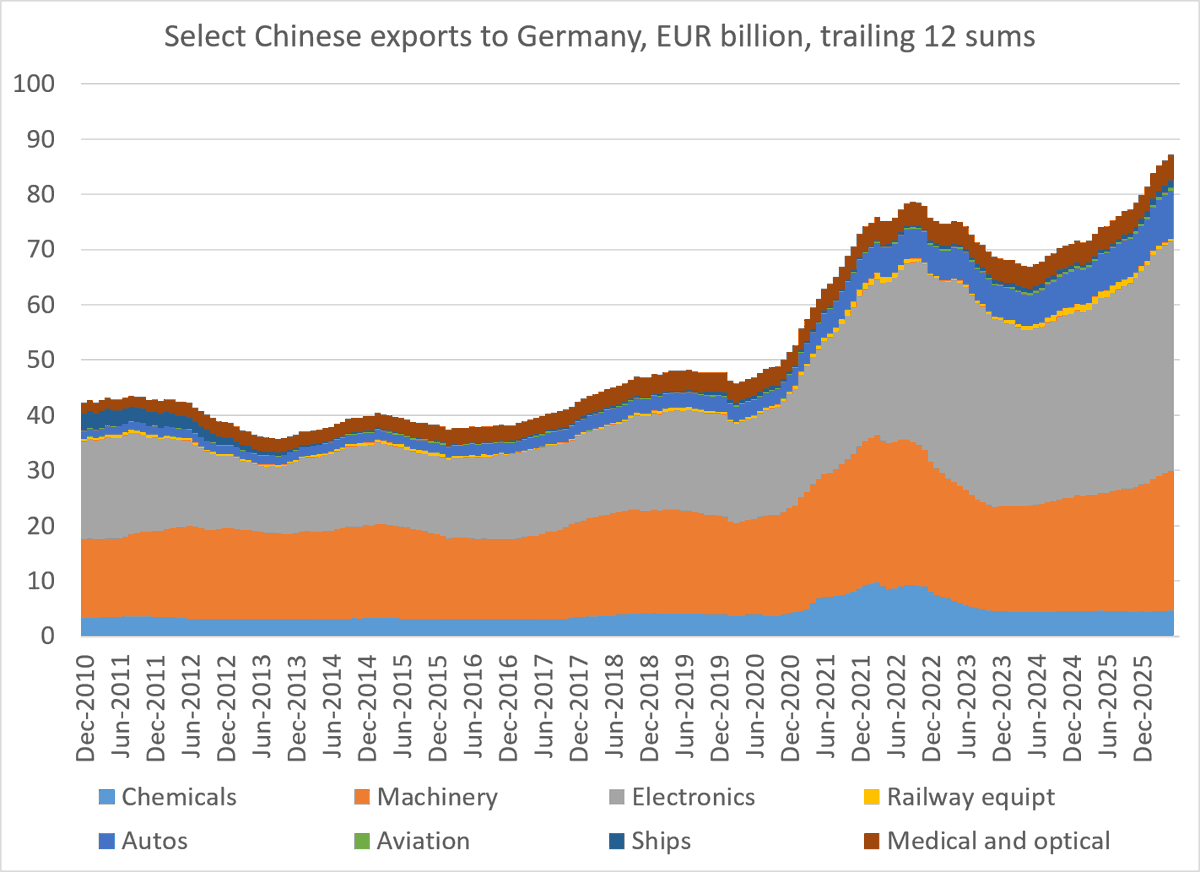

And, as the Suddeutsche Zeitung emphasized, China now has that kind of scale across most of the mechanical engineering sector, and of course aspires to similar scale in commercial aviation

