Chief Planning Officer, Focus Partners | Prof of Practice in Tax, The American College | Lead Fin Plan Nerd, https://t.co/PQnTgtrk2b | Dad x3 + husband | Opinions are my own

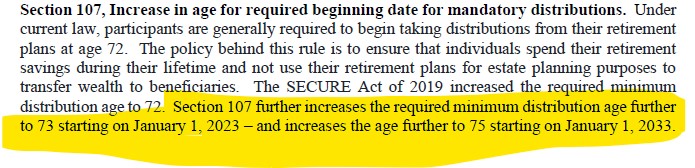

2/x

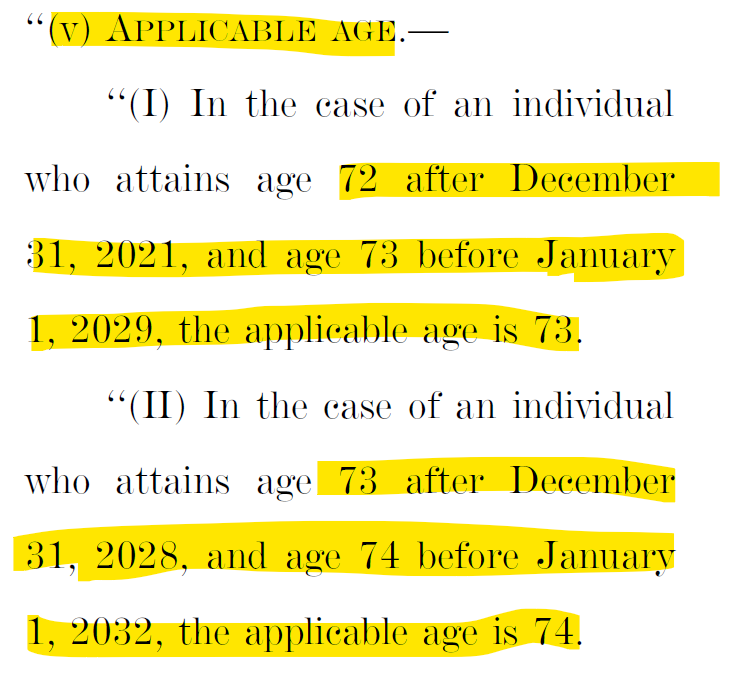

2/x