Economist based in Brussels (🇧🇪). This is my private account and doesn't reflect the views of my employer.

„Merkel, Altmaier sowie Bundeswirtschaftsminister Philipp Rösler (FDP) möchten bei der chinesischen Führung jetzt erreichen, dass diese ihre Subventionspraxis eindämmt, um eine Klage noch abzuwenden.”

„Merkel, Altmaier sowie Bundeswirtschaftsminister Philipp Rösler (FDP) möchten bei der chinesischen Führung jetzt erreichen, dass diese ihre Subventionspraxis eindämmt, um eine Klage noch abzuwenden.”

@Springernomics "Bekanntester deutscher Vertreter der Theorie ist Dirk Ehnts, Vorstandssprecher der Samuel-Pufendorf-Gesellschaft für politische Ökonomie."

@Springernomics "Bekanntester deutscher Vertreter der Theorie ist Dirk Ehnts, Vorstandssprecher der Samuel-Pufendorf-Gesellschaft für politische Ökonomie."

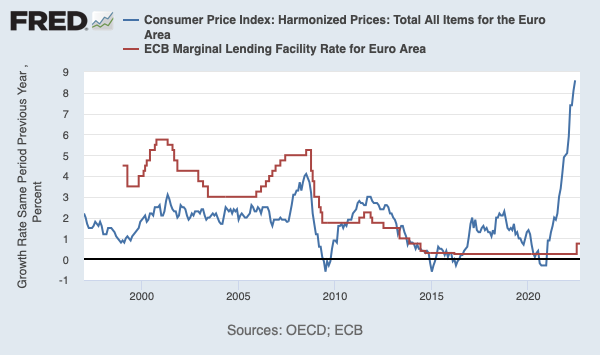

The Euro was introduced in 2002, exchange rates fixed in 1999. So, we have interest and inflation rates from 1999 onwards. From late 1999 the ECB raised interest rates, but inflation was steady at around two percent.

The Euro was introduced in 2002, exchange rates fixed in 1999. So, we have interest and inflation rates from 1999 onwards. From late 1999 the ECB raised interest rates, but inflation was steady at around two percent.

Featuring @StephanieKelton, @TheStalwart, @FadhelKaboub, @nssylla, @rohangrey, @billy_blog, @ptcherneva, @GennaroZezza, @RichardJMurphy (in order of appearance), many others and myself (on #MMT in the Eurozone).

Featuring @StephanieKelton, @TheStalwart, @FadhelKaboub, @nssylla, @rohangrey, @billy_blog, @ptcherneva, @GennaroZezza, @RichardJMurphy (in order of appearance), many others and myself (on #MMT in the Eurozone).

The Slovaks use the €uro, the Czech the Czech crown. Maybe the exchange rate of the Czech crown has moved and done something to the inflation rate. Or maybe government spending is higher in the Czech than in the Slovak Republic (data is not available). [2/n]

The Slovaks use the €uro, the Czech the Czech crown. Maybe the exchange rate of the Czech crown has moved and done something to the inflation rate. Or maybe government spending is higher in the Czech than in the Slovak Republic (data is not available). [2/n]