13/

sueddeutsche.de/projekte/artik…

13/

sueddeutsche.de/projekte/artik…

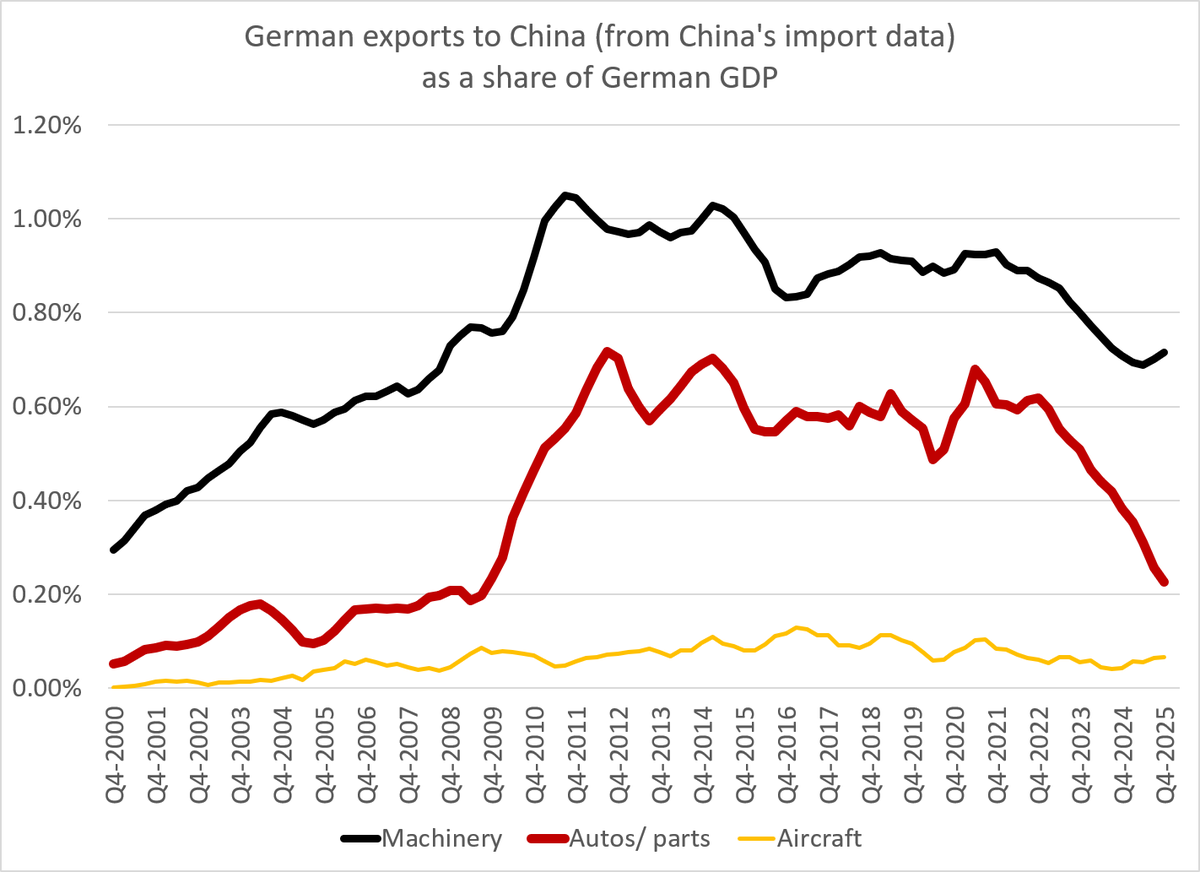

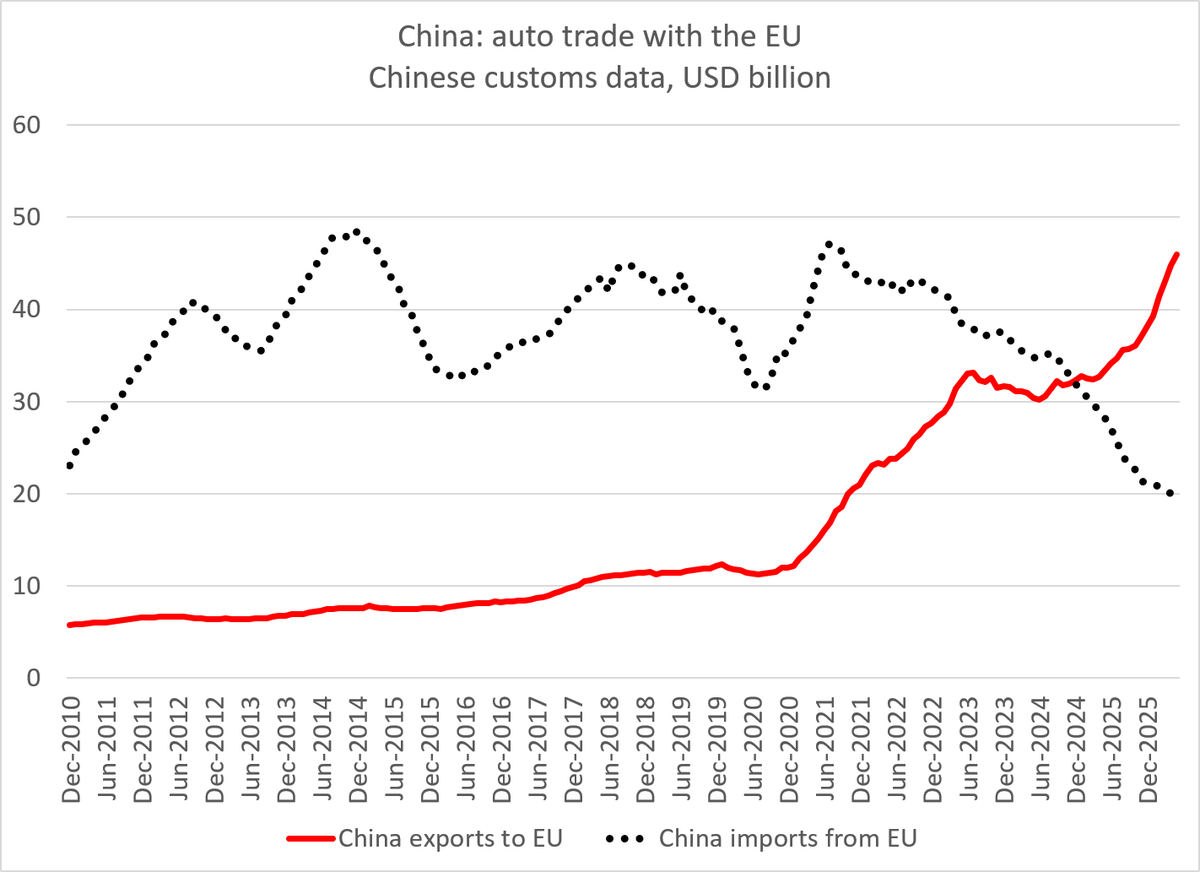

The rise in Chinese exports to Germany in core industrial sectors over the last 6 years hasn't primarily been driven by autos (the auto impact is stronger in the broad EA/ EU data)

14/

14/

Tooze has some doubts that exchange rate moves are the solution -- he echoes the views of the central bank establishment that appreciation would make China's deflation worse ...

15/

15/

I tend to think that currency appreciation is far easier than trying to negotiate changes to China's domestic industrial policies/ subsidies and/or social spending -- appreciation was part of the solution to the first China shock after all

16/

16/

There isn't any evidence that changes in the exchange rate have changed the pace of Chinese deflation in recent years -- so I don't think any nominal appreciation would be fully offset (tho the price changes make it harder to generate a big real appreciation)

17/

17/

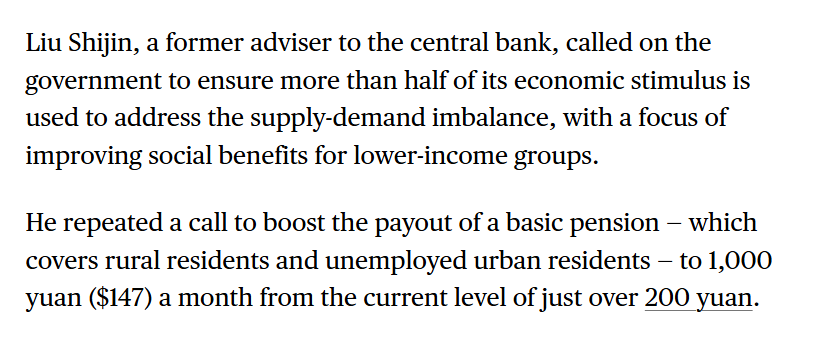

And there is ample room for China to respond to less growth from net exports with more social spending. Like this idea for example

18/ bloomberg.com/news/articles/…

18/ bloomberg.com/news/articles/…

Tooze as usual is unsurpassed at putting policy debates in a broader historical and social context

19/

adamtooze.substack.com/p/chartbook-45…

19/

adamtooze.substack.com/p/chartbook-45…

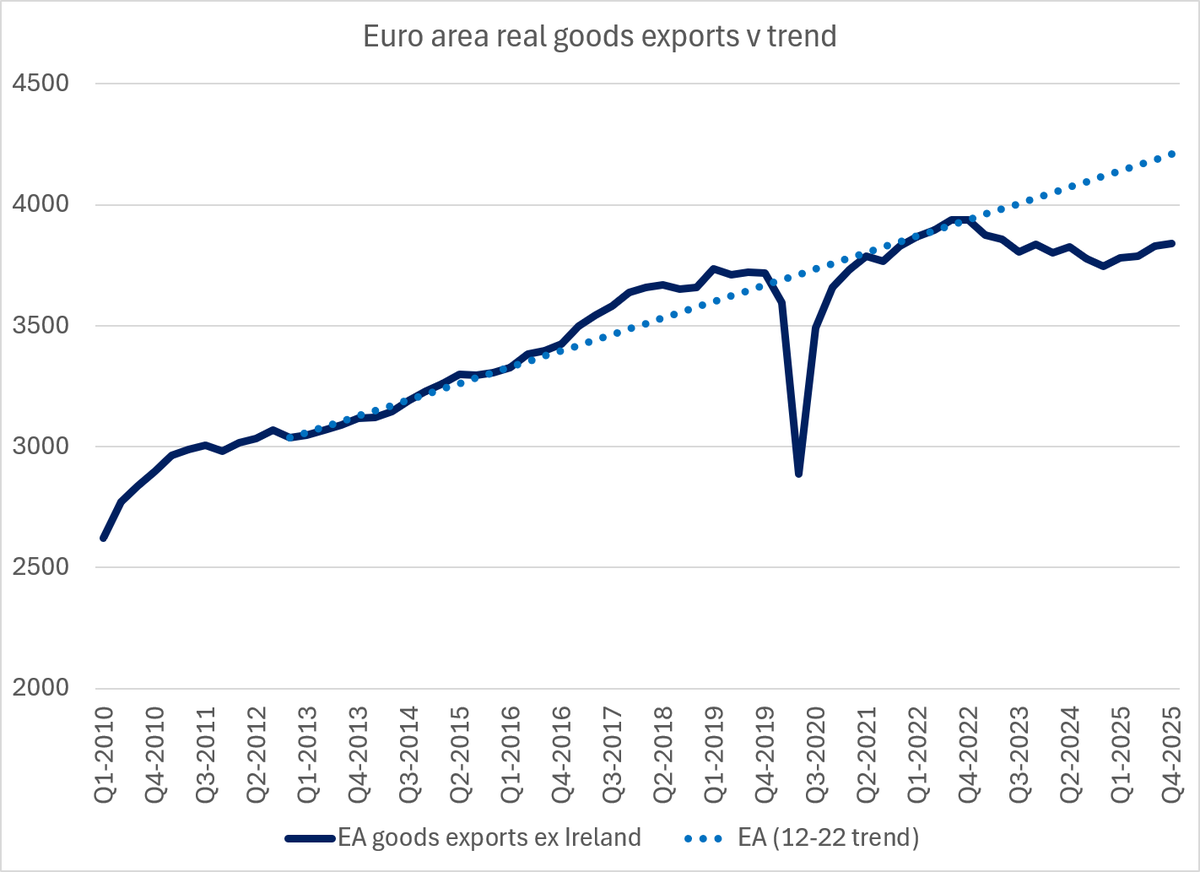

And there should be no debate over the scale of the challenge facing "legacy" surplus economies -- first and foremost Germany ...

20/20

cer.eu/sites/default/…

20/20

cer.eu/sites/default/…

• • •

Missing some Tweet in this thread? You can try to

force a refresh